UK FISCAL: Ten big picture takeaways from the Budget (2/3)

Nov-28 16:39

- 4. OBR forecasts still look optimistic to us, further increasing questions over the validity of the headroom. In particular productivity growth of 1.0% still seems on the more optimistic side (albeit this downgrade of 0.3ppt was broadly in line with expectations ahead of the Budget). And the 2026 growth forecast in particular of 1.4% (above the BOE's 1.2% and Bloomberg consensus of 1.1%) also looks optimistic to us.

- 5. Near-term inflation reducing measures are broadly in line to a little higher than expected. The GBP150 cut to energy bills is higher than the GBP84 cut that would have been had VAT on energy been cut with no other policy changes. The “temporary” fuel duty cut of 5p/litre isn’t fully cancelled, but its reversal will be delayed and staggered. The OBR estimates that the policy measures in full will reduce 2026 CPI by 0.3ppt with a peak reduction of 0.5ppt in Q2-26. The government refers to a 0.4ppt reduction “next year” which we assume must be referring to FY26/27. This will make it easier for the MPC to justify cuts – so despite there not being big moves in the front-end on the Budget, we think this is another hurdle removed to a December cut and the option for further cuts into 2026.

- 6. The majority of the energy bill cuts are only temporary for three years and will be reversed in April 2029. This is going to cause the BOE some communication issues if it wants to continue to deliver cuts from its April 2026 meetings onwards, as from the April 2026 MPR it will now have to forecast a big spike in CPI (driven by energy bills) at the end of its forecast period. This makes the timing and communication of cuts deeper into 2026 more challenging, but wasn’t really appreciated on the day of the Budget release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Oct-29 16:04

- EUR/USD: Nov04 $1.1635-40(E1.3bln)

- USD/JPY: Oct31 Y152.50($1.2bln)

- USD/CAD: Oct31 C$1.3500($1.1bln)

MNI EXCLUSIVE: EC inflation forecasts will have to take account of ETS2

Oct-29 15:54

European Commission inflation forecasts will have to take account of the ETS2 carbon-trading scheme..-- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

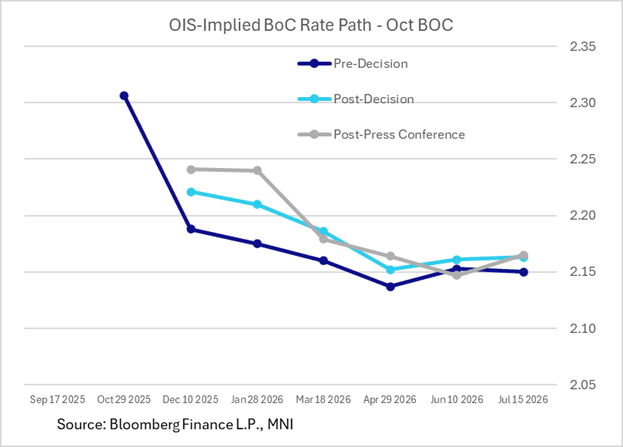

BOC: MNI BoC Review-Oct 2025: Pause Seen With Rates “About Right”

Oct-29 15:53

We've just published our review of the October Bank of Canada meeting - Download Full Report Here

- Along with the expected 25bp cut to an overnight rate of 2.25%, a key phrase from the BOC’s October policy statement drove a mildly hawkish market reaction by signalling an intention to hold rates steady at upcoming meetings (vs market/analyst expectations split between a further 25bp cut or a post-October pause coming into this meeting).

- The key phrase in the statement was: "If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- Though Governing Council didn’t close the door to another cut ("If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast”), the language about rates being “about right” was repeated a few times in the post-meeting press conference, reinforcing the perception that the BOC envisages holding rates in future meetings in its base case, after having reduced policy rates by 275bp in this cycle.

- Terminal BOC overnight rate expectations concluded the press conference at around 2.15%, versus 2.12-2.13% coming into the meeting – suggesting expectations are now leaning more toward an indefinite hold rather than another cut in the cycle.

- The Canadian dollar benefited as well, with USDCAD extending losses through the press conference to move through the 1.3900 handle.

- We haven’t seen any Canada bank analyst view changes as yet. Coming into the meeting, 7 Canadian banks had been split 3/4 in favour of another cut in this cycle beyond October; BMO analysts wrote after the decision they still anticipate another 25bp reduction though we await Desjardins’ and National’s verdicts.