CNH: Steady CNH Start, Focus On Today's USD/CNY Fixing

USD/CNH has had a relatively steady start to Thursday trade. We were last near 7.3020, only down a touch from end Wednesday levels in US trade. This is underperforming a slightly softer USD trend against the majors with both the BBDXY and DXY indices ticking lower.

- There will be focus on today's fixing given the tendency for higher settings in recent weeks. The fix has risen on 9 out of 11 days over this period.

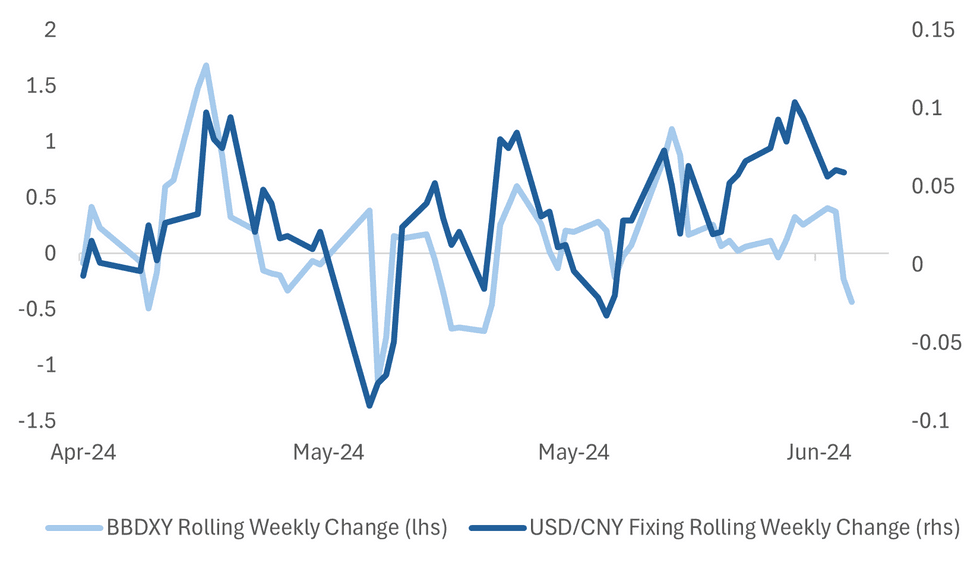

- We have had firmer USD bouts during this period, but the chart below plots illustrates that the USD has moved off highs in recent session, as the rolling weekly rate of change turns negative.

- The other line on the chart is the weekly rate of change in the USD/CNY fixing. Notwithstanding the different betas between the two series, we might have expected a lower USD/CNY rate of change over the past week given the USD softness.

- For today's fix the model estimates will likely be expecting a lower estimate relative to yesterday, given broader USD losses, although the official 4:30pm close was higher at 7.2734 yesterday.

- An unchanged or higher USD/CNY fixing today will reinforce bearish yuan expectations.

Fig 1: Rolling 1 Week Change In BBDXY USD Index & USD/CNY Fixing

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Hold Overnight Gains Ahead Of 10Y Supply

In Tokyo morning trade, JGB futures hold overnight gains, +25 compared to settlement levels, sparked by weaker-than-expected US ISM data.

- Japan’s monetary base rose 0.9% in May from a year ago versus expectations of +2.2%.

- Cash JGBs are richer beyond the 1-year, with the futures linked 7-year outperforming (2.8bps richer). The benchmark 10-year yield is 2.3bps lower at 1.046% versus the cycle high of 1.101% set last week.

- Today’s 10-year auction held last month went poorly, with the tail lengthening and the cover ratio falling to 3.151x from 3.799x at April’s auction.

- The current 10-year auction is taking place with an outright yield of approximately 20bps higher than the early May offering.

- Traders will monitor today’s 10-year supply to gauge demand for Japanese bonds with BoJ’s monetary policy decision looming next week. The BoJ will likely keep the JGB purchase reduction plan flexible, dependent on market conditions, and avoid providing an exact number, said analysts at MUFG (per BBG).

- Swaps are richer, with rates ~1bp lower. Swap spreads are mostly wider.

FOREX: USD Softer, But Yen Lags, Q1 GDP Partials Coming Up In Australia

The USD is marginally weaker in the first part of Tuesday trade. The BBDXY tracks under 1250, not too far from lows recorded in the first part of Monday trade.

- Cross asset wise US equity futures are higher, but only by around 0.1-0.15% at this stage. Regional equity sentiment is mostly weaker for Asia Pac markets that are open. US yields are a touch higher, with gains around 1bps across the benchmarks, following Monday's sharp dip (post weaker ISM data).

- The yen is underperforming at the margins, last near 156.15/20, slightly above end NY levels from Monday.

- AUD and NZD have ticked higher, but gains are under 0.1%. AUD/USD is near 0.6700, but hasn't been able to breach this figure level yet. NZD/USD is close to 0.6200.

- Coming up we have partials for Q1 GDP in Australia. Net exports (forecast is -0.7, versus 0.6 prior), along with the current account, inventories (0.7% forecast, prior -1.7%) and company profits (-0.9% forecast, versus 7.4% prior), are all due.

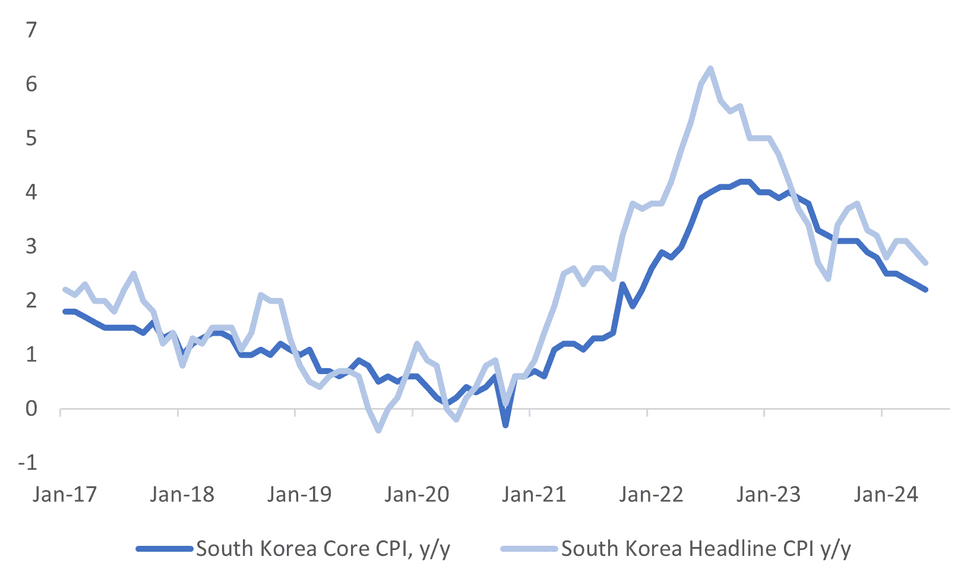

SOUTH KOREA: Y/Y Inflation Momentum Slows Further, Core Pace Back To Late 2021 Levels

South Korea May CPI was a touch below market expectations. The m/m outcome was 0.1%, against a 0.2% forecast and flat outcome in April. headline was 2.7% y/y, versus 2.8% forecast and 2.9% prior. Core (ex food and energy) was 2.2%, in line with expectations but slightly lower than April's 2.3% print.

- Headline inflation is back near mid 2023 lows, while core is back to late 2021 lows, see the chart below.

- Core CPI y/y is now not too far from the BoK's target of 2%. The central bank noted in its most recent policy meeting there were high uncertainty regarding the inflation outlook (this year's core forecast is at 2.2%, headline 2.6%).

- In terms of the detail, food -0.7%m/m, which fell for the second straight month, was a drag, as were furnishings (-0.2%). 4 out of 12 sub indices recorded a firmer m/m pace compared to April. Clothing and transport both rose 0.6% m/m.

- The data, at the margin, adds to the BoK easing case in H2. Sticky household inflation expectations (still above 3%) aren't translating into an uptick in core pressures at this stage.

Fig 1: South Korea CPI Saw Further Deceleration In May

Source: MNI - Market News/Bloomberg