US DATA: Tame Headline CPI Belies Core Distortions, Food/Energy Divergence

Dec-18 17:51

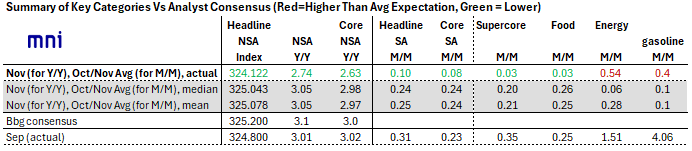

Headline inflation came in softer than expected across monthly average and Y/Y measures in the November (and partial October) report, but caveats abound.

- As noted it appears that the November aggregate indices were downwardly biased by distortionary housing CPI readings for November (even if, as we note, it will never be known whether the bias was to the upside or the downside given October's data will never be collected).

- That being said, the 2.74% Y/Y reading for November was well below the 3.05% expected, with the downside being driven by the downside miss to core (2.63% vs 3.05%) which in turn will have incorporated the questionably soft housing figures.

- Headline CPI came in around 0.10% M/M on average in Oct and Nov (2-month rise was 0.20%). Both food and energy inflation softened on an average M/M pace compared with September though dynamics vs expectations varied.

- Energy prices printed an average 0.54% M/M in Oct/Nov (rose 1.08% between Nov and Sep), down from 1.5% in Sept but well above the 0.06% expected.

- The BLS did provide monthly gas prices which showed a 2.1% M/M drop in October reversed and then some in November at +3.0% (after 4.1% in Sept), suggesting that the upside momentum for energy as a whole occurred in November. However, based on gas prices so far in December, this should pull back considerably in the next report.

- Food prices were basically flat between September and November however, rising by a total 0.06% for a 0.03% M/M monthly average. That's well below the 0.2% average expected and the 0.35% printed in September. The underlying indices suggest -0.11% M/M average deflation in grocery prices and +0.23% rises in food away from home, the latter indicating some upside momentum after a recent pullback.

- That alone could have upside implications for the core PCE readthrough from this report (as CPI food away from home is included in that PCE services category). For instance, Morgan Stanley have lowered their core PCE forecast to 0.13% M/M Oct-Nov average vs 0.28% pre-CPI, although that's still above the 0.08% M/M seen today for core CPI.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USDJPY Continues Ascent to Fresh Cycle Highs

Nov-18 17:47

- USDJPY continues to extend higher late Tuesday, with the bounce for equities off the lows and a move higher for US yields supportive. Following the sharp move lower for equities after the US cash open, USDJPY traded in a resilient manner, with the 155.00 handle providing solid support. The next technical target of 155.53 (a Fibonacci projection) has been met and cleared, and there appears little in the way of this trend reversing course.

- We noted earlier how the Japanese yen has been proving immune to the recent weakness for major equity benchmarks and the more forceful verbal warnings from Japanese officials on one-sided adjustments for the currency.

- Furthermore, the ongoing tensions between Japan/China, disappointing Q3 GDP data and fiscal related uncertainty continues to provide a pessimistic domestic backdrop.

- The next level on the topside for USDJPY is at 155.89, the Feb 3 high, however, more meaningful resistance is at 156.75, the Jan 23 high.

- Japan National CPI data for October is scheduled Friday local time.

US STOCKS: Midday Equities Roundup: Weaker But Off Lows, Tech Stocks Lagging

Nov-18 17:35

- Major US equity indexes remain weaker but off lows at midday Tuesday, a general risk-off tone ahead of Nvidia's eagerly awaited Q3 earnings after tomorrow's close. Currently, the DJIA trades down 633.34 points (-1.36%) at 45951.26, S&P E-Minis down 72.75 points (-1.09%) at 6618.5, Nasdaq down 349.9 points (-1.5%) at 22354.33.

- Chip makers led declines in the first half followed by Consumer Discretionary names:

- Western Digital -6.33%, Micron -5.12%, Advanced Micro Devices -4.22%, Microsoft -3.41% and NVIDIA -2.27%.

- Amazon -4.23%, Home Depot -4.15%, Best Buy -1.70% and Lowe's Cos -1.63%.

- Meanwhile, Health Care and Consumer Staples sector shares led advances at midday:

- Medtronic +5.95%, Merck +4.26%, Dexcom +3.25%, Biogen +3.16% and Gilead Sciences +1.96%.

- Archer-Daniels-Midland +2.16%, Bunge Global +1.93%, Hershey +1.91% and Philip Morris International +1.81%.

- Larger names yet to announce earnings this week include: Target Corp, Valvoline Inc, Lowe's Cos, Williams-Sonoma, TJX Cos, NVIDIA, Palo Alto Networks, Jacobs Solutions, Bath & Body Works, Walmart, Copart, Gap, Intuit, Ross Stores and BJ's Wholesale Club.

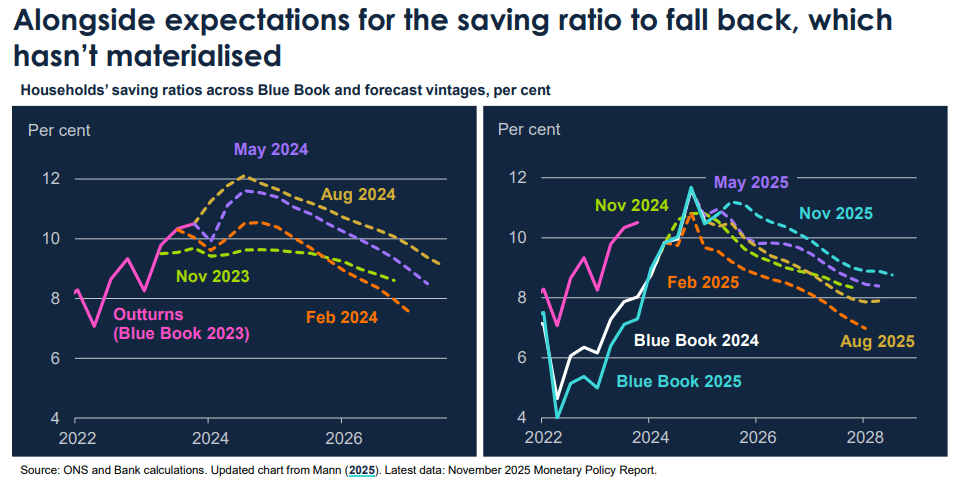

BOE: Dhingra Slides Maintain Clearly Dovish Stance

Nov-18 17:20

There don’t look to be any surprises in BoE Dhingra's presentation, being the most dovish MPC member. Some highlights from her slides:

- Consumption growth has been consistently weaker than forecast

- The expected falling back in the saving ratio has failed to materialise

- Microdata points to disposable incomes being just as weak as consumption

- Spending microdata suggests household costs are less optimistic regarding a real wage recovery

- Only interest income has grown consistently during the “consumption puzzle period”

- The financial counterpart of savings shows a paying down of debts rather than an accumulation of liquid assets for future consumption

- And deposits have been stable except for the top quintile of households