AUDUSD TECHS: Support Remains Intact

Dec-30 07:53

- RES 4: 0.6976 2.00 proj of the Oct 13 - 27 - Nov 3 price swing

- RES 3: 0.6956 High Aug 30

- RES 2: 0.6909 76.4% retracement of the Aug 11 - Oct 13 downleg

- RES 1: 0.6801/6893 High Dec 28 / 13 and the bull trigger

- PRICE: 0.6777 @ 07:50 GMT Dec 30

- SUP 1: 0.6629 Low Dec 20 and key short-term support.

- SUP 2: 0.6585 Low Nov 21 and a key short-term support

- SUP 3: 0.6531 50.0% retracement of the Oct 13 - Dec 13 climb

- SUP 4: 0.6500 Round number support

AUDUSD is holding on to the bulk of its most recent gains. Support at the 50-day EMA - at 0.6677 - remains intact for now. A clear break of this EMA is required to suggest scope for a deeper pullback and 0.6629, the Dec 20 low, is seen as a key short-term bear trigger. A stronger resumption of gains would refocus attention on 0.6893, the Dec 13 high and the bull trigger. Clearance of this level would resume the recent uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Fade off their highs

Nov-30 07:52

- Equities are fading off their best levels, nothing big after the French CPI beat, just 8 points for Estoxx future.

- Bund test initial small support at 140.51.

FRANCE DATA: Bunds 40 ticks lower on French HICP data

Nov-30 07:51

- French HICP a tenth higher than expected - in contrast to the soft Spanish HICP print yesterday (and the German HICP print was largely also in line despite the soft national German CPI print).

- Bunds kneejerk lower by 40 ticks to 140.60 from around 141.00 ahead of the data.

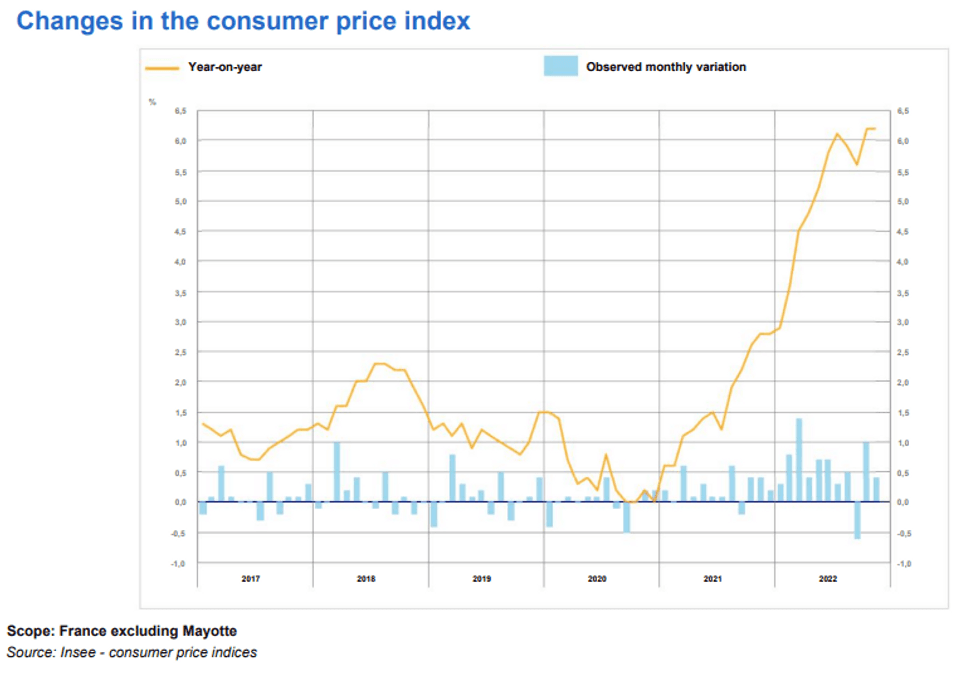

FRANCE DATA: CPI Holds Steady in November, Consumer Spending Dips

Nov-30 07:50

FRANCE NOV (F) CPI +0.4% M/M (FCST +0.3%); OCT +1.0% M/M

FRANCE NOV (F) CPI +6.2% Y/Y (FCST +6.1%); OCT +6.2% Y/Y

FRANCE NOV (F) CPI +7.1% Y/Y (FCST +7.0%); OCT +7.1% Y/Y

- French inflation rates remained buoyant in the November flash estimates, holding steady at +6.2% y/y (CPI) and +7.2% y/y (HICP).

- Some slowing was noted on the month-on-month figures, with CPI decelerating to +0.4% m/m from +1.0% m/m in October.

- Food and manufactured product prices are anticipated to have accelerated further, whilst service prices keep pace with October inflation rates.

- Despite fiscal support in the form of fuel rebates, energy prices recorded only a marginal deceleration on the year. However, on the month energy and manufactured goods saw some easing.

- Q3 GDP was confirmed to have expanded at a modest +0.2% q/q, whilst consumer spending data released this morning signalled a sharp October contraction (-2.8% m/m).

- This was the largest monthly dip since April 2021, underpinned by a fall in energy, manufactured goods and food consumption.

Trending Top

Apr-24 20:29