SWEDEN: Solid Rise In Nov GDP, Riksbank Not Concerned About Inflation Risks

Jan-09 08:39

Swedish GDP rose 0.9% M/M in November, according to monthly activity data. That was much stronger th...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Yields Edge Higher Alongside Peers

Dec-10 08:34

Gilts weaken alongside global peers, although futures stick comfortably within yesterday’s range.

- A reminder that we have suggested that post-Budget movement in OI in futures doesn’t point to the establishment of a meaningful number of high conviction longs since that event, despite the market apparently deeming Chancellor Reeves’ fiscal consolidation to be credible.

- Risks surrounding the backloaded nature of the fiscal consolidation that was outlined in the Budget may be key here, albeit with the cash curve flattening as the DMO continues to skew issuance away from the long end.

- Futures -14 at 90.96. Initial support and resistance located at 90.62 & 91.29, respectively.

- Yields 1.5-2bp higher across the curve.

- SONIA futures flat to -2.0, marginal hawkish repricing as gilts soften.

- Global cues have driven the hawkish repricing seen over the last week or so.

- The DMO will sell GBP4.5bln of the 4.75% Oct-35 gilt this morning.

ECB: What Would Macron's Suggestions Mean For The ECB?

Dec-10 08:34

- French President Macron has called for a change in the ECB's monetary policy objectives (Bloomberg article here): “it seems to me that European monetary policy can be significantly adjusted today” adding that “Reasserting the value of the European internal market means we can’t let inflation be our sole objective, but also growth and employment", he said. This is not the first time Macron has called for changes to ECB thinking. Last year, he called for expanded objectives "integrated with that of growth and decarbonisation".

- What would that mean for interest rates? The ECB currently has a single mandate, "maintaining price stability". Macron's proposals look to align the ECB's mandate closer to the Federal Reserve's, which also optimizes for maximum sustainable employment.

- Some economic theories highlight the “divine coincidence”: Stabilising inflation often automatically stabilises the output gap, meaning there is little to no trade-off between inflation and output stabilization. However, dual mandates can also come into tension, particularly in the case of a stagflationary environment. Macron's suggestion may argue for lower rates as the focus is not unanimously on controlling inflation any more.

- What would be the policy process for a change to the ECB's mandate? This would require an ECB treaty change - which ultimately needs to be ratified by all 27 EU member states. This may require parliamentary approval, referendums or constitutional court judgements, meaning a comprehensive policy process. Other EU leaders are yet to publicly support Macron's views.

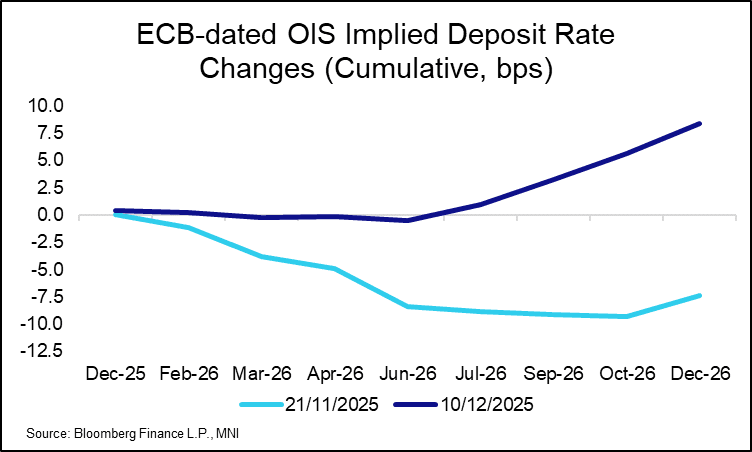

STIR: Villeroy and Simkus Try To Push Back On Hike Expectations

Dec-10 08:25

- This morning’s ECB speakers have offered some pushback against growing expectations for a hike as soon as December 2026, but their comments haven’t impacted market pricing for now. Villeroy noted that “as seen today, there is really no reason to envisage a rate increase in the near future, contrary to certain rumors and speculation that may have been heard”. Meanwhile Simkus said that there is “no evidence” of inflation overshooting the target. Villeroy and Simkus have moderated their previously dovish stances in recent weeks. As such, their views probably align broadly with the median Governing Council member.

- ECB-dated OIS price ~8.5bps of hikes through the end of next year, while the ESTR 1y1y forward rate is currently 2.15%, 22bps above the overnight rate.

- Recent hawkish repricing in EUR rates was helped by Executive Board member Schnabel saying she was “comfortable” with expectations for the next ECB move to be a hike. We stress that these comments weren't surprising given Schnabel's usual stance, and note that in the same interview she said that “Interest rates are in a good place, and in the absence of larger shocks, I expect them to stay in this place for some time.”

- At next week’s ECB press conference, President Lagarde is unlikely to explicitly push back on market pricing. In September, her response to a question on markets was: “I don’t have to be happy or unhappy. I think that markets do what they have to do, and we do, as the central bank, what we have to do. Now, of course, as I said, we monitor markets always and, as you know, also as part of our projections, we account for market positions at a certain point in time”.

- We instead think that Lagarde will stress that ECB policy remains in a “good place”, implicitly suggesting the 2% level is appropriate for the foreseeable future (but of course conditional on incoming data).