SWAPS: Spreads Narrow After Bowman Signals SLR Reform Part Of Holistic Process

Jun-06 15:42

Newly-installed Fed Vice Chair for Supervision Bowman's speech on "Taking a Fresh Look at Supervision and Regulation" is here.

- The most noteworthy comment is her reiteration of the likelihood of supplementary leverage ratio (SLR) reform: "The original calibration of the eSLR was based on forecasts of the level of reserves and other so-called "safe assets" in the system that are now far out of line with current levels. I expect that in the near future, the agencies will publish a proposal to help address this concern and ensure that the eSLR resumes functioning as a backstop capital requirement." As a result of the SLR requirement, "banks are less inclined to engage in low-risk activities like Treasury market intermediation and revise their business activities in a way that is neither justified nor responsive to their customer needs. These distortions can also create broader financial system impacts like increased stress on Treasury market functioning,"

- Bowman also said the Fed will host a conference in July addressing several aspects of large bank regulation including SLR, though in a nod to broader reforms, she says there will also be potential changes discussed at the event including GSIB surcharges, Basel III capital requirements, and stress testing.

- In Q&A, she elaborated on the need for a holistic approach to regulation: "So if we change one, we need to ensure that the others can reflect the appropriateness of what what the aggregate level of capital in the system should be. So the idea is that we're already looking at our stress tests. We're looking at the SLR. We know that Basel III needs to be finalized and we have the surcharge that is out for proposal from from the previous years. So each one of these components, one is very complex, but two, they also have overlapping requirements that interact with each other. So it's important, as we're concerned, to bring all of the pieces of the large bank capital framework that we understand how they interact together and that we're talking about each one of them and identifying those ways and that when we're approaching changing 1 or 2 of those or or three of them that we understand whether or not we need to make changes to all of them."

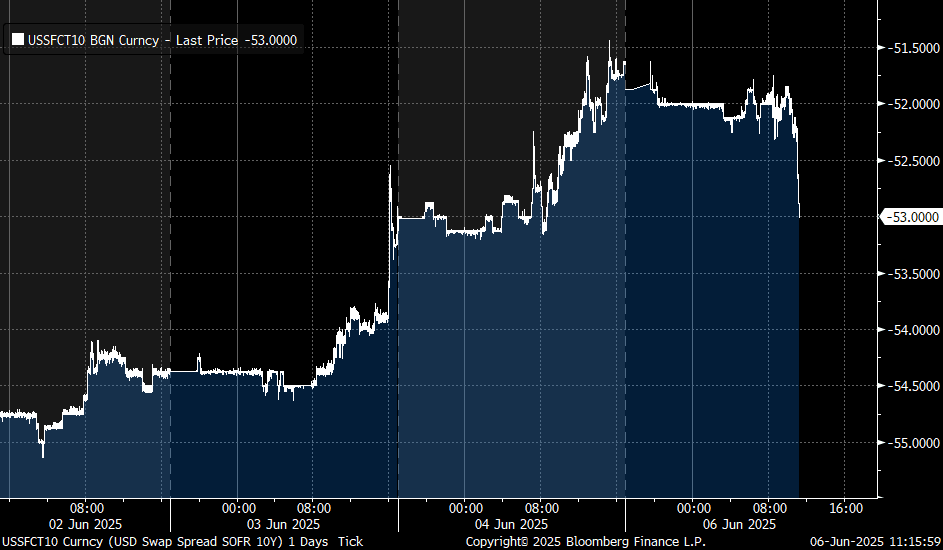

- It's unclear whether there was a little disappointment at a perceived lack of further detail or added urgency from Bowman on SLR reform. Swap spreads ticked slightly higher in the wake of the Bowman speech release but have pulled back since the Q&A (in swaps' favor against Tsys) to a 2-session low for SOFR/Tsy 10Y at -52.6bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Jun'25 2Y/5YSteepener

May-07 15:41

Latest cross posted at 1133:22ET, DV01 $255,000:

- +7,000 TUM5 103-22.38, buy through 103-22.25 post time offer vs.

- -6,000 FVM5 108-16.25, sell through 108-16.5 post time bid

FED: US TSY 17W BILL AUCTION: HIGH 4.200%(ALLOT 51.46%)

May-07 15:32

- US TSY 17W BILL AUCTION: HIGH 4.200%(ALLOT 51.46%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 31.65% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 3.50% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 64.86% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.02

US TSY OPTIONS: Large Jun'25 5Y Vol Scale Seller

May-07 15:27

- Over -13,000 FVM5 107.5/109 strangles, last level at 19 vs. 108-16.5/0.18%, implied vol 4.45%