EURGBP TECHS: Support Remains Intact

- RES 4: 0.8865 High Nov 14 and a bull trigger

- RES 3: 0.8840 High Nov 20

- RES 2: 0.8818 High Nov 26

- RES 1: 0.8802 High Dec 2 and a key near-term resistance

- PRICE: 0.8773 @ 15:51 GMT Dec 19

- SUP 1: 0.8735/21 Low Dec 18 / 9

- SUP 2: 0.8706 76.4% retracement of the Oct 8 - Nov 14 bull leg

- SUP 3: 0.8670 Low Oct 21

- SUP 4: 0.8656 Low Oct 8 and a key support

The bull cycle in EURGBP that started Dec 9 highlights a possible reversal of the Nov 14 - Dec 9 corrective phase. Key short-term support has been defined at 0.8721, the Dec 9 low. A break of this level would signal scope for a deeper retracement,and open 0.8706, a Fibonacci retracement. Initial firm resistance to watch is unchanged at 0.8802, the Dec 2 high. Clearance of this hurdle would be a bullish development.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Again Despite Soft UK CPI

Gilts underperformed for a second consecutive session Wednesday.

- The short end outperformed on the UK curve as October CPI data on the soft side (headline, services, food inflation below BOE forecasts) appeared to open the door to a December BOE cut slightly wider.

- Gilts initially rallied though global dynamics and local fiscal/political concerns weighed and there was clear underperformance further down the curve. 10Y Gilt yields hit the highest levels in a month.

- A revived bid in equities about 2 hours before the European cash close saw core FI pull back, reversing nascent gains for Bunds.

- On the day the UK curve bear steepened, with Germany's twist steepening. Periphery/semi-core EGB spreads closed slightly tighter.

- Thursday's global focus will be the delayed US September nonfarm payrolls report, though we get varied European data as well including German PPI and Eurozone and UK (GfK) consumer confidence. We also get appearances by BOE's Mann and Dhingra.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 2.018%, 5-Yr is up 0.1bps at 2.294%, 10-Yr is up 0.5bps at 2.711%, and 30-Yr is up 1.3bps at 3.332%.

- UK: The 2-Yr yield is up 0.6bps at 3.806%, 5-Yr is up 2.8bps at 4.001%, 10-Yr is up 4.8bps at 4.602%, and 30-Yr is up 6.2bps at 5.448%.

- Italian BTP spread down 0.9bps at 74.2bps / French OAT down 0.5bps at 75bps

US TSY FUTURES: December'25-March'26 Roll Update

The latest Tsy quarterly futures roll volumes for December'25 to March'26 outlined below. Percentage complete gradually rising ahead the "First Notice" date of Friday, November 28. Current roll details:

- TUZ5/TUH6 appr 417,500 from -6.0 to -5.62, -6.0 last; 8% complete

- FVZ5/FVH6 appr 882,200 from -2.75 to -2.25, -2.75 last; 16% complete

- TYZ5/TYH6 appr 299,200 from 1.5 to 2.0, 1.75 last; 15% complete

- UXYZ5/UXYH6 180,100 from 5.25 to 5.75, 5.25 last; 6% complete

- USZ5/USH6 50,100 from 13.0 to 14.0, 13.0 last; 10% complete

- WNZ5/WNH6 appr 244,300 from 9.5 to 10.25, 9.75 last; 9% complete

- Reminder, Dec'25 futures don't expire until next month: 10s, 30s and Ultras on December 19, 2s and 5s on December 31. Meanwhile, Dec'25 Tsy options will expire this Friday, November 21

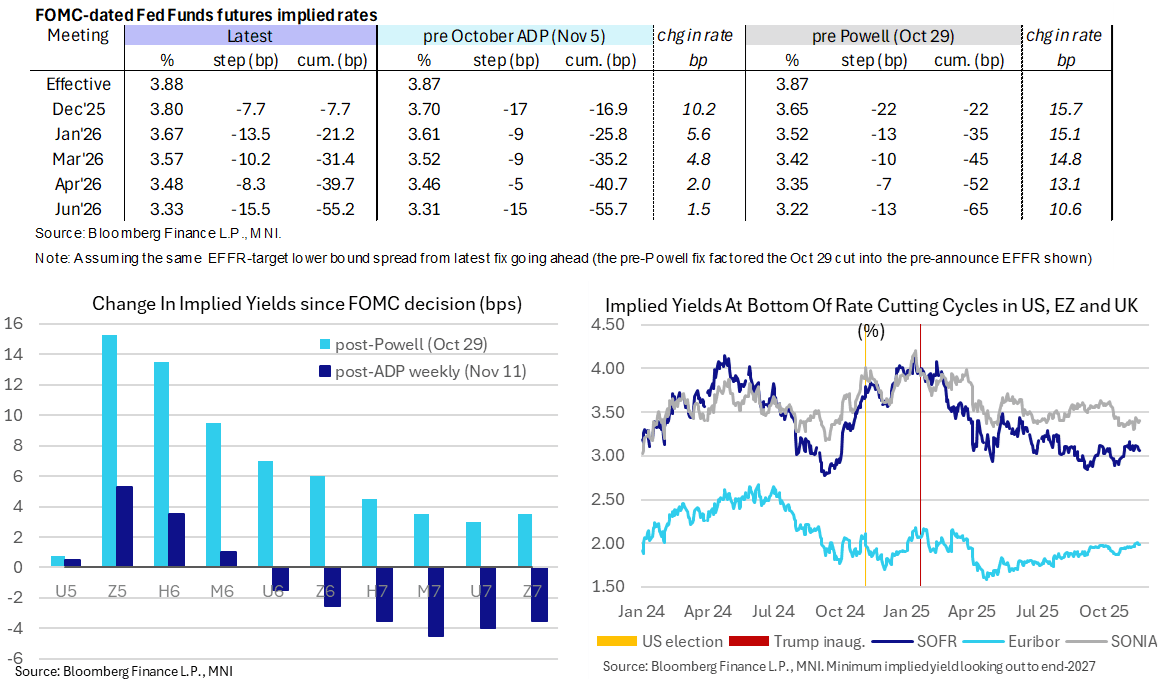

STIR: Fed December Cut Now Seen At 1/3 Likelihood After BLS NFP Rescheduling

- Updating a Fed Funds run after the BLS decision to not release an October payrolls report and instead bundle the establishment survey findings into the November report now due on Dec 16.

- Cumulative cuts from 3.88% effective: 7.5bp Dec, 21bp Jan, 31.5bp Mar, 39.5bp Apr and 55bp Jun.

- SFRZ5 still leads concentrated losses on the day, currently -0.0125 at 96.1775 vs 96.1975 pre-BLS headlines, but is paring the drop to an earlier low of 96.1650.

- There’s understandably little impact further out the curve, with small gains on the day from SFRU6 onwards. The terminal implied yield of 3.065% (SFRH7, -1bp) is at the low of the 3.065-3.16% range for closes seen in recent weeks.

- Whilst still somewhat of a surprise, it shouldn’t be have been fully ruled out, having warned in our data scheduling update at 1105ET that “MNI remains doubtful that the Fed will have nonfarm payrolls data for November (originally scheduled for Dec 5) by its December 9-10 meeting - particularly since the BLS backlog appears to be clearing only slowly, and the Thanksgiving holiday (Nov 27) approaches”.

- Rounding out labor releases from the BLS update, it will publish the October JOLTS report on Dec 9, day one of the two-day FOMC meeting.