EM LATAM CREDIT: Tecpetrol: New 5-Year Fair Value

(B1/NR/BB-)

IPTs: N/A FV: 7.25% Area

• Argentina based oil and gas E&P company Tecpetrol mandated investor meetings ahead of the potential issuance of USD benchmark-sized, 144a/Reg S, senior unsecured 5-year notes. The use of proceeds will be for general corporate purposes including capital expenditures to expand unconventional production.

• TECPET 33s (WAL 6.2Y) were last quoted 7.12%, 22bp tighter since June 30th and 50bp tighter than new issue pricing January 2025. Amid the pessimism in mid-Sept for Argentina (ARGENT; Caa1/CCC/CCC+) bonds, TECPET outperformed with yields only climbing about 20bp to 7.37% and then quickly bounced back to 7.2% a week later.

• The market does not seem to price much Argentina risk into the TECPET valuation, though maybe it should as ratings are tied to the sovereign and in a prolonged downside scenario TECPET valuations would be more severely impacted. For that reason, we look to recently issued Brazil independent oil and gas E&P company Prio (PRIOBZ; Ba3pos/NR/BB*+) with 5-year notes quoted at 7.2%. TECPET should trade a bit wider due to its Argentina risk but that is offset somewhat by PRIO’s smaller production scale.

• Another good comp would be Pan American Energy (PANAME; B1/NR/BB-) with 2032s (5.5Y WAL) last quoted 7.14%. PANAME is a bit larger in terms of production scale at 222k/boed vs 190k for Tecpetrol and has a longer 19 years of reserve life vs 14 years for Tecpetrol. PANAME also is vertically integrated with substantial refining operations.

• We observe a relatively flat yield curve when looking at other Argentina energy companies such as YPF (YPFDAR; B2/B-/CCC+) and Vista (VISTAA; B2/NR/BB-).

• TECPET leverage is relatively low at about 1.5x but is expected to rise to 4.5x next year, according to Fitch, as a result of borrowing to fund investment in Argentina’s Vaca Muerta region but then is expected to fall back to 2x with EBITDA doubling by 2027. Tecpetrol is owned by conglomerate Techint

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Breaches Support At The 50- Day EMA

- RES 4: 1.2063 2.236 proj of the Feb 28 - Mar 18 - 247 price swing

- RES 3: 1.2000 Round number resistance

- RES 2: 1.1919/23 High Sep 17 / 2.0 proj of Feb 28 - Mar 18-27 swing

- RES 1: 1.1735/1820 20-day EMA / High Sep 23

- PRICE: 1.1701 @ 18:39 BST Sep 26

- SUP 1: 1.1646 Low Sep 25

- SUP 2: 1.1574 Low Aug 27

- SUP 3: 1.1528 Low Aug 5

- SUP 4: 1.1392 Low Aug 1 and bear trigger.

The trend theme in EURUSD is unchanged, it remains bullish and the recent pullback appears corrective. However, support at 1.1680. the 50-day EMA, has been breached. A clear break of this average would signal scope for a deeper retracement and expose 1.1574 initially, the Aug 27 low. For bulls, a resumption of gains would refocus attention on 1.1923, a Fibonacci projection. Initial firm resistance to watch is 1.1820, the Sep 23 high.

MACRO ANALYSIS: MNI US Macro Weekly: FedSpeak Reaffirms Range Of Cut Views (2/2)

While we heard the monetary policy views of 6 of 12 current FOMC voters this week, there were no real surprises. We go through all of the relevant FOMC communications in full in our Macro Weekly PDF.

- Chair Powell reiterated that policy is not on a preset course; Gov Bowman and Gov Miran reiterated their more-dovish-than-median views; Musalem and Schmid suggested only limited scope for easing; and Goolsbee eyed neutral rates 100-125bp lower but was “uneasy” with too much front-loading.

- Virtually of the week’s FOMC speakers noted labor market risks had begun to surface, but had varying concerns about inflation. To sum up:

2025 FOMC Voters:

- Powell Reiterates "There Is No Risk-Free Path", Policy Not On Preset Course (Sep 23)

- Gov Bowman: Concerned Will Need Faster And Bigger Cuts (Sep 23)

- St Louis's Musalem: Limited Room For Easing, Policy May Be Close To Neutral (Sep 22)

- Chicago's Goolsbee Eyes Neutral Rates 100-125bp Lower (Sep 23), Uneasy With Too Much Cut Frontloading (Sep 25)

- Gov Miran: Appropriate Rates In 2.00-2.50% "Ballpark" (Sep 22)

- KC Fed's Schmid: Slightly Restrictive Policy The "Right Place To Be" (Sep 24)

Non-2025 Voters:

- Atlanta's Bostic Pencils In No More Cuts this Year, But Watching Data (Sep 22), Longer-Run Dot Suggests Limited Impetus To Cut Further (Sep 23)

- SF's Daly: Likely Further Cuts Will Be Needed To Support Labor Market (Sep 24)

- Cleveland's Hammack: Policy Very Mildly Restrictive, Concerns On More Cuts (Sep 22)

- Dallas's Logan: Time To Move From Fed Funds Policy Rate To Tri-Party Repo (Sep 25)

- Barkin: Jobs Shakier, Inflation Less Troubling (Sep 26)

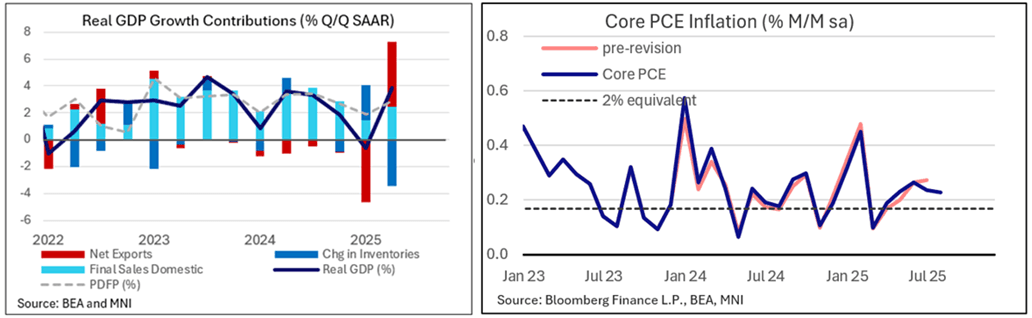

MACRO ANALYSIS: MNI US Macro Weekly: Too Solid For Comfort (1/2)

We've just published our US Macro Weekly - Download Full Report Here

- The US economy now appears to be on more solid footing than it seemed a week ago. Versus 45bp in Fed rate reductions through the remainder of 2025 as of last Friday, futures markets now price 40bp. Half of that retracement came Thursday at 0830ET, when Q2 GDP data, initial jobless claims, durable goods orders, and goods trade data all pointed to stronger ongoing GDP growth than previously anticipated.

- Q2 GDP growth was revised up significantly in the 3rd and final reading, to 3.84% Q/Q SAAR from 3.29% in the 2nd reading (consensus had expected this to be unchanged in the 3rd).

- And while that’s in the past, the latest monthly data saw the Atlanta Fed's GDPNow estimate for Q3 jump to 3.9% from 3.3% last week.

- Friday’s PCE data suggested solid consumption dynamics through August (and no nasty surprises in the core inflation data).

- As such, the week’s data almost unambiguously portrayed a better domestic demand story through – and beyond – a volatile first half of the year related to tariff policy shifts.

- That poses something of a quandary for a Fed that has shifted its sights to labor market risks. GDP is not employment, but a case for rate cuts at a time when inflation is still pushing 3% is tougher to make when the economy is growing at close to a 4% real pace and equities remain at or near all-time highs.

- October's cut is no longer such a sure thing as it seemed after the September meeting, with a 25bp ease now priced at 21bp (~84% implied prob), versus closer to 23bp (90+%) at the end of the prior week.