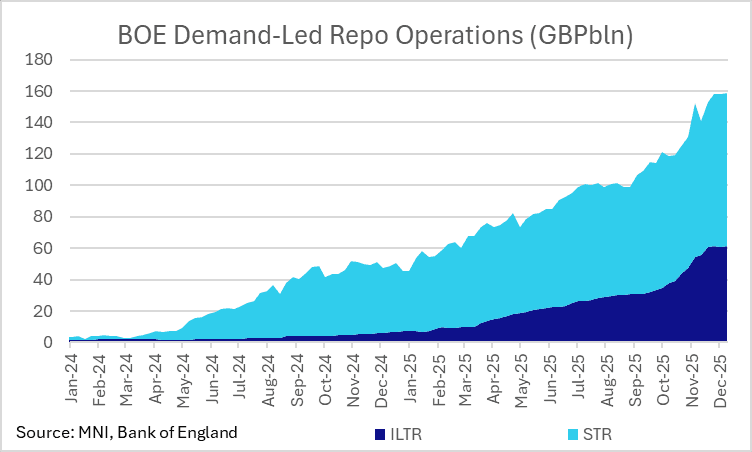

BOE: STR usage GBP0.1bln higher; BOE repo usage broadly stable for 3 weeks

Dec-04 10:43

- STR usage GB97.208bln (GBP105mln higher than last week) and follows ILTR usage increasing GBP625mln net on Tuesday.

- This puts BOE repo operation usage at GBP158.8bln, GBP730mln higher than last week and another record high.

- But big picture, usage of these operations is broadly unchanged for three consecutive weeks now.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BELGIUM T-BILL AUCTION RESULTS: TC Results

Nov-04 10:41

| Maturity | Feb 12, 2026 | May 14, 2026 | Oct 15, 2026 |

| Amount | E740mln | E844mln | E818mln |

| Target | E2.0-2.4bln | Shared | Shared |

| Previous | E1.002bln | E800mln | |

| Avg yield | 1.927% | 1.983% | 2.001% |

| Previous | 1.889% | 1.977% | 1.964% |

| Bid-to-cover | 2.73x | 3.33x | 2.89x |

| Previous | 3.09x | 2.22x | 1.91x |

| Previous date | Oct 14, 2025 | Oct 07, 2025 | Oct 14, 2025 |

GILTS: Off Highs After Reeves But Still Outperforming Bunds

Nov-04 10:39

Gilts continue to outperform core global FI peers after the UK media signalled the increased likelihood pf meaningful fiscal tightening in the UK.

- Chancellor Reeves didn’t provide any fresh detail, which saw gilts trade away from session highs.

- Still, her choice of phrases and omissions of manifesto pledges (there was no mention of avoiding hiking the big 3 taxes and no increases of taxes on working people) left the door open to meaningful alterations in the Budget later this month.

- Elsewhere, wider risk-off price action stemming from equity weakness in a couple of meaningful global tech names (Palantir & SK Hynix) provided cross-market support.

- Gilt futures traded as high as 93.98 before trimming gains to ~93.70 (+33).

- Next resistance at 94.00.

- Yields 2.5-3.5bp lower, curve flatter. October closing lows intact at this stage.

- Long 3-Year supply passed smoothly.

- SONIA futures flat to +4.0. October highs in SFIZ6 remain untouched.

- BoE-dated OIS is flat to 2bp more dovish on the day, showing 7bp of easing for this week’s meeting (which we deem to be a 50/50 decision), 17bp through December (vs. ~19bp at one point today) and 30bp through February.

- BoE’s Breeden will speak at Santander’s International Banking Conference. Note that the BoE is in its pre-meeting quiet period, so don’t expect her to comment on monetary policy. She will focus on financial stability and there will not be a text release.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.903 | -6.6 |

Dec-25 | 3.807 | -16.2 |

Feb-26 | 3.668 | -30.1 |

Mar-26 | 3.602 | -36.7 |

Apr-26 | 3.490 | -47.9 |

Jun-26 | 3.460 | -50.9 |

Jul-26 | 3.397 | -57.2 |

Sep-26 | 3.379 | -59.0 |

OUTLOOK: Price Signal Summary - Corrective Cycle In EUROSTOXX50 Futures

Nov-04 10:39

- In the equity space, the trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Attention is on support at the 20-day EMA, at 6804.03 (pierced). A clear break of this level average would signal scope for a deeper retracement and expose the 50-day EMA at 6698.11 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high.

- Short-term weakness in EUROSTOXX 50 futures is considered corrective. The contract has breached the 20-day EMA, signalling scope for a deeper retracement towards support at the 50-day EMA, at 5567.19. Support below the EMA lies at 5549.50, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Key resistance and bull trigger is 5742.00, the Oct 29 high.