EU TECHNOLOGY: TMT: Week In Review

Mar-07 11:59

- BBG’s C&S/M&E/Telco/Tech indices -5/-1/+1/+1bp WoW vs. €IG corps. YTD: +3/+1/+2/+6bp.

- TMT IG primary closed this week. On ratings, AT&T was moved to positive outlook by S&P (now Baa2/BBB[P]/BBB+) while Fitch downgraded Eutelsat SA’s IDR/SUN rating from BB+[N] (now B1/B/BB[N]) with the Eutelsat Comms holdco also downgraded.

- On earnings, we had results from JCDecaux (mixed), Informa (mixed), ITV (slight pos) and Universal Music (slight pos) though none were the drivers of any notable spread divergence.

- Elsewhere we flagged positive satellite news as political dynamics weigh on Starlink prospects in Europe, S&P commentary on WBD earnings and journalistic speculation on a WPP buyout.

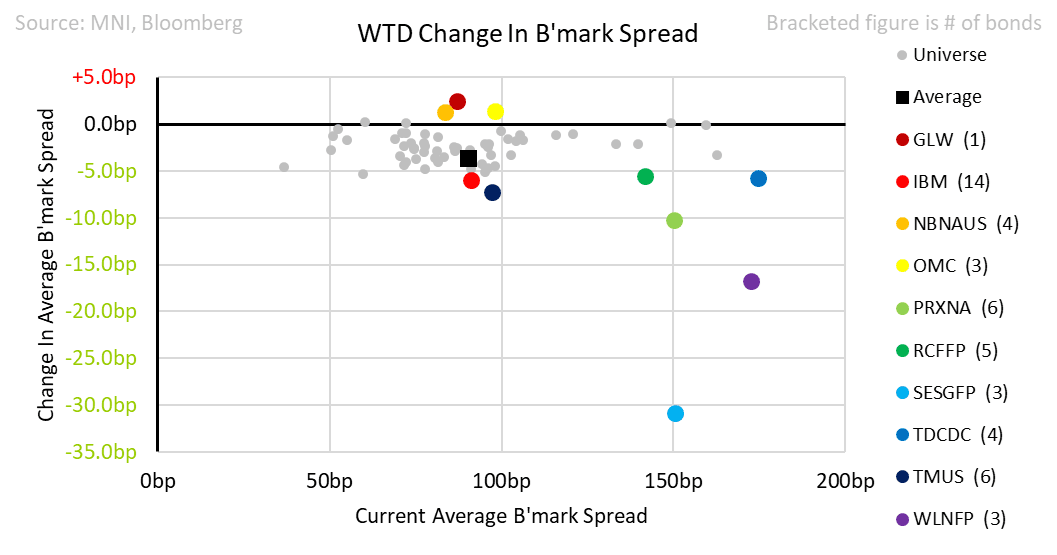

- On spreads, SES was the notable IG performer while Eutelsat bonds are 5-13pts higher vs. Friday’s close on the positive sector news. Elsewhere, higher beta names like Worldline and Prosus also outperformed amidst the risk-on tone.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: TY Testing Resistance, Refunding and ISM Services Headline The Docket

Feb-05 11:51

- Treasuries have extended yesterday’s rally that received a helping hand from lower-than-expected jobs openings, with today’s gains amidst broader FI rallies including from EGBs and Gilts.

- Today’s calendar focus is primarily on Treasury’s QRA at 0830ET (MNI Refunding Preview here) before ISM services for January at 1000ET. US policy headlines will also be closely watched, especially on US-China trade relations.

- Cash yields are 2.3-4.2bp lower, with declines led by 7s.

- 2s10s is within recent ranges at 28.5bps (-1.6bp).

- TYH5 sits close to session highs of 109-15 (+ 08+) on solid cumulative volumes of 410k.

- It challenges resistance, having cleared 109-10 (50-day EMA) and now eyeing 109-15+ (Feb 3 high). A clear break of the 50-day EMA would strength a short-term bullish case and open 109-31 (Dec 18 high).

- Data: MBA mortgages (0700ET), ADP employment Jan (0815ET), Trade bal Dec (0830ET), S&P Global US serv/comp PMI Jan final (0945ET), ISM services Jan (1000ET)

- Fedspeak: Barkin BBG TV (0730ET), Barkin fireside chat (0900ET), Goolsbee at automotive conference (1430ET), Bowman update on economy and bank regulation (1500ET), Jefferson gives lecture after the close (1930ET) in remarks likely to heavily resemble yesterday’s speech – see STIR bullet.

- Bill issuance: US Tsy $64B 17W bill auction (1130ET)

NORWAY: January House Prices Well Above Norges Bank Forecast

Feb-05 11:50

Norwegian secondary house prices rose a notable 1.4% M/M SA in January, up from 1.0% in December and well above Norges Bank’s 0.5% M/M projection in the December MPR. All else equal, this will be a hawkish input into Norges Bank’s March rate path, but is unlikely to deter a well-signalled 25bp cut.

- Low supply of new built homes since the pandemic has shifted demand towards existing homes, and continues to be a key driver of existing home price rises.

- Eiendom Norge also point to “less uncertainty about the household economy going forward” alongside “moderate relief in lending regulations”.

- There were record numbers of home listings and sales in January, according to the press release.

- There was little reaction in NOK to the data, with NOKSEK extending session lows at typing amid continued SEK strength, now 0.3% lower today,

OAT: Block trade

Feb-05 11:48

OAT Block trade, suggest buyer:

- OATH5 ~1k at 124.62.