AUSTRALIA DATA: Surplus Widens But Trend Sideways

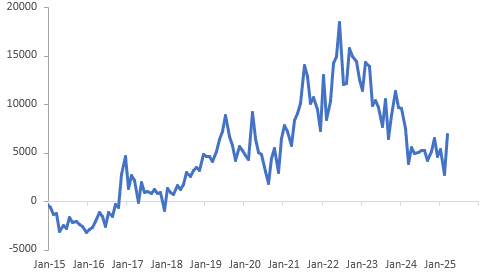

There was a $4bn widening in Australia’s merchandise trade surplus in March after narrowing $2.5bn in the previous month. The move to the highest surplus at $6.9bn in over a year was driven by a strong pickup in goods exports driven by Australia’s mining commodities, while imports contracted on the month. Through the volatility though, the trend in the trade surplus is steady.

Australia merchandise trade surplus A$mn

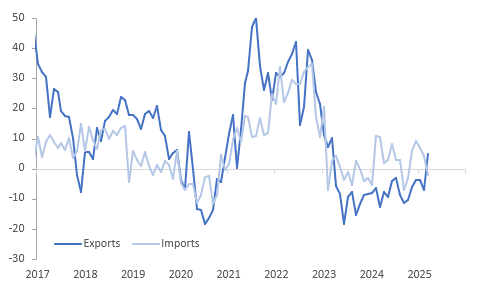

- Exports rose 7.6% m/m to be up 5.0% y/y, the first positive in two years. Non-rural goods rose 8.6% m/m, rural fell 8.5% m/m (weakness was broad-based) and non-monetary gold rose 25.9% m/m.

- Imports fell 2.2% m/m to be down 2.1% y/y after +4.2% y/y in February. The weakness was across major categories with consumer goods down 0.7% m/m & 3.3% y/y, capital goods -5.1% m/m & -10% y/y and intermediate -2.1% m/m & -0.4% y/y, possibly signalling continued subdued domestic demand.

- Food & clothing drove the drop in consumer goods, while vehicles rose 3.3% m/m. Machinery, telecoms equipment and other capital goods fell, while ADP equipment and industrial transport rose.

Australia goods exports vs imports y/y%

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: A$ Off Lows As Equities Recover & China PMI Rises

A$ has trended lower through most of the session as weaker risk appetite continued to weigh but is off its lows and bounced on the better-than-expected China Caixin manufacturing PMI after falls across much of Asia. AUDUSD is down slightly to 0.6245 after a low of 0.6232, while the USD index is little changed.

- February retail sales were slightly weaker than expected rising 0.2% m/m after 0.3% with annual growth moderating 0.2pp to 3.6%. Looking through volatility from seasonal discounting, retail spending is in line with rates seen since October.

- The yen and euro continue to benefit from weaker risk sentiment driven by tariff fears leaving AUDJPY down 0.2% to 93.52 but off today’s low of 93.27 and AUDEUR -0.1% to 0.5770 up from 0.5759. AUDGBP is 0.1% lower at 0.4832.

- AUDNZD is moderately higher today at 1.1009 and has spent most of the session above 1.1000 reaching a peak of 1.1010.

- Equities are mixed with the ASX up 0.4% and Hang Seng +0.7% but CSI 300 flat and S&P e-mini down 0.4%. Oil prices are moderately higher with WTI +0.1% to $71.56/bbl. Copper is up 0.5% but iron ore has fallen below $102/t.

- The RBA decision is announced at 1430 AEDT today followed by Governor Bullock’s press conference at 1530 AEDT. The bank is widely expected to leave rates at 4.10% after cutting 25bp at the last meeting (see MNI RBA Preview here).

- Later the Fed’s Barkin speaks on policy and the economic outlook. US final March manufacturing PMI, March manufacturing ISM, February JOLTS job openings and March Dallas Fed services print. The ECB’s Lagarde, Lane and Cipollone speak and European March manufacturing PMIs and euro area CPI are released.

AUSSIE BONDS: Little Changed Ahead Of RBA Policy Decision

ACGBs (YM flat & XM +0.5) are little changed after today’s data and before the RBA policy decision.

- February retail sales were slightly weaker than expected rising 0.2% m/m after 0.3% with annual growth moderating 0.2pp to 3.6%. Looking through volatility from seasonal discounting, retail spending is in line with rates seen since October but 3-month momentum has slowed. The pickup in consumer confidence from lower inflation & rates should support the upward trend in retail spending going forward.

- The RBA decision is announced at 1430 AEDT today followed by Governor Bullock's press conference at 1530 AEDT. The bank is widely expected to leave rates at 4.10% after cutting 25bp at the last meeting (see MNI RBA Preview here).

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest gains.

- Cash ACGBs are 1bp richer to 3bps cheaper with the AU-US 10-year yield differential at +20bps.

- Swap rates are 1bp lower.

- The bills strip is +1 to +2 across contracts.

CROSS ASSET: Watching Credit Spreads

US financial conditions are tightening, with most of President Trump's Agenda being bad for growth, outside of deregulation. These policies have the potential to have a bigger impact on asset prices than is being expected.

- Goldman’s has worryingly cut its S&P target for a second time this month and now expects the Index to end the year around 5700.

- Credit spreads which have been relatively well behaved to start the year are now starting to pay attention as the probabilities of stagflation increase.

- HY spreads are approaching the 400 level which in the past if broken has seen periods of extreme volatility and risk aversion.

- An acceleration through here would be a very bad sign for stocks and an indication of much lower levels from here.

- Foreign investors have accumulated huge amounts of US equities since 2010. We have already seen the start of a rotation back to Europe in particular, but this has the potential to gather in pace.

Fig 1: Credit Spreads - High Yield

Source: MNI - Market News/Bloomberg