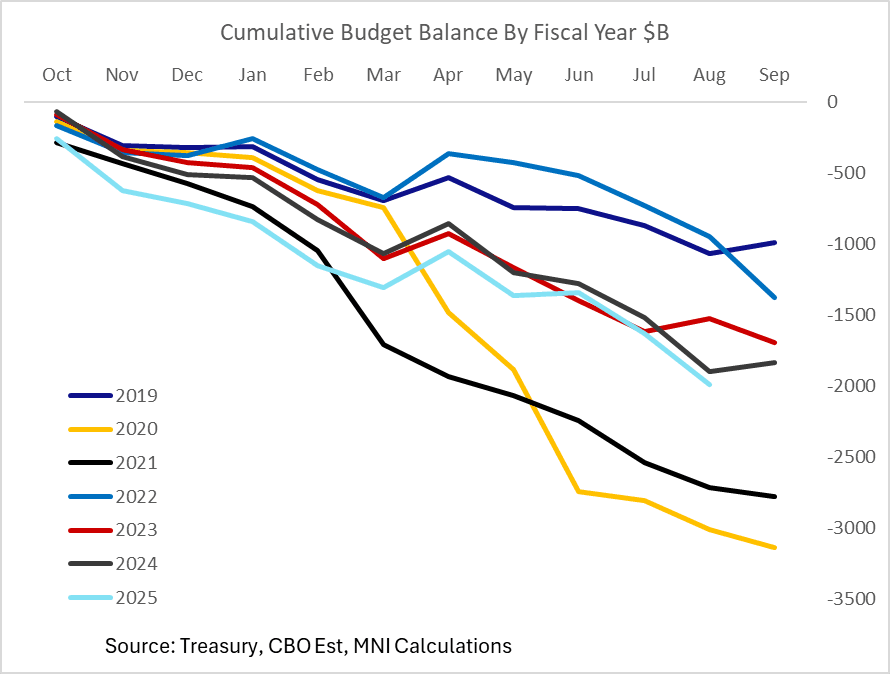

US FISCAL: Tariffs Partially Offsetting Deficit Expansion So Far

With one month remaining in the fiscal year (Oct-Sep), the Congressional Budget Office is estimating a cumulative deficit of $1.989T through August, including a $360B deficit for August itself. That's about $92B above last year's cumulative total to this point. While the Treasury's official August tally will only be released Thursday at 2pm ET, the CBO's estimate is usually very close to the mark.

- When accounting for timing shifts in outlays, however, the deficit is only about $11B bigger than it was at this point.

- Year-to-date, accounting for timing shifts, outlays are up 5% for a total $310B Y/Y in the 11 months through August, of which $223B is mandatory spending and $72B is net interest on the public debt. The estimate is flattered to the downside by a $110B fall in Department of Education outlays, about half of which is related to adjustments to student loans. And FDIC outlays fell $63B, vs 2024 which was hit by bank failures in the wake of the Silicon Valley Bank debacle.

- And in terms of timing-adjusted receipts, they're up $299B Y/Y in the fiscal year-to-date, or 7%. While corporate taxes are a little lower (largely due to timing shifts), individual income taxes are up 8% ($181B) - and "other receipts" soared 45% ($102B).

- It should be no surprise that within that category, customs duties made up $95B (+137% Y/Y) of that total, marking a $165B total for the fiscal year so far, in the wake of the Trump administration's tariff increases.

- The deficit is still tracking above most analyst expectations we've seen of $1.8-1.9T (was $1.83B in FY2024), though September tends to be a mixed month in terms of net outlays and there is of course the new monthly boost of tariffs (not including any negative dynamic effects on growth from said tariffs). We will get more details after the official Treasury statement expected Thursday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: UBS Above Consensus For Core CPI In July

- UBS see core CPI at a seasonally adjusted 0.35% M/M in July, a little above consensus of 0.3% or MNI unrounded 0.32% and top of the unrounded analyst estimates we've seen to date.

- They see core goods inflation accelerating to 0.38% M/M after 0.2% M/M in June, but largest increases set for subsequent months with 0.6% in Aug, 0.76% in Sep and 0.73% in Oct.

- They see core services inflation accelerate from 0.25% to 0.35% M/M, led sequentially by lodging away from home and airfares.

- On latest Adobe data: “In July this year the Adobe DPI declined more than in the same month last year, but less than in July 2023 and the five years prior to the pandemic. That moderately strong, but not booming, price change has been a recent theme in the Adobe data. Nonetheless, moderately strong increases add up: Since the implementation of the China tariffs in early February the Adobe DPI has declined less than in similar 6-month periods in any year in its 12-year history except for the start of the inflation surge in”.

USDCAD TECHS: Shallow Bounce Off Lows

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3792 @ 15:33 BST Aug 11

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD remains subdued, despite the shallow bounce Friday feeding through to further gains on Monday. This follows the weaker-than-expected jobs data last week. The pair remains notably lower on the week on the back of last Friday’s USD weakness. Initial firm support has been breached at the 1.3737 20-day EMA, a break below which would resume the correction off the early August high at 1.3879. On the recent run higher, price traded through the 50-day EMA at 1.3744, which aided the rally. This week’s price action, however, has cancelled that bullish threat and returned focus lower. The 100-dma becomes a key pivot point at 1.3824 last.

US TSYS: Leaning Bull Flatter Ahead Of CPI

The Treasury curve leaned bull flatter Monday ahead of Tuesday's CPI release.

- With no key data or Fed speakers on Monday's schedule, and looming CPI being the week's most impactful release, trading was relatively subdued and focused more on geopolitical developments.

- That included anticipation of the Trump-Putin meeting later this week per the Ukraine conflict, and the China tariff truce which was due to expire Tuesday (but per CNBC has been extended by 90 days as widely expected).

- In contrast to last week's reports which drew a small but notable reaction (namely firming the USD), there was little reaction to a Bloomberg report that current FOMC members Vice Chair for Supervision Bowman, Vice Chair Jefferson, and Dallas Fed's Logan are in the running to succeed current Fed Chair Powell.

- Indeed Bowman's comments over the weekend re eyeing 3 rate cuts by year-end were largely taken in stride as she's been a vocal (and dissenting) dove in recent months.

- Implied Fed funds were unchanged through year-end, still eyeing 57bp of cuts. Tsy yields traded within Friday's ranges overall, with volumes light (725k TYU5 contracts traded through 3:45ET)

- As noted, Friday sees a busier schedule including CPI - MNI's preview is here. Consensus sees core CPI inflation at 0.3% M/M and unrounded analyst estimates broadly echo this with a median 0.32% M/M. We also hear from Fed's Barkin (non-2025 voter) and Schmid (2025 voter, hawk) after CPI, with other data including the NFIB small business survey and the Federal budget statement.

- Latest levels: The 2-Yr yield is down 0.4bps at 3.758%, 5-Yr is down 0.7bps at 3.8242%, 10-Yr is down 1.2bps at 4.2713%, and 30-Yr is down 0.9bps at 4.8403%. Sep 10-Yr futures (TY) up 1.5/32 at 111-28 (L: 111-25 / H: 112-0-)