EU REAL ESTATE: Swiss Prime Site: Wider than Colonial

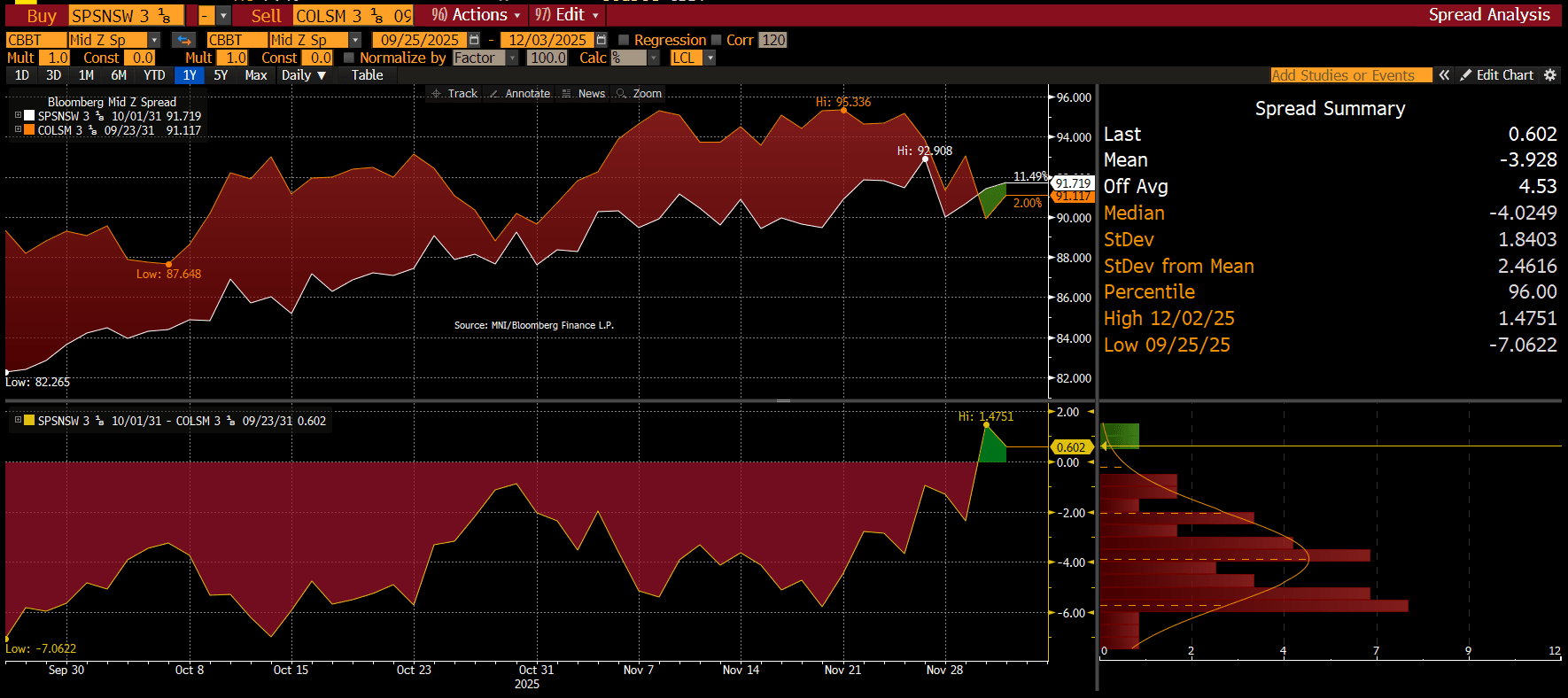

• SPSNSW 3.125 31 now screening slightly wide to Colonial COLSM 3.125 31

• A3 rated vs Baa1/BBB+

• SPSNSW equity is up 22% this year vs a flat performance from Colonial

• SwissPrime has a larger owned GAV of CHF 13.1bn (€14bn equiv) vs €11.9bn and also has a significant management arm.

• Swiss Prime's reported LTV comes in as closer to EPRA numbers. SwissPrime ~38.3% vs 47% for Colonial.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bullish Recovery

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4039/80 High Oct 24 / 16 and the bull trigger

- PRICE: 1.4022 @ 08:04 GMT Nov 3

- SUP 1: 1.3888 Low Oct 29 and key short-term support

- SUP 2: 1.3848 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3769 Low Sep 19

- SUP 4: 1.3727 Low Aug 29 and a bear trigger

A strong rally in USDCAD last week highlights a reversal of the corrective bear leg between Oct 14 - 29. Note that the climb suggests that a doji candle on Oct 29 is a valid reversal signal. The pair is also holding on to its latest gains - a bullish signal. A continuation higher would open 1.4080, the Oct 16 high and a bull trigger. Key short-term support and the bear trigger has been defined at 1.3888, the Oct 29 low.

SWITZERLAND: Light CHF Weakness After October Inflation Softer-than-expected

EURCHF is testing last Friday’s 0.92920 high following the lower-than-expected October inflation print (+0.15% since the data was released). EURCHF has been consolidating just above the 20-day EMA of 0.92780 over the past three sessions. A clear break of this average would expose the 50-day EMA at 0.93079.

- In front-end rates markets, the Dec ’26 SARON future is up ~1 tick since the data was released. Although markets price a ~50% implied probability of another cut across the next 12 months, the bar to a move back into negative territory in the short-term looks to be fairly high. SNB’s Tschudin said last week that it is ok if inflation moves below 0% for a "short time".

- Core CPI was 0.5% Y/Y in October, below the 0.7% consensus and prior. Headline inflation was 0.1% Y/Y (vs 0.3% cons, 0.2% prior). A reminder that the SNB’s latest conditional inflation forecast for Q4 2025 is 0.4%.

- Imported inflation looks soft again, falling 1.3% Y/Y (vs -0.9% in September, -1.3% in August). Food and non-alcoholic beverage inflation fell 0.5% Y/Y (vs -0.8% prior), while goods inflation was -1.6% for the second consecutive month. Although the CHF real effective exchange rate has weakened through the second half of October, the lagged impact of CHF strength since April still looks to be weighing on imported price pressures.

- Services inflation also softened relative to September, printing at 1.1% Y/Y (vs 1.4% prior). The volatile package holidays component looks to have played an important role though, rising 0.3% Y/Y (vs 4.8% prior).

GILTS: Opening Calls

Gilt Opening calls, 93.52/93.74.