KRW: Spot USD/KRW Holding Close To 1390, Still Lagging Equities

Spot USD/KRW finished up at 1389.2 in Thursday trade, little changed versus end Wednesday levels. The won continues to lag softer USD trends, amid rising Fed easing expectations, while tech equities also continue to rally. At this stage USD/KRW is up modestly versus end levels from last week.

- Spot USD/KRW did finish off intra session highs near 1394 from Thursday trade. Still, we haven't been able to get under the 1384 level so far this week, while late August lows rest near 1380.

- Whilst softer USD trends are helping to keep USD/KRW capped sub 1400, the wedge with global tech equity trends and Fed easing expectations remains wide. To be sure US-SK 1y1y differentials are above recent lows, but is still implying USD/KRW should close to 1370, not 1390 (all else equal).

- In the equity space, the SOX rose 0.63% on Thursday, up for the sixth straight session, while the MSCI IT was up a modest 0.23%. To recap, the Kospi finished 0.90% higher yesterday, while offshore investors added $168.3mn to local stocks.

- Via BBG: "South Korea must accept the trade deal with the Trump administration that includes investment in the US, or it will pay tariffs, Commerce Secretary Howard Lutnick tells CNBC."

- Uncertainty around the US-South Korea deal may be weighing on won sentiment, or at least curbing USD/KRW downside amid some of the positives outlined above.

- The data calendar is quiet today. The finance ministry will release its monthly economic assessment report.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

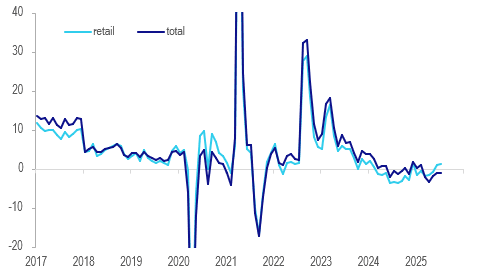

NEW ZEALAND: Gradual Recovery In Retail Card Spending

July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- While total retail spending rose slightly on the month, the core was close to flat. Statistics NZ noted that consumables transactions rose 0.5% m/m, while vehicles ex fuel jumped 5.2%. Apparel fell 1.9% and durables -0.8%.

- Non-retail ex services expenditure increased 1.6% m/m but services only 0.3%.

NZ card spending y/y%

Source: MNI - Market News/LSEG

JGBS: Futures Weaker Overnight After US CPI Data, PPI & 5Y Supply Due

In post-Tokyo trade, JGB futures closed weaker, -18 compared to settlement levels, after US tsys finished with a twist steepening on Tuesday.

- The focus was on the July CPI for insight on the FOMC's policy path. That the data failed to surprise on the hotter side of expectations opened the door a little wider for a September rate cut.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- That provided a strong underpinning for Wall Street which climbed to record highs.

- (Bloomberg) -- "Japan's current benchmark 10-year government bond wasn't traded at all on Tuesday, the first such instance in more than two years, according to data from an institutional brokerage."

- Today, the local calendar will see PPI and Machine Orders data alongside 5-year supply.

AUSSIE BONDS: Twist Steepener With US Tsys, Q2 Wages Due

ACGBs (YM +1.5 & XM -1.0) are slightly mixed after US tsys finished with a twist steepening on Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- Cash ACGBs are 2bps richer to 1bp cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 37% probability, with a cumulative 52bps of easing priced by year-end.

- Today, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond today and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.