EM LATAM CREDIT: Telefonica Movil. Chile: 3 Alternatives, Choose Wisely–Positive

(MOVCHI; NR/BBneg/BB-neg)

• MOVCHI 31s were quoted at $57.5, 14.4% yield, down 4 points since June 30th and 20 points YTD. Telefonica of Spain is seeking to sell its Chile assets, but the market price for MOVCHI notes reflects pessimism for who the buyer might be, if any. Bonds dropped over 2 points last week upon news that America Movil’s joint bid with Entel was terminated: https://mni.marketnews.com/44EicGP

• We think Telefonica Moviles Chile (TMC) gets sold and its credit profile improves as part of a larger scale entity in a more consolidated Chile telecom market. Regulatory risk is a key consideration as well as financing capacity. We think America Movil is the most likely candidate as it already has taken steps to increase its scale in the Chile telecom market and now, we have a motivated seller providing an opportunity to expand further. The company also has the most financial flexibility. America Movil has room to grow its relatively small presence in Chile, currently lumped in with Uruguay and Paraguay to form the “Southern Cone” division in earnings reports, so it would make sense to increase scale in such a large growth potential market as Chile.

• TMC is a valuable asset for several reasons. The company has a 23% market share in mobile services and is the leader in 5g with 1.5mn subscribers according to Mordor Intelligence who also forecasts 3.6% compound annual growth for the Chile telecom market overall and 2.9% subscriber growth for the next five years. Demand for data and internet is growing and TMC has a 37% leading market share in fiber optics as well as a 28.5% share in broadband. Intense competition amongst four main competitors has pressured margins and profitability.

• The TMC credit profile is already under pressure with EBITDA declines, increasing capex and negative free cash flow causing an increase in net debt leverage, reported at 5x as of Q3 2025 up from 3.5x December 2024. The company has already tapped CL221mn of a CLP371mn 5-year credit line from parent Telefonica of Spain with the balance earmarked for 2025 and 2026 maturities but beyond that the outlook gets cloudier. That murky credit backdrop partly explains the weakness in the bonds with doubts about acquisition from one of the incumbents also contributing as TMC has a significant market share in both mobile and broadband, so a challenging regulatory approval process is expected.

• WOM (WOMMOB; NR), with a 21% market share in Chile mobile services, reportedly already submitted a bid, but skepticism abounds as the Chile telecom company exited bankruptcy March 2025 and now is owned by its bondholders. An additional USD500mn in capital was contributed so it’s less likely that more capital would be forthcoming. The concern then is how the estimated USD1bn price tag would be financed. Private equity firm Novator was the previous owner of WOM and that didn’t work out so well, so there could be reluctance on the part of other private equity shops to participate, though we think with the benefits of a consolidating market and increased scale it is possible. If equity is not available, then the concern is that leverage is employed to make the acquisition which would impair the balance sheet. WOM has a small broadband business so at least that segment of the acquisition would face less of a regulatory hurdle, though mobile would still be challenging. The positive effects of a much larger scale WOM with top mobile market share in Chile as well as a substantial fixed line business after the combination and synergies with product bundling in a more consolidated Chile telecom market could offset the negative impact of the higher leverage and ultimately result in a stronger credit profile.

• Mexico based Latin America telecom services provider America Movil (AMXLMM; Baa1/A-/A) started a JV in Chile, ClaroVTR, in 2022, increased its stake to 91% October 2024 and in July 2025 acquired the balance to gain 100% ownership. America Movil saw the benefits of being able to bundle Claro’s mobile services with VTR’s broadband capabilities. It seems TMC would offer more of the same, though on a much larger scale now. ClaroVTR already has 20.9% of the mobile market which would jump to 44% after the combination and leap to the number one spot ahead of Entel’s 33%. In broadband, ClaroVTR already has the largest market share at 28.9% so with TMC that leaps to 57% compared to Mundo with 20% and Entel with about 10%. America Movil’s interest in the broadband assets may have been what caused an end to the alliance with Entel in jointly acquiring TMC, according to Diario Financiero, as it was previously thought they only had interest in the mobile assets and Entel would take broadband. America Movil has the balance sheet capacity, and this would be a relatively small acquisition for them but there would be significant regulatory hurdles.

• Entel (ENTEL; Baa3/BBB-/BBB-) has a leading 33% market share in mobile already, so the regulatory challenges would be even greater and the benefits of an acquisition less compelling. Entel sold its Fiber optics business for USD358mn in 2022 to On*Net Fibra and signed a long-term wholesale usage agreement as a means of having access to the business with less capex reflecting a change to an “asset light” model. In the JV with America Movil, it was thought that Entel would have interest in the broadband assets, though that would reverse their asset light strategy which leaves us with some doubts. The company has less financial flexibility than America Movil. Moodys recently moved its outlook from negative to stable on the ‘Baa3’ rating, citing improved leverage to 2.8x as of June 2025 and expected to decline to 2.5x by year end. Adding USD1bn of debt would lead to gross debt leverage estimated at 5x which would likely lead to a loss of IG ratings. You can see from the behavior of ENTEL bonds that the market does not think this combination is likely as ENTEL 32s were quoted T+105bp, the tightest spread levels for the past year. Bonds widened out 25bp to T+137bp in the following weeks after the non-binding JV agreement with America Movil to bid for TMC was announced but have since snapped back in.

• One last remote possibility is that a foreign competitor enters the fray. We posted back in June 2025 about U.S. based Verizon being granted a public telecommunications service concession in Chile that authorizes the company to offer Voice over Internet service for up to 30 years. Verizon has a new CEO as of two months ago who is already making big changes domestically to cut costs to enable more competitive pricing. It’s likely that he would be focused in the short term on fixing the U.S. business before venturing abroad.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

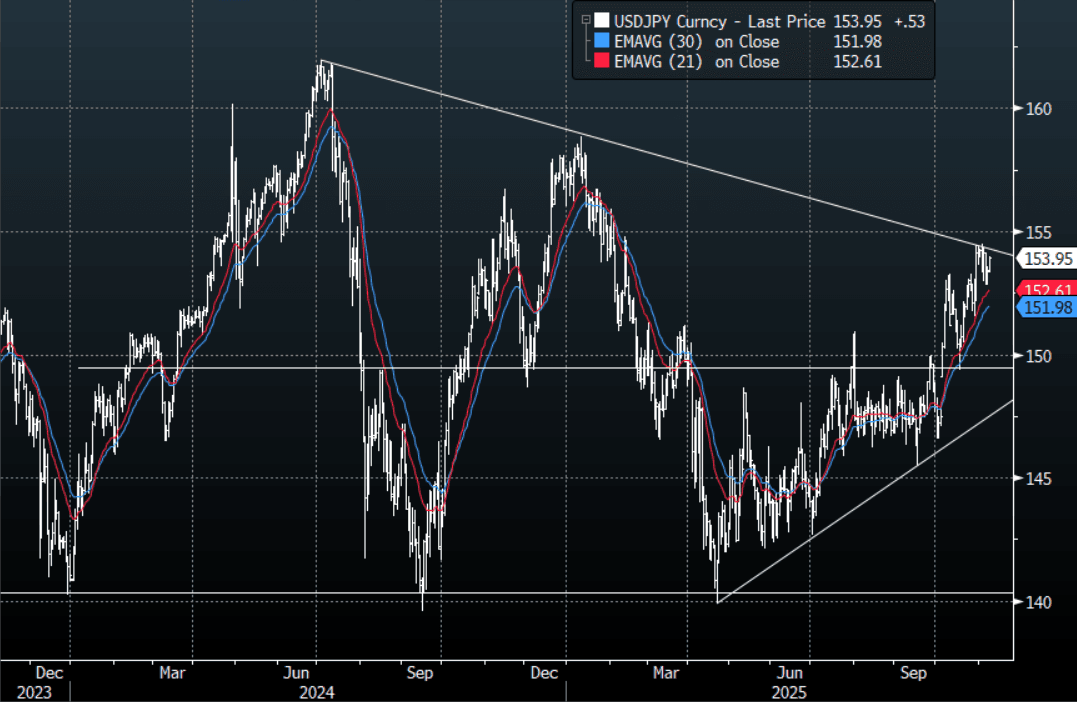

JPY: USD/JPY - Gaps Higher On Positive Shutdown Report

The Friday night range was 153.01 - 153.59, Asia is currently trading around 153.95, +0.35%. The pair has gapped higher on the Asian open as reports of a potential deal on the US shutdown make the rounds, reversing the short-term negative market sentiment on risk. USD/JPY found solid demand around the 153.00 area on Friday again, any confirmation of the shutdown ending would potentially see a knee-jerk higher in risk. In this scenario the focus would turn again to the resistance around the 154-155 area. A sustained break above here could potentially see the uptrend regain upward momentum as the focus would turn to the 160 area where I would start to become wary of intervention risks.

- Bloomberg reports, “ The LDP becomes more flexible in targeting budget surplus; CDP cites "fiscal discipline issues". On an NHK program on the 9th, LDP Policy Research Council Chairman Takayuki Kobayashi said, "Rather than being fixated on a single-year balance, we need to think about it a little more flexibly" regarding the target of achieving a primary balance surplus, an indicator of fiscal soundness.”

- Nikkei says, "Japan seeks to boost investment with upcoming economic stimulus. Japan's economic stimulus package is set to include tax cuts to spur investment focused around 17 key industries, including AI and semiconductors, and multi-year budget allocations to make policy more predictable, the Nikkei newspaper reported.”

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

- Data/Event : Leading Index

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Unemployment Rate Forecast To Dip, Released Thursday

The focus of the week will be Thursday’s October jobs data. After the unemployment rate rose 0.2pp to 4.5% in September, the release will be monitored to see if there is some stabilisation as the data can be volatile on a monthly basis. Bloomberg consensus expects it to fall 0.1pp to 4.4% with new jobs up 20k and the participation rate stable at 67%. RBA Governor Bullock has advised to look at the data on a 3-month average basis.

- On Monday, RBA Deputy Governor Hauser speaks at 1030 AEDT on the Outlook for the Australian Economy. It can be watched here.

- Other RBA speakers this week include a fireside chat with Assistant Governor (Financial System) Jones on Wednesday at 0915 AEDT and with Assistant Governor (Business Services) McPhee on Friday at 0910 AEDT.

- Key surveys are also released this week with November Westpac consumer confidence on Tuesday, which may be down again following the RBA’s clear hold on 4 November and the higher Q3 CPI print.

- The October NAB business survey also prints on Tuesday. It has been gradually recovering with the price/cost components fairly stable. The employment component is likely to be monitored after the Q3 survey showed an increase in employment intentions.

- Q3 home lending is published on Wednesday and the value of loans is forecast to rise 2.6% q/q after 2.0% in Q2.

- November Melbourne Institute consumer inflation expectations are out on Thursday. The series has been running at a higher rate since mid-year at 4.6% compared with 4.1% for the first 5 months of 2025. October was 4.8%.

ASIA: Government Bond Issuance Today

- South Korea to Sell KRW1.5 tn 3-Year Bonds

- Bank of Korea to Sell KRW1 tn 91-Day Bonds

- South Korea to Sell KRW1.5 tn 3-Year Bonds

- Philippines To Sell PHP 7.5Bln 182D Bills (PH0000060394)

- Philippines To Sell PHP 7.0Bln 91D Bills (PH0000059917)

- Philippines To Sell PHP 7.5Bln 364D Bills (PH0000061350)