EMISSIONS: Speculators Raise EUA Bullish Bets to Highest Since Late March

Aug-13 07:37

Investment funds increased net long positionings in EU ETS futures on the ICE exchange for the third consecutive week to the highest since the week ending 28 March, according to the latest COT data as of 8 August.

- Investment Funds net long positionings increased by 8,1009 to +28,856

- Investment Firm net short positionings increased by 9,405 -426,583

- Commercial Undertaking net long positionings edged up by 824 to +313,362

- December 2025 EUAs increased by around 2.7% in the week to 8 August, supported by gains in EU equities amid strong earnings and optimism over a potential ceasefire in Ukraine.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA JAN-JUNE NEW LOANS CNY12.92 TRLN VS MEDIAN CNY12.72 TRLN

Jul-14 07:35

- CHINA JAN-JUNE NEW LOANS CNY12.92 TRLN VS MEDIAN CNY12.72 TRLN

- CHINA END-JUNE M2 +8.3% Y/Y VS MEDIAN +8.2%; END-MAY +7.9% Y/Y

- CHINA END-JUNE M1 +4.6% Y/Y VS +2.3% Y/Y END-MAY

- CHINA END-JUNE M0 +12.0% Y/Y VS +12.1% Y/Y END-MAY

- CHINA JAN-JUNE TSF CNY22.83 TRLN VS MEDIAN CNY22.43 TRLN

GERMAN AUCTION PREVIEW: Schatz Coupon Announcement

Jul-14 07:35

Germany will look to sell E5bln of the new 1.90% Sep-27 Schatz (ISIN: DE000BU22106) at its auction tomorrow (July 15)

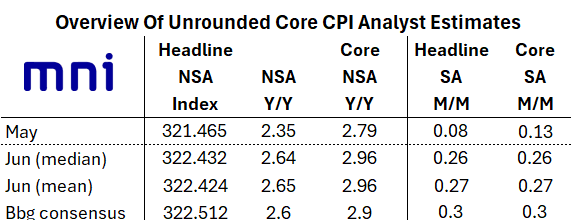

US INFLATION: [RPT] CPI Seen Picking Up In June, Core Goods Eyed

Jul-14 07:30

Note: Our full CPI preview will be released later today.

June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation. Both core and headline CPI are seen rising to the mid 0.20s% M/M, from May's readings of 0.13% for core and 0.08% for headline.

- Such outturns would mean the strongest M/M headline CPI since January, with core continuing to range between 0.0-0.3% for a 5th consecutive month. They would also bring the Y/Y core reading to 2.9% or 3.0%, with headline at 2.6% or 2.7% (both would be 4-month highs).

- The first area of focus will be on core goods prices, with the impact of import tariffs expected to become more acute as the summer progresses: core goods are seen up from May's flat M/M reading to closer to 0.2%, with tariff-sensitive categories such as apparel and recreational goods seeing a pickup, offset by a drag from used vehicles.

- Core services are seen picking up modestly from 0.2% M/M in May to closer to 0.3%, with May's relatively tame housing inflation steady-to-higher. "Supercore" (core services ex-housing) is expected to rise from May's surprisingly low sub-0.1% M/M print to closer to 0.3%, as airfares and medical care services prices regain traction.

- It's unlikely that a downside surprise would persuade the Federal Reserve to seriously consider cutting rates in July, given the expected pickup in tariff-related prices in coming months, but it would certainly help lay the groundwork for a resumption of easing in September.