EU COMMUNICATIONS: TMT: Week In Review

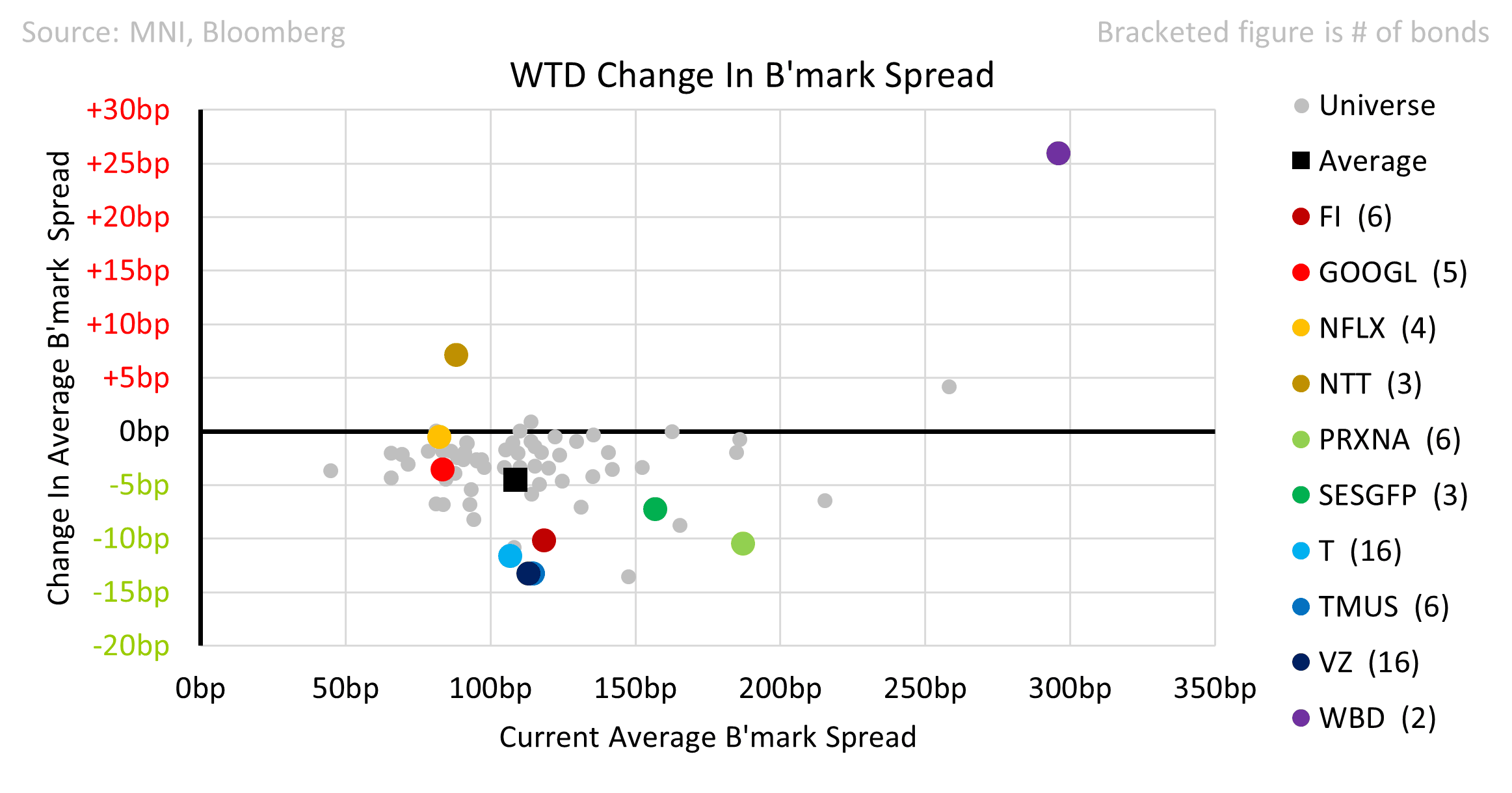

• On spreads, the overall sector slightly outperformed the strong market with a 5bps tightening. WBD was 25bps wider with NTT and WorldLine also soft. Verizon and AT&T are notably large issuers so their moves of 12-13bps better will have been impactful.

• The Warner Bros curve steepened after CNBC reported that a split in the group was likely in the near-term. The curve widened significantly over the summer on concerns that debt would be left with the legacy TV ops while the growth drivers were split from the group. We don’t see anything in the bond docs that would prevent such a move.

• We expect the NTT Group bid for the outstanding shares in NTT Data to have ratings impact. The name was placed on negative watches at Moody’s and S&P with downgrades likely. We also noted President Trump’s comments on a potential film tariff. FY25 results showed a soft final quarter and confirmed higher YoY leverage.

• Earnings this week included Amadeus (Neutral), Infineon (Slight Neg), Nexi SpA (Neutral), Swisscom (Slight Neg), Warner Bros (Mixed), JCDecaux (Neutral), Fidelity (Neutral), Global Payments (Neutral), Telenor (Neutral).

• Elisa came for a small €300mn 5yr deal that tightened 35bps to price at MS+85bps (flat to our FV with a 3.1x cover.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US MBA: MARKET COMPOSITE +20.0% SA THRU APR 04 WK

- MNI: US MBA: MARKET COMPOSITE +20.0% SA THRU APR 04 WK

US TSYS: Latest Aggressive Steepening Pared, 10Y Auction Watched

- Treasuries trade bear steeper overnight as US assets have come under pressure following the pushing ahead with higher “reciprocal” tariffs for those countries with trade surpluses with the US and yesterday’s acknowledgement of 104% tariffs on China.

- Recent lurches higher in the VIX and MOVE indices will likely have prompted deleveraging, while a potential continued unwind of basis trade positions remains in focus for the bond market.

- A weak 3-year auction added pressure yesterday afternoon with its 2.4bp tail. Although indirect take-up for the 3-year supply was broadly in line with recent auctions at 66.94%, it still raises questions around broader Tsy demand. Today's 10-year and tomorrow's 30-year auctions will come under even greater scrutiny as a result.

- Cash yields are 6-10.5bp higher, with 7s leading the increase and 2s lagging.

- Highlighting the wide ranges that continue to be seen, 30Y yields are at 4.86% (+9.5bp) but earlier briefly topped 5%, broadly meeting the Jan 14, 2025 high at a level last seen in Oct 2023. The Oct 2023 high of 5.1764% was its highest since 2007.

- 2s10s sits at 61bp (+4bp) having topped out at 73.8bp overnight for steeps since early 2022.

- TYM5 trades at 110-23+ (-24) following another overnight session with huge volumes, currently at 1.4mln.

- It saw an overnight low of 110-01, continuing a breach of both 20- and 50-day EMAs to focus attention on trendline support at 109-29 (drawn from Jan 13 low). To the upside, resistance at 112-08 (Apr 7 high).

- Data: Weekly MBA mortgage data (0700ET), Wholesale inventories/trade sales Feb F/Feb (1000ET)

- Fedspeak: Barkin (1100ET), FOMC minutes (1400ET) – see STIR bullet.

- Coupon issuance: US Tsy $39B 10Y note re-open - 91282CMM0 (1300ET)

- Bill issuance: US Tsy $60B 17W bill auction (1130ET)

SCHATZ: Swap related trade

Schatz Swap related trade, suggest Payer:

- DUM5 ~5.25k at 107.56.