EU TRANSPORTATION: Travel gets a beating

Seems nothing personal against ADP. On long-end (5Y+) travel names are:

- Dufry (HY) +22

- Lufthansa +14

- Heathrow +7-13

- easyJet +10

- Melbourne +6-8

- Sydney +6-7

But holding better are

- Royal Schiphol +5

- MAG +2

- Gatwick +2

- Avinor unch +1

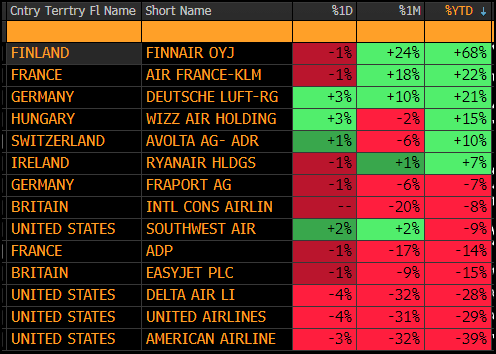

Concerns are likely driven by earnings cuts from US Airlines which are being blamed on weak domestic conditions:

- American: 1Q revenue cut from +3-5% to flat which it sees driven by safety concerns post flight 5342 accident and "softness in domestic leisure segment, particularly in March"

- Delta: 1Q revenue cut from +7-9% to +3-4% on weak domestic demand driven by macro uncertainty. Notes "Premium, international and loyalty revenue growth trends are consistent with expectations"

- Southwest: 1Q unit revenues cut from +5-7% to +2-4% portion of that cut on California wild fires and less government travel rest on soft bookings and demand trends.

- Dufry guides through it noting :"year-to-date 2025 numbers does already include a clear slowdown in the U.S. And despite that, you cannot see those effects in the consolidated numbers because other regions more than compensated for that."

European Reported Traffic (Jan/Feb)

- Ryanair: (+2/+14%), load factor (+2ppt/unch)

- Wizz: (+5%/+4%), load factor (+2/+4ppt)

- Finnair: (+7%/+5%), load factor (+4/+3ppt)

- Heathrow: (+5.4%/-1.5%)

- Frankfurt: (-3.1%/-0.1%)

Perhaps in-line with both the above, local equities are holding firmer (see below)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRIA: FPÖ & ÖVP Leaders Meeting w/President As Coalition Talks Falter

Leaders of the two political parties tasked with forming a governing coalition meeting with Federal President Alexander van der Bellen presently amid speculation that talks have ground to a halt and could collapse. Herbert Kickl from the far-right Freedom Party of Austria (FPÖ) and Christian Stocker of the conservative Austrian People's Party (ÖVP) are meeting van der Bellen separately according to reports from Der Standard.

- Talks have reportedly hit a roadblock in the past week due to disagreements on the distribution of ministerial portfolios, as well as concerns within the ÖVP of whether a gov't likely led by Kickl would be sufficiently committed to maintiaining a pro-EU, anti-Russia stance, and protecting media freedoms.

- On his way to meet the president, Kickl denied talks had broken down saying "If the negotiations had failed, you would have heard something about it." He claims that his meeting with Stocker on 10 Feb 'went well' and were carried out in a good atmosphere. The FPÖ leader has reiterated that his party holding the Interior Ministry, which controls migration policy as well as law enforcement and the security services, is not up for debate despite ÖVP demands to hold onto the office.

- Should talks collapse there are a number of possible options. One is the appointment of a technocratic gov't of experts by the president. Another is that the ÖVP re-enters coalition talks with the centre-left Social Democrats and liberal NEOS. Alternatively, if none of these options are palatable, snap elections could be called.

LOOK AHEAD: Wednesday Data Calendar: CPI/Annual Revisions, Fed Chair Powell 2.0

- US Data/Speaker Calendar (prior, estimate)

- 12-Feb 0700 MBA Mortgage Applications (2.2%, --)

- 12-Feb 0830 CPI MoM (0.4%, 0.3%), YoY (2.9%, 2.9%)

- 12-Feb 0830 CPI Ex Food & Energy MoM (0.2%, 0.3%), YoY (3.2%, 3.1%)

- 12-Feb 0830 Real Avg Weekly Earnings YoY (0.5% revised, --)

- 12-Feb 0830 Real Avg Hourly Earning YoY (1.2% revised, --)

- 12-Feb 1000 Fed Chair Powell House Financial Services testimony

- 12-Feb 1130 US Tsy $62B 17W bill auction

- 12-Feb 1200 Atlanta Fed Bostic economic outlook (no text, Q&A)

- 12-Feb 1300 US Tsy $42B 10Y Note auction (91282CMM0)

- 12-Feb 1400 Federal Budget Balance (-$86.7B, -$89.2B)

- 12-Feb 1705 Fed Gov Waller on Stablecoins (text, Q&A)

AUD: Firmer on Corrective Bounce, With Equities Providing Relief

AUD/USD through the London close at new session highs - the pair is shrugging off any concerns over the installation of steel/aluminium tariffs and instead is benefiting from the relative strength of global equities (rate is following the e-mini S&P higher here) and the resultant tailwind for energy. Key resistance is just above at 0.6302, the 50-day EMA. A break would be bullish.

- While tariff headlines have proved negative for iron ore prices (DCE Iron Ore futures are 2% off the week's highs), the run higher off the January lows will be providing underlying support for the currency.

- Intraday USD weakness remains a key driver more broadly in G10 today which, while mild, is looking through the weakness in the belly of the US curve - driven in turn by EGB/Gilt bond supply given the heavy syndication flow today. More importantly, the front-end of the US curve is stable enough - leaving markets content to sell the USD across the US morning as equities and sentiment improved.

- Despite the latest bounce, the AUD trend structure remains bearish. A resumption of the bear leg would open 0.6045, a Fibonacci projection.