FOREX: Sustainability of USD Move Will Depend on Yields Holding Below 4.00%

Oct-24 12:38

- Dollar resolves lower to following the gap pressure in US yields. No surprise to see EURUSD, GBPUSD to new daily highs but it's USDJPY that's posted a notable pullback: through overnight lows of 152.48 to reject the test of the mid-October highs at 153.27.

- Sustainability of this USD move will depend on US yields holding below 4.00%, but the move is sticking so far, with little signs of a fade and recovery back to unchanged.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: MNI POLITICAL RISK - Trump Continues Hawkish Pivot On Russia

Sep-24 12:35

Download Full Report Here

- President Donald Trump will receive an intel briefing in the morning before hosting a ‘Rose Garden Club’ dinner at 19:00 ET 00:00 BST.

- The White House is vetting Josh Sterling as a potential nominee for CFTC chair.

- Trump delivered a combative 57-minute speech to the UN General Assembly yesterday, arguing Western nations are collapsing due to poor leadership, uncontrolled immigration, and green energy commitments.

- Trump gave away little regarding foreign policy but signalled a possible route out of his dispute with Brazilian President Luiz Inácio Lula da Silva.

- Secretary of State Marco Rubio will continue UN engagements today with two meetings on Middle East security.

- The EU's chief trade negotiator will meet USTR Jamieson Greer this week to try to restart negotiations on metals tariffs.

- Trump cancelled a meeting with Democratic leaders, leaving no clear offramp to avert a government shutdown on October 1.

- Trump said Kyiv can regain all territory controlled by Russia, a major shift from the Trump administration’s long-held position that Ukraine must accept territorial concessions to facilitate a ceasefire agreement with Russia.

- Trump offered broad support for Argentinian President Javier Milei. Treasury Secretary Scott Bessent outlined US measures to stabilise the Argentinian economy.

- Iran’s Supreme Leader threw cold water on Tehran’s last-ditch attempts to avert the reimposition of UN sanctions this weekend.

- Poll of the Day: Trump is most negative on the issues Americans rate as the most important.

Full Article: US DAILY BRIEF

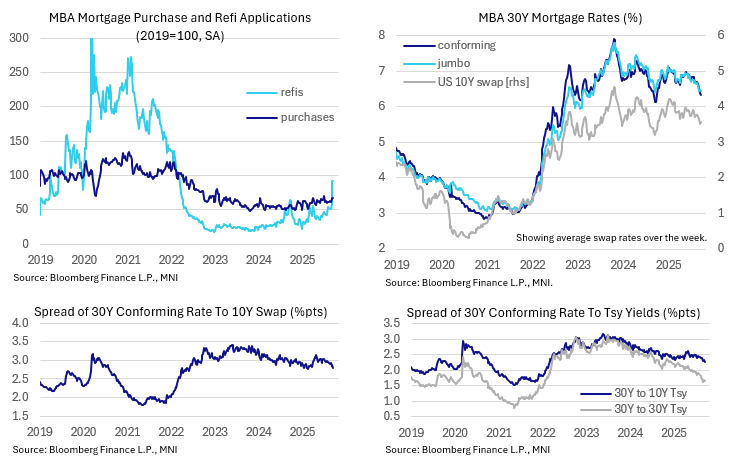

US DATA: Elevated Mortgage Refi Apps Steady W/W As Spreads, Rates Tick Lower

Sep-24 12:33

Mortgage application activity as measured by the MBA composite index was basically flat in the week of Sept 19, rising by 0.6% W/W after the prior 29.7% surge was the biggest since January. This is a refinancing story so far, similar to other periods seeing pullbacks in yields since 2023, with outright purchase activity remaining weak.

- Purchase applications rose 0.3% (2.9% prior) with refinancings up 0.8% (after 57.7%). While the previous week's surge didn't extend, the latest rise brought refinancing apps to fresh post-Q1 2022 highs, as homeowners clamor for the lowest rates seen since September 2024. The overall composite nudged up to its highest since May 2022.

- While the latest 5bp downtick in 30Y conforming rates to 6.34% didn't fuel much additional activity in the most recent week, that rate has now fallen 35bp in a month (6.69% week of August 22), alongside a 23bp drop in 10Y Treasury yields (average weekly basis) and 22bp for 30Y.

- The spread of the 30Y conforming mortgage rate to 10Y Tsys was 226bp in the latest week, down 7bp for the lowest since February 2022; to 10Y swaps it's the lowest since February this year.

- The spread of jumbo-to-regular 30Y rates has moved to its widest since February, at 10bp (jumbo = 6.44%), with the spread having been inverted over much of that period in jumbos' favor.

- The mortgage market is a long way from being outright supportive of residential activity, but it is headed in that direction. Note that the recent decline in yields and thus pickup in activity coincides with the Fed's Jackson Hole symposium at which Chair Powell signaled that the Fed would resume rate cutting (and did so at last week's meeting).

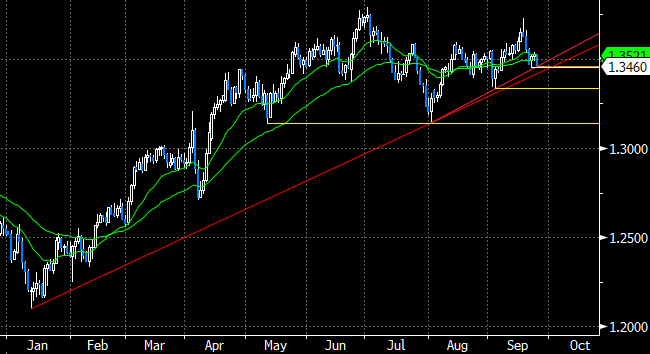

FOREX: GBPUSD Probing Trendline Support

Sep-24 12:20

- The dollar’s supportive tone continues to dominate currency markets on Wednesday, as markets digest the latest U.S. & Russia comments surrounding Ukraine. GBPUSD has reverted lower in sympathy, currently probing initial trendline support (drawn from the Aug 01 low) at 1.3458. Clearance of this line would strengthen a bearish threat and target a move towards key support which resides at 1.3333, the Sep 3 low.

- As a reminder, flash PMIs for September disappointed expectations on Tuesday, adding to the building negative sentiment following last week’s public sector net borrowing data and associated concerns around the upcoming budget.

- Goldman Sachs believe vulnerabilities in the UK labour market, the need for further fiscal consolidations, global cyclical risks and a challenging structural valuation picture still point to a gradual drift higher in EUR/GBP from here.

- The latest recovery for the cross paves the way for an extension towards the bull trigger at 0.8769, the Jul 28 high. Clearance of this level would strengthen the bullish theme.

Source: Bloomberg Finance L.P. / MNI