US: Trump To Sign Tariff-Related Executive Orders Shortly

US President Donald Trump is shortly due to sign executive orders at the White House that are expected to outline unilateral tariff rates for countries that haven't yet struck trade deals with the United States. LIVESTREAM

- MNI's US Daily Brief details Trump's flurry of trade announcements yesterday and outlines countries that have trade agreements still outstanding. With a South Korea agreement in place, eight countries now have a trade framework with the United States.

- Notable pending trade deals include Brazil (50% threatened tariff rate), Laos (40%), Myanmar (40%), Cambodia (36%), Thailand (36%), Bangladesh (35%), Canada (35%), Serbia (35%), Algeria, (30%), Bosnia and Herzegovina (30%), Iraq (30%), Libya (30%), Mexico (30%), South Africa (30%), Sri Lanka (30%), Brunei (25%), Kazakhstan (25%), Malaysia (25%), Moldova (25%), and Tunisia (25%). Other outstanding deals, including Turkey and Australia, are facing the lowest reciprocal tariff rate of 10%.

- Treasury Secretary Scott Bessent yesterday urged corporate America, investors and US trade partners “not to panic” if tariff rates surge on Aug. 1 because deals have not been reached yet, saying that countries “can still do a deal” after Trump’s deadline expires, per CNBC.

- Trump also signed an executive order yesterday to end a "de minimis" tariff exemption for low-value commercial shipments.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Resumes Its Uptrend

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6603 High Nov 11 ‘24

- RES 1: 0.6590 High Jul 01

- PRICE: 0.6565 @ 16:29 BST Jul 01

- SUP 1: 0.6500 20-day EMA

- SUP 2: 0.6453/6373 50-day EMA / Low Jun 23 and a reversal trigger

- SUP 3: 0.6357 Low May 12

- SUP 4: 0.6275 Low Apr 14

The medium-term trend set-up in AUDUSD remains bullish and Monday’s gains strengthen current conditions. The break higher marks a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 0.6603 next, the Nov 11 2024 high. Key short-term support has been defined at 0.6373, the Jun 23 low. A pullback would be considered corrective.

US TSYS: Late Japan, India Trade Deal Comments Rattle Markets Briefly

- Treasuries look to finish weaker but off lows - drawing some buy interest after Pre Trump commented on trade deals with Japan and India.

- Bloomberg headlines: "DOUBT WE'LL HAVE DEAL WITH JAPAN" , "ON JULY 9 DEADLINE: NOT THINKING ABOUT EXTENDING" while "SUGGESTS JAPAN COULD PAY 30% OR 35% TARIFF".

- Nikkei spun it a little differently: "US TO HANDLE JAPAN LATER IN TARIFF TALKS, PRIORITIZING INDIA".

- Tsy Sep'25 10Y futures trade -7.5 at 111-28.5 after the bell vs. 111-22.5 low, 10Y yield +.0176 at 4.2456%. Curves remain flatter: 2s10s -3.167 at 47.299, 5s30s -3.900 at 93.654.

- The bull cycle in Treasury futures remains intact, however prices reversed hard off highs into the Tuesday close. As such, the contract has failed on the approach to the next important resistance at 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Note that the uptrend is overbought, a pullback would unwind this position. First key support to watch is 111-05+, the 20-day EMA.

- Stocks dipped (SPX emini -3.75 at 6250.0) as did US$ slightly after climbing off morning lows into midday high (BBDXY: 1185.43 low / 1191.23 high).

- Looking ahead: Wednesday data focus on MBA Mortgage Applications at 0700ET, Challenger Job Cuts at 0730 followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

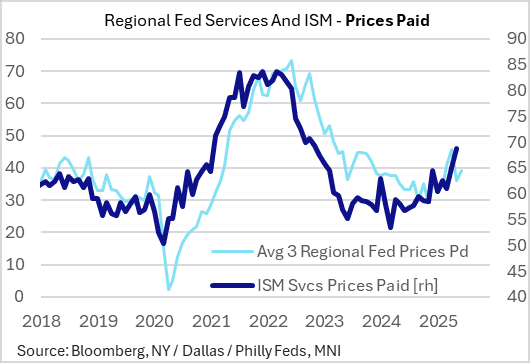

US OUTLOOK/OPINION: ISM Services Prices Should Have Steadied In June (2/2)

The ISM Services Prices Paid gauge is seen moderating to 68.4 from 68.7, which would be the first drop since March but still keep the index above 60 for a 7th consecutive month.

- Part of this expectation for a moderation derives from June's flash S&P Global PMI report which noted that while service sector prices "rose sharply...often attributed to tariffs but also reflecting higher financing, wage and fuel costs", "service sector input costs and selling prices nonetheless rose at slower rates than in May, in part reflecting more intense competition."

- Conversely, across regional Fed surveys, we saw a pickup overall in June, with rises of varying magnitudes in each of the Philadelphia, Dallas, and New York surveys, with the Richmond Fed's 1-year % change rising to 5.2% from 5.0%.

- That said, the rapid rise in the ISM Services prices paid gauge wasn't reflected by the pullback in Fed surveys in May and June vs April's recent peak.