US DATA: Trade Deficit Re-Widens In May As Exports See Historic Pullback

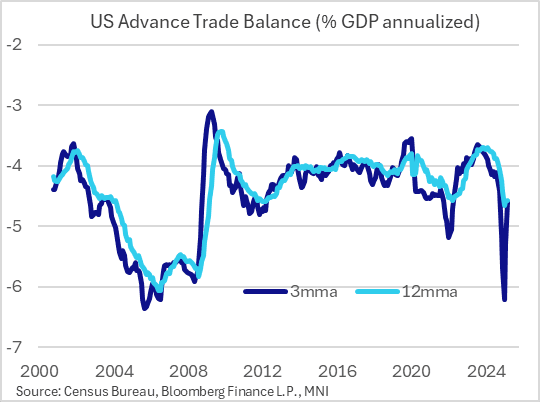

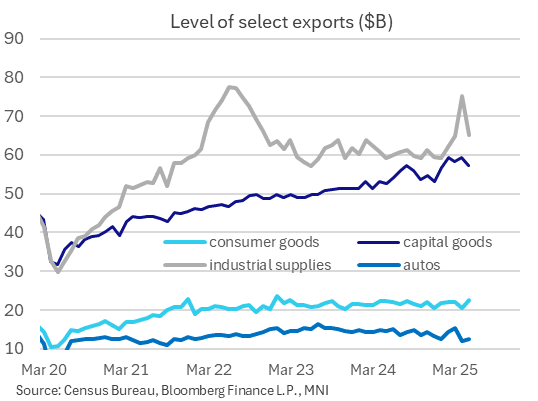

The advance goods trade deficit was bigger than anticipated in May, with the $96.6B shortfall comfortably exceeding the $86.1B survey. This is likely to weigh slightly on Q2 GDP estimates, with weakness in exports particularly concerning.

- This was the 2nd smallest deficit in the last 14 months (April's $87.0B was the other) though, and brings the 3-month moving average of the deficit down to roughly 4.6% of GDP vs the 6.2% peak in March which represented a significant pre-tariff front-loading of imports, including gold.

- But in May, it wasn't imports that drove the widening shortfall - those were steady at $275.8B (vs $275.9B in March), albeit with some volatile category-by-category dynamics highlighted by a 12% rise in auto imports (after -20%), offsetting a 6.2% drop in consumer goods (-32.0% prior). Indeed consumer goods imports hit a 12-month low (all seasonally-adjusted) at $65.6B, continuing to unwind after a record in March close to $103B.

- Instead it was exports that suffered in May, dropping 5.2% M/M - which was the biggest drop since the Global Financial Crisis in 2008, outside of the initial pandemic fallout in April 2020. The major contracting export categories were industrial supplies and materials (including petroleum), down 13.6% (+16.0% in April), with capital goods shipments falling 3.3% (after 1.7%).

- We'll have to wait for the final goods and services trade release on July 3 for the breakdown in individual categories (for example to see to what extent weaker oil exports for example weighed in May as opposed to other industrial products) and a country-by-country breakdown but the magnitude of the pullback in exports is potentially concerning if it turns out they were weighed down by foreign trade retaliation (eg Canada) and thus a "new normal".

- That said, it looks for now - as with imports - a normalization after the pre-tariff spike (note US auto exports remain around their weakest levels since mid-2021). It will probably be a couple of more months at least before volatility shakes out.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SEK: Brief Wave Of SEK Weakness; No Obvious Trigger

Fresh wave of weakness seen in SEK crosses. No obvious headline trigger for the move, which has already started fading.

- EURSEK reached a fleeting high of 10.9937, piercing the 20-day day EMA at 10.8952 in the process.

- USDSEK similarly marked above the 20-day EMA (9.6685), before moving back below the handle. The stronger-than-expected US consumer confidence reading at 1500BST will have also support the USDSEK pair.

- Heavy Swedish data calendar tomorrow, with retail sales, trade, lending and wage data due at 0700BST.

EQUITIES: Firmer Cash Markets, But Overnight Futures Gains Fail to Hold

- US cash markets gap higher at the open on the overnight ramp in futures as Trump outlined a delay to the higher tariff threat levied against the EU. Tech and travel names trade well on the back of the news - with Teradyne, AMD and Oracle all higher alongside airlines.

- The e-mini S&P still holds 65 point gains on the day, but is off overnight highs. This keeps the price pinned well between the longer-term trend indicators of the 100- and 200-dmas. A bullish trend condition remains intact and the latest pullback is considered corrective. A key support lies at 5719.58, the 50-day EMA.

- Carmakers are the strongest subcomponent, but the performance is far from uniform: Tesla is higher by ~4% against much smaller gains for General Motors and Ford - better S/T trade relations with Europe are underpinning the rally, but Musk's reassurance that he's back working hard for Tesla will be shoring up the price.

- Trade headlines remain an ever-present background risk, but geopolitics is containing any breakout higher in prices after Trump's more belligerent tone with Putin on top of Germany's announcement over the weekend that Western weaponry can be used deeper into Russian territory - allaying any hopes of an imminent reset in Ukraine-Russia relations.

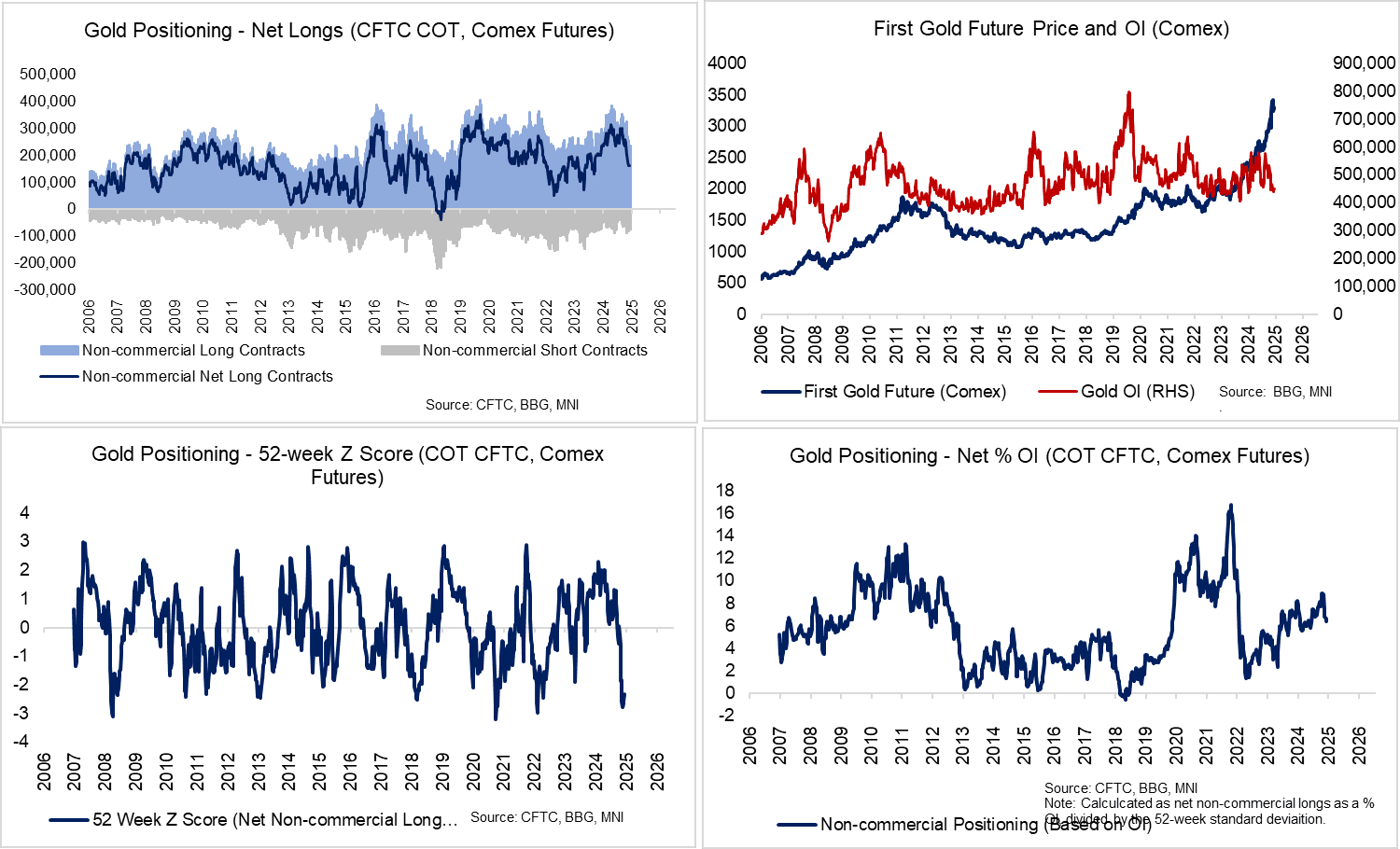

GOLD: 20-day EMA and USD Pullback Lends Gold Support; Technical Outlook Bullish

Gold has fallen 1.4% to ~$3,300/oz, but a move away from highs for the broader USD index and support from the 20-day EMA has contained downside intraday. Technically, the recovery from the May 15 low has signalled an end to the corrective phase that started on April 22. Medium-term trend signals are unchanged and remain bullish, with initial resistance at $3365.9 (May 23 high). This level shields the May 7 high at $3435.6.

- Even though peak US effective tariff rates appear to be in the rear-view, US President Trump’s U-turn on 50% EU tariffs last weekend indicates that trade policy uncertainty remains acute. Taken alongside ongoing US fiscal concerns, the case for gold in portfolios and as central bank reserves remains strong.

- Following the aformentioned corrective phase between Apr 22- May 15, the positioning backdrop is also cleaner for those looking to re-enter gold longs.

- TD Securities note that “CTAs will buy gold in any scenario over the coming week. We expect that systematic trend followers will grow their position size by a third by this time next week (or +10% of max size), benefiting from vol-control and rising signal strength. This will mark the first notable buying impulse in gold futures following large scale liquidations associated with macro fund divestment in the weeks surrounding Liberation day”.

- Looking at the sources of gold demand, TD write that “only retail ETF holders are vulnerable, both in the West and the East. A shift in strategic asset allocations has contributed a significant portion of recent global ETF inflows, suggesting that persistent central bank buying activity should be sufficient to offset such outflows from retail holders”.

- According to World Gold Council data, there was $3.4bln of outflows from Gold ETFs between May 5 and May 23 (31.4 tonnes). Monthly data for April covering Central Bank flows should be released around the start of June.