ASIA STOCKS: Taiwan Outflows Persist, Can Malaysian Inflows Pick Up Further?

Yesterday saw more outflow pressures than inflows for the EM Asia Pac region. Taiwan net outflows continued, with the past 5 days now seeing outflows of more than $4bn. Trends in local stocks reflect a buy on dips mentality, although the TWSE hasn't been able to sustain moves back above 28000 at this stage (which marked recent cycle highs at the start of the month). Taiwan will soon be back at YTD outflows if current trends persist. For South Korea we did see modest inflows yesterday, but it is too early to say if this is the start of a turnaround. Indeed early trends today, per the BBG NBUY function, are for offshore net selling (over $200mn). We did see US tech related equity trends falter in Tuesday trade, although the Kospi is still up close to 1% so far in Wednesday trade. US equity futures are also higher.

- Elsewhere, the recent see-saw pattern in Indian flows continued, with the 5-day sum back close to flat. Onshore equity sentiment looks more positive, although we are still a little distance from late Oct highs above 26k for the Nifty. Focus remains on any US-India trade deal announcement.

- In South East Asia, positive Indonesia inflow momentum slowed somewhat. Malaysia saw positive trends yesterday and with the Malaysian Prime Minister upbeat on local growth prospects, we could see firmer trends for local stocks. Note in the past trading month we have seen over $350mn in net outflows, so there is ample scope for a pick up in the period ahead.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 64 | -3424 | -1697 |

| Taiwan (USDmn) | -516 | -4199 | 497 |

| India (USDmn)* | -568 | -76 | -16456 |

| Indonesia (USDmn) | -39 | 113 | -2332 |

| Thailand (USDmn) | -75 | -140 | -3164 |

| Malaysia (USDmn) | 48 | 54 | -4179 |

| Philippines (USDmn) | 12 | 108 | -661 |

| Total (USDmn) | -1074 | -7566 | -27991 |

| * Data Up To Nov 10 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

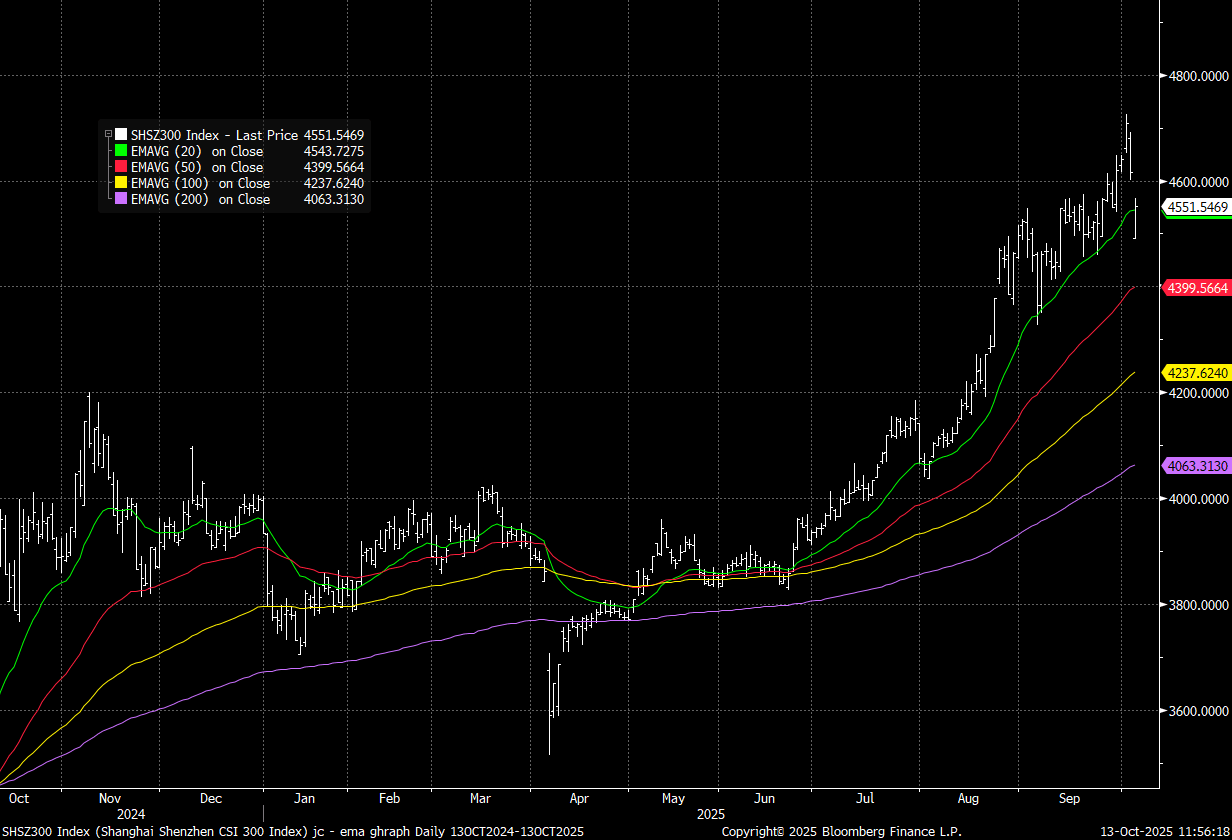

CHINA STOCKS: 20-day EMA Support Challenged, Onshore Media Confident In Outlook

China equity markets have opened up weaker amid renewed US-China trade tensions, but we sit up from early lows. Some higher beta/tech sensitive markets are challenging their respective 20-day EMA support points. This follows though a very strong run higher in recent months. Onshore media continued to express confidence in the outlook. Via BBG: "There’s no need to be “overly pessimistic” about China’s A-share market as its medium-term momentum remains intact despite external shocks, Shanghai Securities News reported Monday, citing brokerages."

- Weakness today builds on losses from Friday, which came prior to the latest Trump tariff threat. Sentiment was weighed then by concerns around export controls in the tech sector, along with valuation concerns.

- Losses in the CSI 300 were close to 3% at one stage but have since been pared (now back closer to 1.35%). We dipped below the 20-day EMA but have since recovered (see the chart below). For higher beta plays, like the Chinext, we are still under the equivalent support point. This index is still down around 2% at this stage.

- The language used by US officials (including US President Trump) suggests scope to negotiate ahead of the Nov 1 deadline for new tariff rates to come into effect. An off-ramp to the 100% tariff threat will be eyed, while Trump's threat on export controls on critical software could also impact China tech related sentiment.

Fig 1: CSI 300 Supported Under 20-day EMA Support Point

Source: Bloomberg Finance L.P./MNI

CHINA PRESS: Yicai Chief Economist Confidence Index Reached 50.3 In October

Yicai News Agency’s Chief Economist Confidence Index registered 50.3 points in October, down from 50.6 in September but remaining above the 50 point expansion threshold for the third consecutive month. Economists forecasted third-quarter GDP growth at 4.8% year-on-year, with expectations of a similar pace in the fourth quarter. For the full year, the average GDP growth projection remained at 4.8%. Regarding upcoming September economic data, participants projected CPI growth at -0.2% year-on-year, PPI at -2.3%, fixed asset investment growth at 0.0%, retail sales of consumer goods up 3.1% and industrial value-added up 5.1%. Analysts agreed that the probability of adjustments to the Loan Prime Rate (LPR) or the reserve requirement ratio (RRR) in October remained low, suggesting a steady monetary policy stance in the near term.

CHINA PRESS: China Not Banning Rare Earth Exports - MOFCOM

China’s recent trade measures concerning certain rare earth products does not constitute an export ban and applications that meet the relevant requirements will be approved, a spokesperson for the Ministry of Commerce stated. According to the spokesperson, China notified all relevant countries through its bilateral export control dialogue mechanism prior to the announcement. The spokesperson further noted the potential impact of the measures on global supply chains would be minimal.