US CREDIT SUPPLY: Standard Chartered $ B'mark 4NC3 ; 11NC10 - LAUNCH

• $1B 4NC3 Fixed to float +77/ FV +78

• $500MM 4NC3 FRN SOFR+92

• $1B 11NC10 IPT +107 / FV +105

• Format: 144A/Reg S, senior unsecured

• Exp. Ratings: A3/BBB+/A

• Joint Lead Managers: BARC, GS, JPM, Scotia Capital, STANLN (B&D) and UBS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

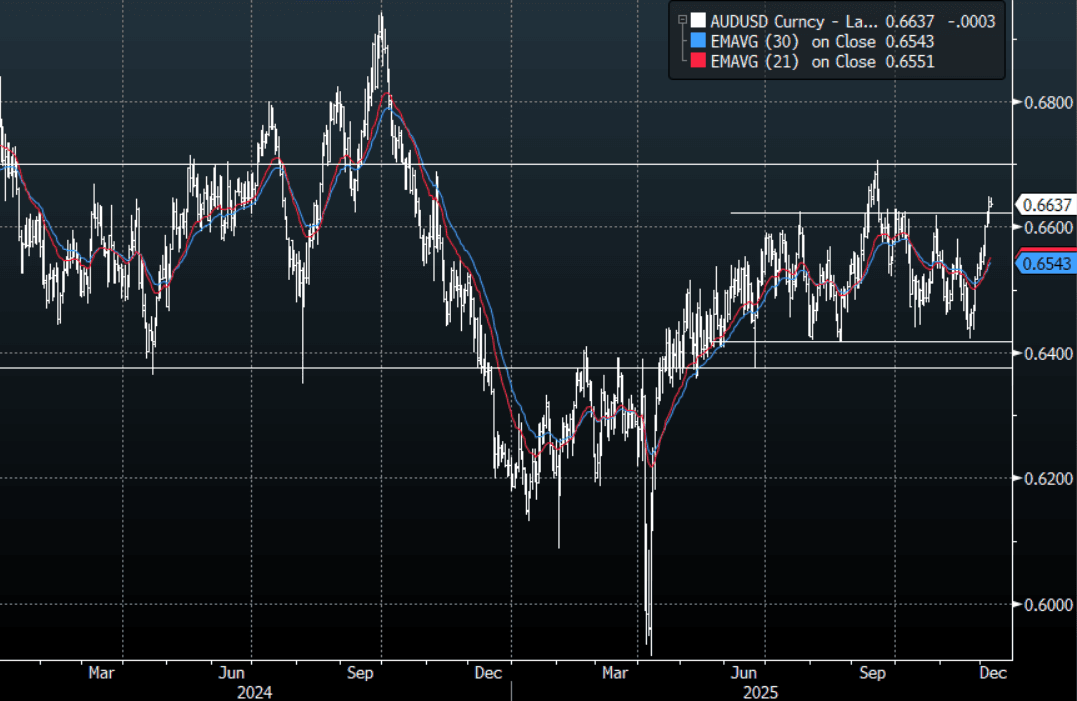

AUD: AUD/USD - Breaks Above 0.6630, But Fails To Extend Higher

The AUD/USD had a range Friday night of 0.6622-0.6649, Asia is trading around 0.6635. The AUD pushed through the 0.6630 area, it has consolidated above there but without really building on this break. The AUD price action remains very constructive and indicative of a market with solid buying interest. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, look to see if the AUD can hold above this 0.6620/30 area. It has come a long way so if this does not hold we could see a pullback, first support below that is toward 0.6570/90 where we should see demand reappear. Ultimately the AUD is looking to rebuild momentum to have another look back toward the 0.6700 area at some point. RBA tomorrow and the FOMC later this week should dictate price action coming up.

- MNI - The RBA decision is announced tomorrow and rates are highly likely to be left at 3.6%. With the outcome widely expected, the tone of the statement and press conference will be scrutinised and given the strength of the data since the last meeting, there is a risk that the bank will sound more hawkish. The market has a 25bp hike priced in by August. October underlying CPI inflation printed at 3.3% and while Q3 GDP was below consensus, domestic demand was very strong rising 1.2% q/q. Governor Bullock said that while the output gap size is uncertain, it probably has closed, which increases risks to inflation from stronger demand. Thus, rates are likely on hold for some time.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD814m), 0.6500(AUD342m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 35 Points

- Data/Event: Foreign Reserves.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

USDCAD TECHS: Bull Channel Breakout

- RES 4: 1.4140 High Nov 5 and a key resistance

- RES 3: 1.4131 High Nov 21

- RES 2: 1.4051 High Nov 28

- RES 1: 1.3939/4016 Low Nov 28 / 20-day EMA

- PRICE: 1.3865 @ 16:35 GMT Dec 5

- SUP 1: 1.3853 Intraday low

- SUP 2: 1.3840 50.0% retracement of the Jun 16 - Nov 6 bull cycle

- SUP 3: 1.3812 Low Sep 23

- SUP 4: 1.3779 Low Sep 22

A bear theme in USDCAD remains intact and Friday’s strong sell-off reinforces a bear theme. The pair has breached an important support at 1.3942, the base of a bull channel drawn from the Jul 23 low. The break highlights a stronger bear cycle and signals scope for an extension towards 1.3840 next, a Fibonacci retracement point. Initial firm resistance to watch is 1.4016, 20-day EMA.

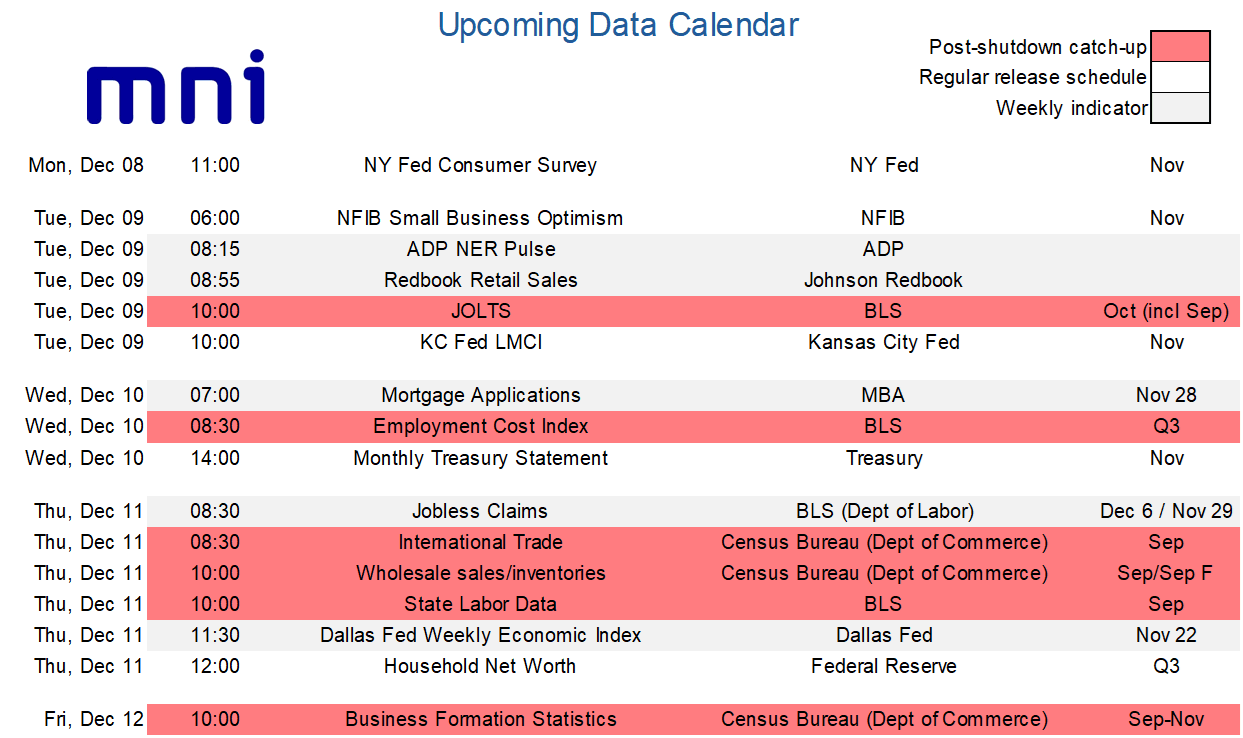

LOOK AHEAD: US Week Ahead: FOMC Decision Dominates, Post Shutdown Data Catch-Up

- Next week’s US calendar is dominated by the FOMC decision on Wednesday, with a third consecutive 25bp cut almost fully priced.

- Expect it to be a contentious meeting however, with many arguing for a pause not least whilst they’re still relatively in the dark on key official data releases following the government shutdown.

- Fed Chair Powell opted for a surprisingly hawkish tone at the late October press conference, highlighting a deeply divided committee on prospects for another cut in December.

- The “fog” had appeared to win out until NY Fed’s Williams, a senior permanent voter, gave unusually explicit guidance on still seeing room “for a further adjustment in the near term”. With no pushback from FOMC members or media briefings, it appears this message has approval from the core of the FOMC which should be enough to see a rate cut this month. The likely catalyst was the further increase in the unemployment rate to 4.44% back in September, although subsequent tracking suggests stabilization and jobless claims data don’t show any signs of deterioration.

- We’ll be looking for the number of hawkish dissents (we’d be surprised if anyone joins Miran dissenting for a 50bp cut) and expect a greater number to object to a cut in the 2025 dot plot, whilst the distribution of dots for 2026 should be in greater focus.

- As for the economic projections, we expect upward revisions to GDP growth but downward revisions to near-term core PCE inflation with tariff passthrough proving less severe than previously feared.

Aside from the Fed, we also receive two months worth of JOLTS data along with other delayed releases as the shutdown data backlog is slowly caught up.