CNH: Still Eyeing Sub 7.0900, Longer Term Policy Goals May Trump Growth Concerns

USD/CNH holds near 7.0940, down slightly for the session, we did have a brief dips under 7.0910 (fresh lows since late Oct), but there has been no follow through. The Oct data dump from earlier, which continued to highlight growth challenges, has done little to impact FX sentiment. Note we also heard from the PBoC's Tao, around increasing the use of the yuan internationally and aiming to make it a stable new option for the world (via BBG). This hints at China's on-going goals around CNY internationalization, which suggests it may be comfortable with a stronger exchange rate than would otherwise be the case (relative to domestic growth trends). In the near term this also continues to reflect the stronger CNY fixing bias relative to market expectations. Such a backdrop may leave USD/CNH risks still skewed to the downside (7.0851 was the mid Sep low), along higher CNY CFETS basket levels (i.e. CNH outperformance on some crosses).

- On balance today's data outcomes continued to highlight a challenging growth backdrop. Property headwinds persist from a price and activity standpoint. IP slowed (although this may have reflected pay back for the Sep bounce), while fixed asset investment surprised notably on the downside. Infrastructure investment fell 0.1% while manufacturing investment grew 2.7%, compared with the previous 1.1% and 4.0% growth.

- As we noted earlier in the week though, market expectations around fresh easing in the near term has generally been push out into 2026 (post recent firmer inflation data). China Stats also expressed confidence in achieving this year's growth target (post today's data outcomes). It noted though more work needs to be done on prices, via our policy team - "authorities plan to promote a moderate price recovery through industrial capacity management, improvements to the market’s competitive environment, and a better balance of supply and demand, Fu added."

- FX sentiment may shift if the authorities become more concern around the growth outlook. The first sign may be a neutral USD/CNY fixing bias. Exports have been a bright spot for growth this year, although Oct momentum faltered.

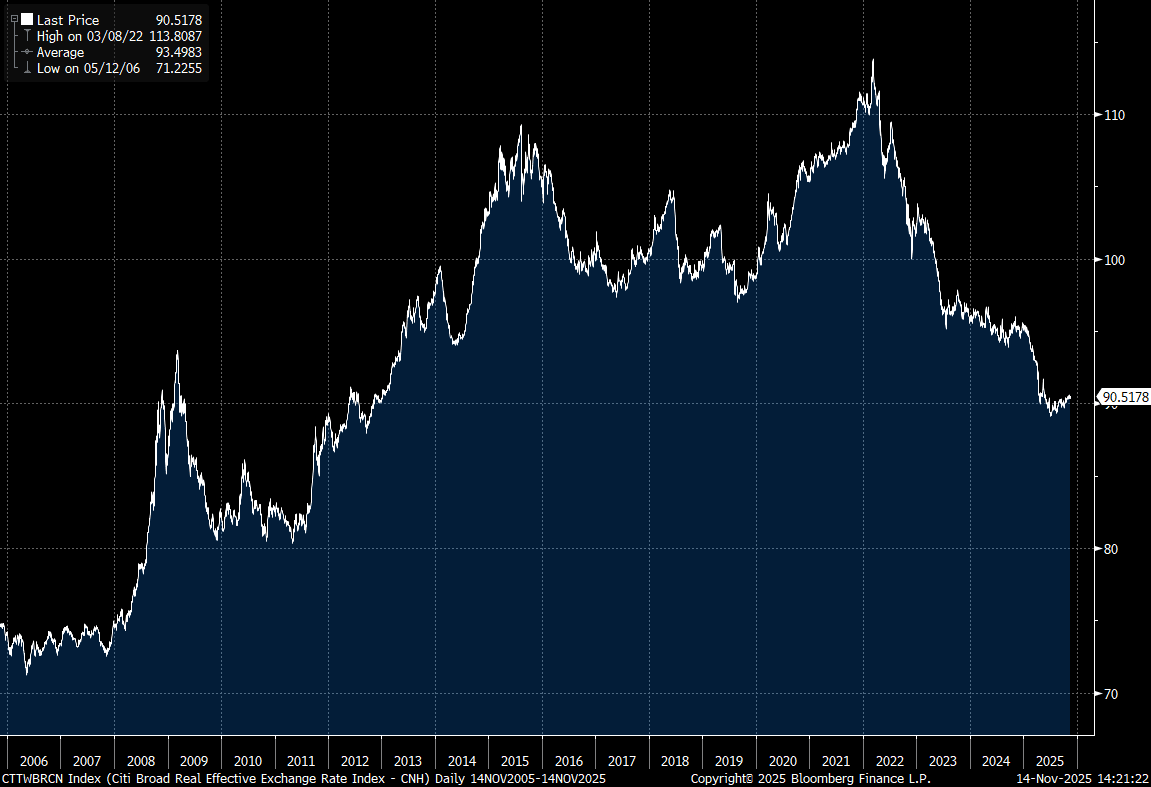

- The CNY CEFTS basket tracker is higher (last near 97.83) but still well off earlier 2025 highs around 102 (close to -4%). Moreover, in real terms the CNY TWI is only modestly above recent lows, see the Citi index below.

Fig 1: CNY REER - Citibank

Source: Citibank/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: 10-Yr Close to Trend Lows - Looks for Possible Break Overnight

TYZ5 traded up during the trading day in Asia reaching a high of 113-15+ from the open of 113-11 unable to provide meaningful follow on from the overnight rally in the US.

- The US 2-Yr is at 3.468%, down -1.5bps today.

- The US 5-Yr is at 3.592% having closed prior to Columbus day at 3.626% and down -1.5bps today.

- The US 10-Yr is down -2.3bps to 4.011% having failed to test 4.00% prior. It had looked likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out and will be watched closely overnight to see if it can break below and hold sub 4.00%.

- The US 30-Yr is down -2.3bps at 4.611%

- The Fed Chairman Powell's comments continued to echo through markets today with him indicating that the outlook for inflation and employment appears to have changed little since September, keeping intact expectations for two more rate cuts this year.

- Key data in the calendar for later is Empire Manufacturing which is forecast to decline -1.8 following -8.7 in September and Real Average Hourly Earnings.

OIL: Supply/Demand Outlook Pressures Crude But Holding Above Support Levels

Oil fell around 1.5% on Tuesday on fears current US-China trade tensions could reduce energy demand as the IEA increased its expectations of 2026 excess supply in the market. Lower-than-expected September China inflation also added to demand concerns. Crude was pressured by these developments today trading within a narrow range. Fed easing expectations and associated softer US dollar (BBDXY -0.2%) following Chair Powell’s comments have likely provided a floor in the APAC session.

- WTI is down 0.3% to $58.53/bbl off the intraday low of $58.37, just above support at $58.22. Brent is 0.5% lower at $62.10/bbl after falling to $62.02 holding above initial support at $62.00, 10 October low.

- US industry stock data are released later on Wednesday and the EIA data on Thursday, delayed a day due to the Monday holiday, and will be monitored given the focus on supply/demand trends. When supply exceeds demand it will appear in higher inventories.

- IEA revised up its 2026 market surplus forecast with excess supply expected to be 4mbd as it reduced demand projections moderately but increased non-OPEC supply by 200kbd for 2026. At 700kbd, consumption is below historical averages. The forecasts suggest downside risks for oil prices.

- Later the Fed’s Miran, Waller and Schmid speak and the Beige book is released. The ECB’s de Guindos, Buch and Donnery, and BoE’s Breeden and Ramsden also appear. US October Empire manufacturing and August euro area IP print.

AUSSIE BONDS: 10y Futures Near Key Resistance, AU 3/10s Curve Flattest Since Apr

Aussie bond futures are mixed, with the 10yr (XM) biased higher, aided by US Tsy futures moves (the US Tsy yield is threatening a downside test of 4.00%). We were last 96.77, +2bps, with earlier highs at 95.78, which is key short term resistance (multiple Sep highs). 3yr futures (YM) are down slightly, last 96.52.

- ACGB yields are mixed, slightly firmer at the front end, 3yr at 3.46%, while the 10yr is off close to 2bps last 4.21%. This leaves the 3/10s slightly flatter at +75bps. The AU-US 10yr spread has been relatively steady last +21bps.

- The RBA's Hunter said today that the RBA is looking to keep inflation close to the current rate which is around 2.6/2.7% for the trimmed mean. Her commentary on recent economic developments was consistent with the 30 September meeting minutes. There was nothing to suggest thinking for the 4 November decision. The Board remains flexible and highly data dependent.

- Market pricing for the Nov RBA meeting remains quite steady, last around 3.49%, against an effective policy rate of 3.60%.

- The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months.

- Note tomorrow we get Sep jobs data for Australia. The market expects a +20k rise, versus -5.4k prior. The unemployment rate is forecast to tick up to 4.3% from 4.2%.