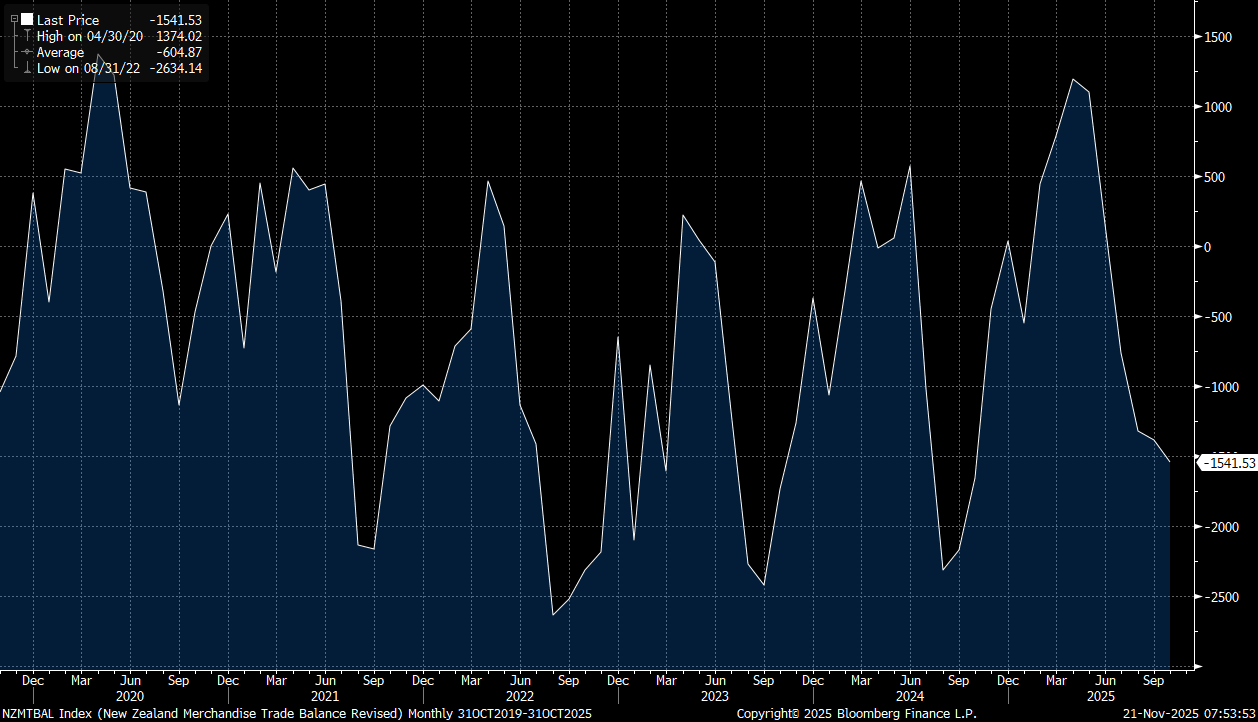

NEW ZEALAND: Trade Deficit Widens In Oct, Not Showing Typical H2 Improvement Yet

New Zealand Oct trade data saw the trade deficit widen slightly to -NZ$1542mn from a revised -NZ$1384mn in Sep. Both exports and imports rose in the month, with imports up by slightly more to drive the wider deficit. The chart below plots the trade deficit for NZ, which usually tends to improve throughout the second half of the year, but this trend isn't evident yet. This is a NZD negative at the margins, and comes after the further decline in whole milk prices earlier this week (at the GDT auction) (see this link). Note the 12 mth YTD deficit was -NZ$2281mn, showing a further trend improvement.

- Exports were up 16% versus Oct 2024 levels, although we are still off earlier 2025 highs in levels terms. Strength was in milk powder and other related products. Exports to China rose 18%, but were up to other destinations as well.

- Imports were up 11% in y/y terms. Stats NZ noted - "petroleum and products**, up $209 million (30 percent); fertilisers, up $209 million (370 percent); mechanical machinery and equipment, up $192 million (19 percent); and electrical machinery and equipment, up $174 million (26 percent)."

- To the extent these import rises reflect a better local investment/domestic demand outlook, will be a watch point going forward.

Fig 1: New Zealand Trade Deficit - Not Showing The Typical Second Half Improvement Yet

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Grind Lower In UST Yields Continued Overnight

Treasury futures finished higher today in a generally strong night for risk assets with the DJIA hitting new highs. TYZ5 finished up +05 at 113-24 after reaching intra-day highs of 113-27+. TYZ5 has opened the Asia trading day at 113-24+ with limited price action at the open.

- The US 2-Yr was unable to get off where it started closing at 3.45%.

- The US 5-Yr ground lower by -1bp to reach 3.56%

- The 10-Yr has consolidated below 4.00%, rallying again overnight by -1.5bps to reach 3.96% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -2.5bps overnight to reach 4.544%. Likely next inflection point could be the April lows of 4.40%.

- SOFR/Treasury options trade mixed on modest volumes Tuesday as the US Gov enters shutdown day 20 while US$ firmer. Projected rate cut pricing steady to mildly mixed vs. late Monday levels (*): Oct'25 at -24.2bp (-24.7bp), Dec'25 at -49.2bp (-50bp), Jan'26 at -64.2bp (-63.7bp), Mar'26 at -78.2bp (-77bp).

- Yield moves are appearing disjointed relative to current interest rate pricing as the government shutdown continues as bond traders agonize over the potential impact on the economy. New ranges are being defined and as markets await the release of the September CPI, markets appeared skewed towards lower yields for now.

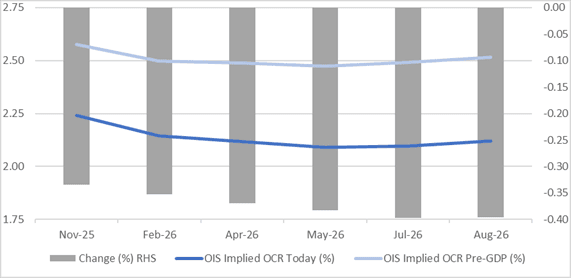

BONDS: NZGBS: Little Changed, Market Awaits Oct 26 RBNZ Cut

In local morning trade, NZGBs are little changed after US tsys finished Tuesday’s session with a modest bull-flattener.

- Stronger-than-expected readings across September headline and core CPI metrics has seen expectations of future BOC cuts diminish slightly, with current meeting dated OIS-implied pricing pointing to about 5bp less easing through the next 4 decisions to March 2026.

- Precious metals sold off sharply on Tuesday, with spot gold currently down by 5.6% at $4,113/oz and silver down by 7.7% at $48.4/oz, albeit off session lows.

- The recent downtrend in whole milk powder prices continued at the overnight auction result (which is held twice per month). We are now 17.5% off the earlier 2025 highs for this price.

- Swap rates are 1bp higher.

- RBNZ dated OIS pricing is little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026. For context, pricing is 34-40bps softer than levels seen in late September before the very weak Q2 GDP print. (see chart)

- The local calendar will be empty today.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

AUD: A$ Underperforms As Metal Prices Fall, AUDUSD Holding Above Support

Aussie underperformed on Tuesday with AUDUSD trending lower through APAC trading and then struggling to return to above 0.6500. It was pressured in the European/US sessions by the correction in gold, weakness in other metals and lacklustre equity performance. AUDUSD fell 0.4% to 0.6488 off the intraday low at 0.6473 and has started today around 0.6491. The USD index rose 0.3%.

- AUDUSD held above initial support at 0.6440, 14 October low. Technicals continue to suggest that there could be a reversal of the bear cycle begun on 17 September.

- Kiwi was one of the better performers in the G10 leaving AUDNZD down 0.3% to 1.1300. It is a bit higher on Wednesday at 1.1307.

- The yen underperformed following new LDP leader Takaichi becoming PM. Her expansionary policy stance has made markets nervous. AUDJPY rose 0.4% to 98.57 after a high of 98.78.

- AUDEUR was little changed at 0.5594 and AUDGBP was 0.1% lower at 0.4853.

- Equities were steady with the S&P flat and Euro stoxx up 0.1%. Oil prices were higher with Brent +0.9% to $61.56/bbl. Gold fell 5.3% to $4125.22/oz. Copper was down 1.7% and iron ore around $104/t.

- There are no data or events in Australia today.