US OUTLOOK/OPINION: Still Some Way For Full Tariff Impact To Show On Prices

Looking ahead to next week’s US CPI (Tue) and PPI (Thu) releases, latest monthly tariff revenue for July suggests we’re still some way off seeing the full impact from tariffs on prices.

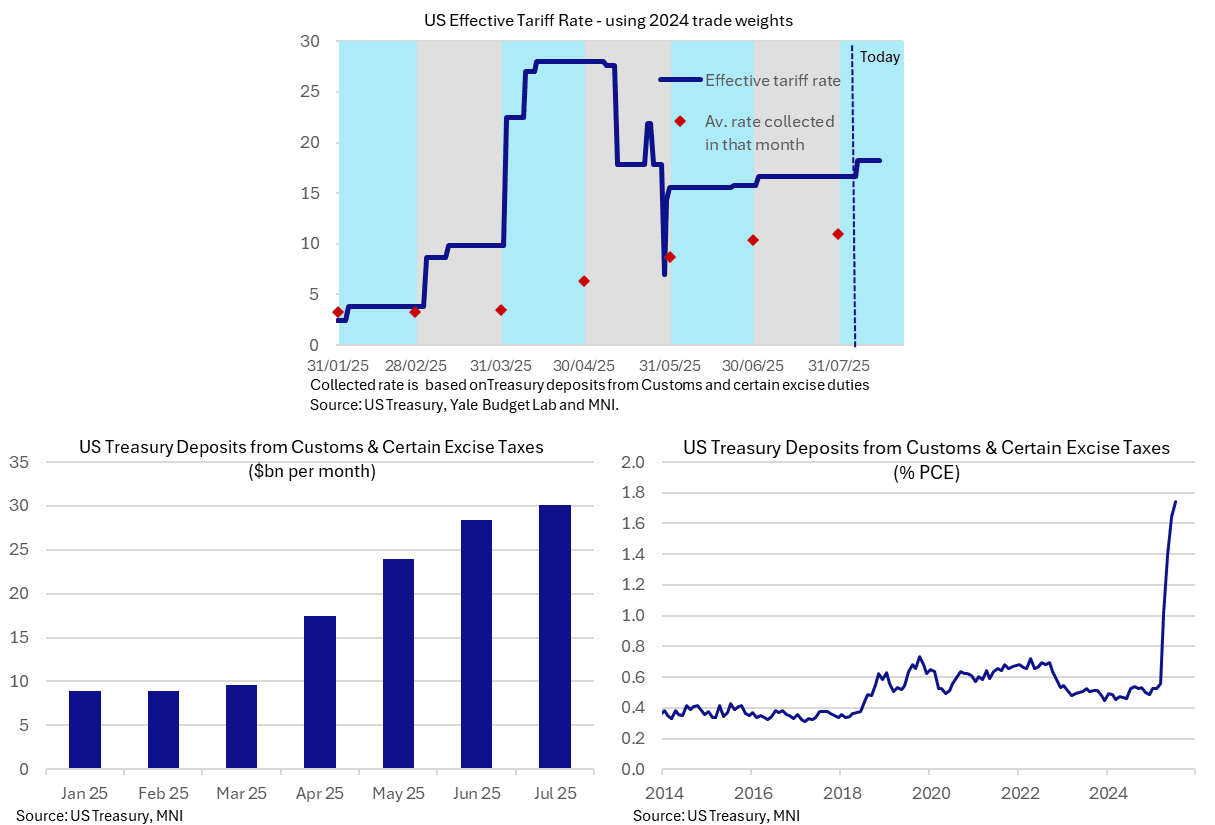

- The effective tariff rate currently stands at 18.3% according to Yale Budget Lab calculations (pre-substitution, i.e. keeping trade shares constant), up from 15.5-16% through June and 16.6% in July.

- In contrast, the $30bn of Treasury deposits from customs and certain excise duties in July was worth 11.0% of goods imports in 2024 (likely reflecting June average tariff rates suggesting further increases still to come). That’s up from 10.3% in June, 8.7% in May, 6.3% in April and 3.0% in Dec 2024 prior to the second Trump administration to give a sense of baseline.

- (Note that this 11.0% rate would be 10.3% if using a 12mth sum up to latest data for June owing to the sharp rise in imports in 1Q25. This dynamic approach with recent data can be misleading).

- Alternatively, these tariff revenues in July were worth ~1.7% of overall personal consumption expenditure, an increase of 1.3pp under the Trump administration.

- Of course, this doesn’t give insight into burden sharing across importers, businesses and consumers.

- On the former, June US import prices showed a partial correction stronger for those from China after what had looked like some taking of a tariff hit in April and May (implied by lower than usual import prices), but import prices more generally haven’t shown much concession. That’s in contrast to NEC Director Hassett saying on Aug 4 that data shows tariffs are being borne by foreign producers, although admittedly the extent to which they’re being borne is vague in that headline.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE: Incumbent Donohoe Confirmed As Eurogroup President For Third Term

The Eurogroup meeting of eurozone finance ministers has formally re-elected incumbent president, Ireland's Finance Minister Paschal Donohoe, for a third two-and-a-half-year term. Earlier today, Spain's Carlos Cuerpo and Lithuania's Rimantas Sadzius both confirmed the withdrawal of their bids to replace Donohoe, each stating that they did not have the required support to oust the incumbent. In late June, MNI's Policy team highlighted the threats to Cuerpo's run for the presidency posed by frustrations over a thwarted banking merger and anger among other European nations at Spain's intransigence on hitting elevated NATO defence spending targets.

- The Eurogroup president's duties include setting the agenda for meetings of finance ministers, drawing up the Eurogroup's long-term work programme, and representing the Eurogroup in international forums and to the European Parliament.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Jul09 $1.1700(E1.7bln); Jul10 $1.1650(E2.1bln), $1.1800(E1.3bln); Jul11 $1.1770(E2.0bln)

- USD/JPY: Jul09 Y144.00-10($1.4bln); Jul10 Y143.95-15($1.0bln), Y144.70-90($1.3bln)

US 10YR FUTURE TECHS: (U5) Monitoring Support At The 50-Day EMA

- RES 4: 113-07 76.4% retracement of the Apr 7 - 11 bear leg

- RES 3: 112-23 High May 1 and key resistance

- RES 2: 112-12+/15 High Jul 1 / 61.8% of the Apr 7 - 11 sell-off

- RES 1: 111-28 High Jul 3

- PRICE: 110-31+ @ 16:08 BST Jul 07

- SUP 1: 110-31 50-day EMA

- SUP 2: 110-16 Low Jun 20

- SUP 3: 110-10+ Low Jun 16

- SUP 4: 110-03 76.4% of the May 22 - Jul 1 bull leg

A bull cycle in Treasury futures is intact and - for now - the latest pullback appears corrective. The contract remains above a key support at 110-31, the 50-day EMA, and the Jul 3 low. A clear break of this average would signal scope for a deeper correction and highlight a possible reversal. For bulls, a resumption of gains would open 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Initial resistance is at 111-28, the Jul 3 high.