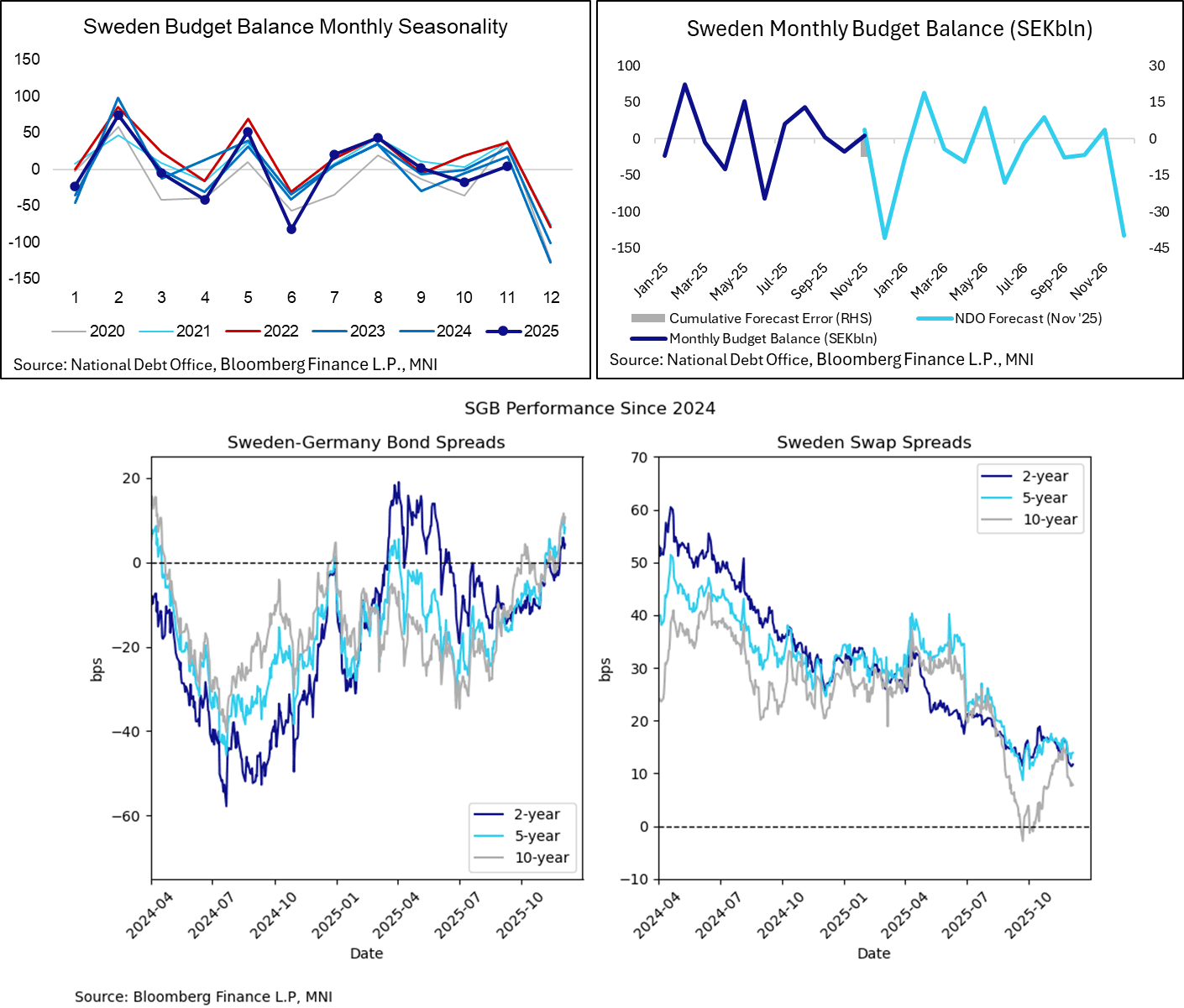

SWEDEN: Today's SGB Underperformance An Outlier In The European Bond Space

The 10-year SGB/Bund spread is ~1.5bps wider today at ~8.5bps, making Swedish bonds a notable outlier across the DM space save for GoCs. Over the last week, SGBs have consolidated underperformance catalysed by the National Debt Office’s November borrowing report, which featured a larger than expected increase in nominal SGB issuance for 2026/2027. This underperformance could extend if incoming domestic macroeconomic data continues to print on the firm side.

- Today’s underperformance looks to be a function of the November budget balance data. Sweden ran a surplus of SEK4.5bln in November, below the SEK12.1bln expected by the NDO. The NDO noted that tax revenues were SEK5bln lower than expected last month.

- This was the first month of fiscal data since the NDO’s borrowing report was released, but nonetheless keeps the theme of increased issuance needs at the forefront.

- Note that Wednesday's nominal SGB auction also saw slightly weaker demand metrics than the prior three outings. The final nominal SGB auction of the year will be held on December 17.

- Next week’s Swedish calendar includes monthly activity data for October, unemployment data for November and details of the (lower-than-expected) November inflation report. These will be important inputs for the Riksbank’s December MPR rate path.

- At the upcoming Riksbank decision, we will be interested in whether there are (upward) rate path revisions in the first three quarters of the forecast horizon – the part of the curve “owned” by the Executive Board and therefore constituting a policy signal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR +5.2M TO 421.2M OCT 31 WK

- US EIA: CRUDE OIL STOCKS EX SPR +5.2M TO 421.2M OCT 31 WK

- US EIA: DISTILLATE STOCKS -0.64M TO 111.5M IN OCT 31 WK

- US EIA: GASOLINE STOCKS -4.73M TO 206.0M IN OCT 31 WK

- US EIA: CUSHING STOCKS +0.3M TO 22.9M BARRELS IN OCT 31 WK

- US EIA: SPR +0.5M TO 409.6M BARRELS IN OCT 31 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -0.6% TO 86.0% IN OCT 31 WK

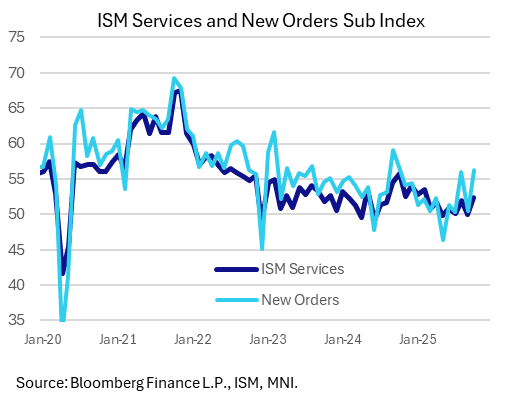

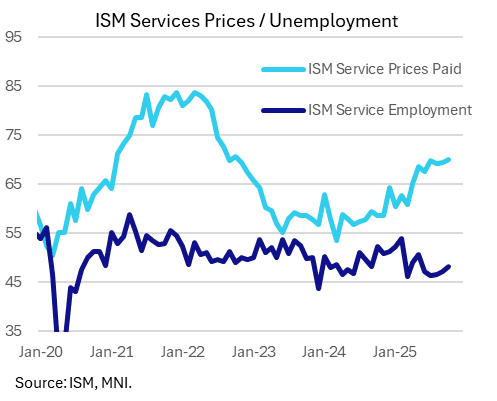

US DATA: ISM Services Activity Bounces Strongly In October, But Prices Edge Up

October's ISM Services report was the strongest overall since early in the year, with the headline PMI index rising to 52.4 from 50.0 for an 8-month high. This easily exceeded the expectation for a slight uptick to 50.8 and came with improvements in most of the key subcomponents, though employment remained weak and there were signs of continuing acute inflationary pressures.

- October saw better readings in Business Activity/Production (+4.4 to 54.3, largely reversing a 5.1 point drop in September), New Orders (+5.8 to a 12-month high 56.2 vs 51.0 expected, likewise reversing a 5.6 point fall in September), Employment (+1.0 to a still-contractionary 48.2 but vs 47.6 expected and a 5-month high), New Export Orders (+1.3 to 4-month high 47.8), and Inventories (+1.7 to 49.5).

- Overall, "comments from many industries mentioned continuing demand stability.”

- On the employment and activity readings, the ISM points out "There was no indication of widespread layoffs or reductions in force, but the federal government shutdown was mentioned several times as impacting business activity and generating concerns for future layoffs."

- Backlog of Orders notably fell 6.5 points to 40.8 for the 2nd lowest reading since May 2009 (per the ISM this hints at increasing productivity: "even with a contracting Employment Index, companies can more than keep up with new orders to reduce backlogs"), while Supplier Deliveries slowed 1.8 points to 50.8. Imports fell 5.5 points to 43.7 suggesting continued impairment of normal trade amid tariff/supply chain uncertainty.

- Inflation remained a problem. The increase in Prices Paid to 70.0 from 69.4 marked the highest print since October 2022 in a continuation of the increases seen more or less since early 2024. This defied consensus expectations for a pullback to a 4-month low 68.0, but corroborates the S&P Global PMI's finding of costs increasing sharply in the month. Per the ISM: "Respondents continued to mention the impact of tariffs on prices paid."

- Indeed this brought the activity gauge a little closer to the S&P PMI which has been signalling robust Services expansion in contrast to a relatively flat ISM.

EURIBOR OPTIONS: Adding to the Large Outright Call

ERU6 98.50c, bought for 3.25 in 17.5k total.