SECURITY: Trump Assured Arab Leaders On West Bank, Gaza Ceasefire Remains Remote

Politico reporting that US President Donald Trump, “promised Arab leaders during a meeting Tuesday that he would not allow Israeli Prime Minister Benjamin Netanyahu to annex the West Bank, according to six people familiar with the discussion.”

- The report appears to refer to a meeting at the UN General Assembly yesterday, where Trump is understood to have presented a group of Arab and Muslim leaders a new US proposal to end the war in Gaza. There haven’t yet been any official readouts.

- The report comes after “Several ministers in Prime Minister Benjamin Netanyahu’s far-right government demanded that Israel annex the occupied West Bank,” in retaliation for the UK, France, Canada, Australia, and others, recognising Palestinian statehood, per FT.

- Politico notes that “despite Trump’s assurance, a ceasefire to end Israel’s nearly two-year war against Hamas was nowhere close to fruition,” according to a source familiar with yesterday’s talks.

- Poliico notes that Arab and Muslim leaders aimed to impress on Trump “that any Israeli incursion into the West Bank would likely lead to the collapse of the Abraham Accords,” Trump's signature first-term foreign policy achievement that he wants to expand to include Saudi Arbia.

- At 17:30 ET 22:30 BST, Secretary of State will hold a press spray ahead of a meeting with his counterparts from Egypt, Saudi Arabia, and the UAE, the three countries likely to backstop post-war Gaza security. Rubio will follow with a separate meeting with counterparts from the Gulf Cooperation Council Member States.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

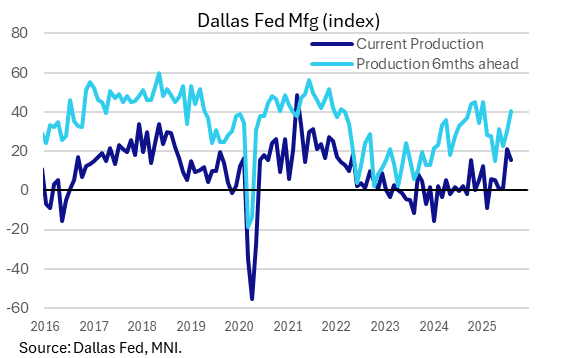

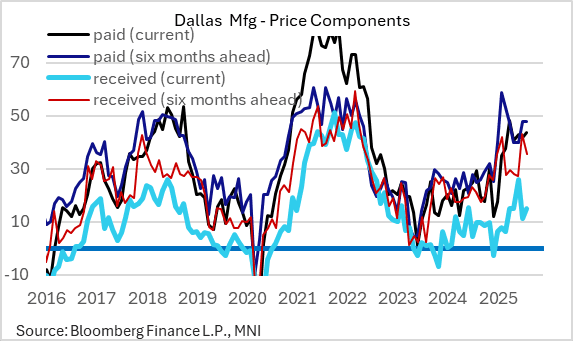

US DATA: Better Activity, Still-Elevated Inflation In Texas Manufacturing Sector

The Dallas Fed's Texas Manufacturing Outlook Survey for August showed continued growth in regional production, albeit with a slightly bigger than anticipated relapse in the overall general business activity index and slightly firmer price pressures. While these readings are volatile month-to-month, they continue to suggest improvement in activity after a tariff-hit period, but price pressures remain elevated (and regional firms still sound extremely concerned about tariff impacts).

- The general business activity index, which is tracked by Bloomberg consensus, missed expectations at -1.8 (vs -0.9 expected, +0.9 prior), which the Dallas Fed characterizes as "indicating little change in activity".

- But this underplayed the broader current strength in activity in the report. The production index, "a key measure of state manufacturing conditions" per the report, fell to 15.3 from 21.3 prior but remained above average, and other measures were also solid. The highlights in that department were new orders, rising for the first time since January (5.8 from -3.6), and shipments rising 12 points to 14.2 for a 3+ year high.

- Forward-looking indicators also suggested improvement (the 6-month production outlook rose to a 7-month high 40.4), while "labor market measures suggested increases in employment and work hours".

- Against this backdrop, price pressures mostly edged higher: current prices paid to a 5-month high 43.7 (up 2.0 points) with priced received at a 2-month high 15.1 (up 4.0 points). 6-month ahead prices paid were basically unchanged at 47.8 (up 0.1 points) albeit a fresh 5-month high, with future prices received pulling back to a 2-month low -12.3 from -4.5.

- Special questions (which also covered services firms ahead of Tuesday's Dallas Fed services release) showed that 48 percent of surveyed businesses "said they’ve been negatively impacted by higher tariffs this year" (just 2% said they were positively impacted), with more than 70 percent of manufacturing firms noting negative impacts. Note also "Firms negatively impacted by tariffs were mixed on whether they passed on cost increases to customers (48 percent of firms) versus absorbed costs internally (39 percent of firms)." The anecdotes in the report add some color to these findings - link here.

US OUTLOOK/OPINION: BofA See Onus Firmly On Data To Prevent Fed Cut

Writing after Fed Chair Powell’s Jackson Hole address on Friday, BofA noted that whilst they formally stick to their call for a hold next month, “the risks have obviously shifted meaningfully toward a cut”. BofA have been one of the more hawkish analysts in recent months, seeing no rate cuts through year-end.

- “The onus is firmly on the data to prevent a cut. A 4.2% u-rate in August, with 70k+ job growth and minimally negative/positive revisions, could keep a hold in play. A 4.1% u-rate would lower the threshold for payrolls, but 4.3% would raise it significantly. If it's a close call, August CPI and PPI should also matter.”

- “Barring further deterioration of the labor market, we think that the Fed would risk a policy error if it were to cut rates. We see signs that economic activity has picked up after the soft patch in 1H. If that is correct, the labor market will likely also rebound. Meanwhile, the underlying inflation picture - excluding of tariffs - has not improved since the Fed started cutting last year. The lagged housing component has decreased substantially, but other components have been flat or up.”

- “While challenging our view to fade near-term cuts, the speech endorses our recommendation to receive 5y OIS (entry 3.44, target 2.8, stop 3.8 current 3.40”). […] We continue to think that a dovish Fed, alongside easy financial conditions and sticky inflation, should support 10-year BEs and the belly inflation in the US versus Europe.”

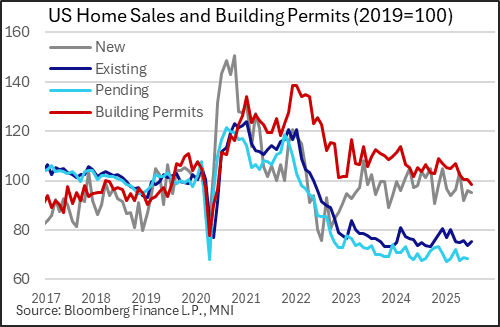

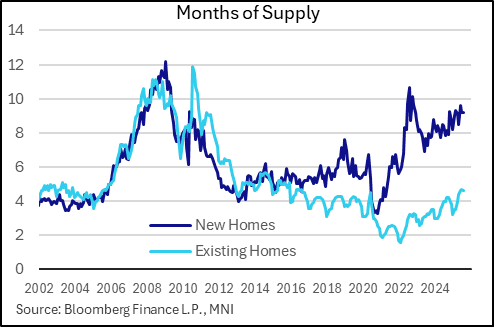

US DATA: New Home Sales Activity Not As Bad As Once Thought, But Still Weak

New home sales were much stronger than expected in July, with an upward revision to June suggesting that activity has been stronger this summer than previously estimated - but nonetheless, broader trends of elevated inventories and falling prices continue to suggest increasing slack in the new build market.

- The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k). This is a significant improvement from May's near-18 month low (623k), though still keeps sales below pre-pandemic (2019) levels (and down 8% Y/Y).

- Regionally, sales were mixed, with falls in the Northeast and West more than compensated for by rises in the South and Midwest.

- The pickup in activity will be welcome news for homebuilders, though the rest of the data remained tenuous.

- One element of good news was that revisions were also seen in lower inventories, closer to 500k the last couple of months whereas June's data had previously shown 511k houses on the market which would have been highest since October 2007 (instead, the distinction of highest since 2007 reverts to March's 504k).

- That said, inventories remain over 9 months of supply equivalent (9.2 for 2 consecutive months) albeit a little below the 9.6 in May though well above levels that prevailed in the tight markets of 2021-23 and above the 7.9 months a year earlier.

- Additionally the data showed a 5.9% Y/Y fall in median prices ($403.8k, $20-30k below prices seen in 2022-23 at the height of the market).

- As such the broad sweep of data continue to indicate deterioration in the new homes market overall, though it may be worsening at a lesser rate than previously thought. This will continue to keep a lid on residential construction activity.