UK FISCAL: Ten big picture takeaways from the Budget (1/3)

Nov-28 16:32

Ten big picture takeaways from the Budget now that the dust has settled. There is more details on all of these points in the MNI UK Budget Review

- There were no big rabbits out of the hat or big negative surprises from any single policy that will have immediate impacts (e.g. headline changes to income tax or other big taxes).

- The welfare and spending increases are all front-loaded – that in itself isn’t a surprise. But quite how backloaded the tax increases are is more of a concern than we had expected. Effectively the large parts of these don’t kick in until April 2029 – and given the electoral cycle and economic / political uncertainty between now and then we are concerned that some of these policies may be further delayed or indeed altered before implementation. Overall this means there is more fiscal stimulus over the next couple of years than expected.

- Headroom was higher than expected at GBP21.7bln (market expectations had been for GBP15bln) but we question its credibility. There is GBP8.6bln from reversing energy bill cuts, efficiency savings and HMRC closing the “tax gap” built into this number alone (with the latter two the increases to these measures since the Spring Statement). Without these headroom would be GBP13.1bln.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Oct-29 16:04

- EUR/USD: Nov04 $1.1635-40(E1.3bln)

- USD/JPY: Oct31 Y152.50($1.2bln)

- USD/CAD: Oct31 C$1.3500($1.1bln)

MNI EXCLUSIVE: EC inflation forecasts will have to take account of ETS2

Oct-29 15:54

European Commission inflation forecasts will have to take account of the ETS2 carbon-trading scheme..-- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

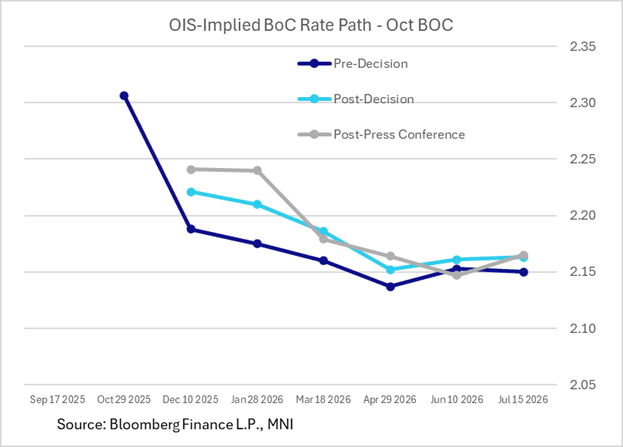

BOC: MNI BoC Review-Oct 2025: Pause Seen With Rates “About Right”

Oct-29 15:53

We've just published our review of the October Bank of Canada meeting - Download Full Report Here

- Along with the expected 25bp cut to an overnight rate of 2.25%, a key phrase from the BOC’s October policy statement drove a mildly hawkish market reaction by signalling an intention to hold rates steady at upcoming meetings (vs market/analyst expectations split between a further 25bp cut or a post-October pause coming into this meeting).

- The key phrase in the statement was: "If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- Though Governing Council didn’t close the door to another cut ("If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast”), the language about rates being “about right” was repeated a few times in the post-meeting press conference, reinforcing the perception that the BOC envisages holding rates in future meetings in its base case, after having reduced policy rates by 275bp in this cycle.

- Terminal BOC overnight rate expectations concluded the press conference at around 2.15%, versus 2.12-2.13% coming into the meeting – suggesting expectations are now leaning more toward an indefinite hold rather than another cut in the cycle.

- The Canadian dollar benefited as well, with USDCAD extending losses through the press conference to move through the 1.3900 handle.

- We haven’t seen any Canada bank analyst view changes as yet. Coming into the meeting, 7 Canadian banks had been split 3/4 in favour of another cut in this cycle beyond October; BMO analysts wrote after the decision they still anticipate another 25bp reduction though we await Desjardins’ and National’s verdicts.