TARIFFS: Taiwan Offs. Travelling To US To Advance Tariff/Chip Deal - Bloomberg

Jan-14 17:14

MNI London: Bloomberg News reports : https://www.bloomberg.com/news/articles/2026-01-14/taiwanese-of...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $1B Willis North America 2Pt Launched

Dec-15 17:08

- Date $MM Issuer (Priced *, Launch #)

- 12/15 $1B #Willis North America $700M +5Y +85, $300M +10Y +98

- 12/15 $550M Perimeter Holdings 8NC3

OPTIONS: Larger FX Option Pipeline

Dec-15 17:06

- EUR/USD: Dec17 $1.1700(E1.2bln), $1.1750(E1.2bln), $1.1800(E1.5bln); Dec18 $1.1550(E1.9bln), $1.1600(E1.3bln), $1.1750(E2.6bln), $1.1797-00(E1.2bln); Dec19 $1.1650(E1.1bln), $1.1675-80(E2.0bln), $1.1750(E1.7bln), $1.1785-00(E4.2bln), $1.1900(E2.0bln)

- USD/JPY: Dec18 Y155.00($3.0bln), Y156.00($3.1bln), Y156.25($2.3bln), Y157.00($4.0bln), Y158.00($4.8bln), Y158.50($1.9bln), Y159.00($6.5bln); Dec19 Y155.00($2.0bln)

- EUR/GBP: Dec19 Gbp0.8800(E1.3bln)

- AUD/USD: Dec18 $0.6540-50(A$1.6bln), $0.6665-75(A$1.3bln); Dec19 $0.6675(A$1.1bln), $0.6700(A$1.6bln)

- AUD/NZD: Dec17 N$1.1410(A$1.5bln)

- USD/CAD: Dec19 C$1.3800($940mln), C$1.3825($1.7bln), C$1.3900($1.7bln), C$1.3950($1.2bln)

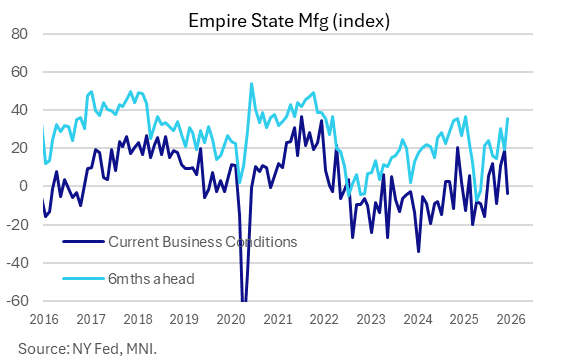

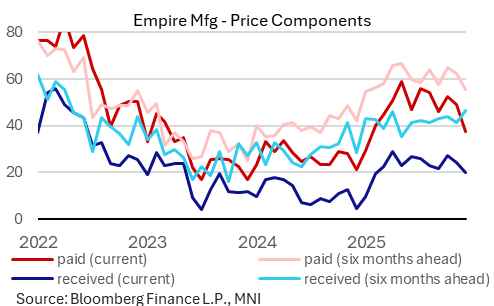

US DATA: Empire Manufacturing Activity Weaker, But Inflation Signals Mixed

Dec-15 17:05

Manufacturing activity in the greater New York region unexpectedly pulled back in December, per the Empire State Manufacturing Survey's General Business Conditions index dropping to -3.9 from 18.7 prior. That compares to a positive 10.0 expected, and November's reading which was one of the highest in the last 3 years. This starts the month's regional Fed surveys on a cautious note in terms of activity, and while input price pressures are clearly moderating, expected future selling prices notably continued to tick up.

- The internals were mostly weaker, with New Orders notably plummeting to a 3-month low 0.0 (15.9 prior) but Employment ticking up to 7.3 after 6.6 for a 5-month high and one of the best readings since 2022 after 3 months of advances.

- The national ISM equivalent to this index reading would be 50.0, a 3-month low and suggestive of flat activity, with Shipments, Delivery Times and Inventory Levels also slipping.

- The 6-month ahead index however jumped to 35.7 from 19.1 for an 11-month high, suggesting that regional manufacturers are hopeful that the current lull is temporary.

- Inflation gauges were notably softer: current prices paid fell over 11 points to an 11-month low 37.6, with prices received and future (6-months) prices paid also falling.

- Intriguingly though, future prices received ticked up to a 44-month high, suggesting possible expectations that higher prices can be demanded of end-consumers. As such we wouldn't interpret the report as unambiguously disinflationary.