NORWAY: Solid Q3 RNS; Next Week Decision Hinges On Assessment of Inflation

The Q3 Regional Network Survey was solid overall, perhaps a touch hawkish on the margin. We think next week’s Norges Bank decision will hinge decisively on how the Committee views the August inflation report, which was stronger-than-expected after considering a policy change in Child daycare prices. There hasn’t been a material reaction in NOK FX/rates to the report, suggesting markets are happy with current pricing that still leans in favour of a 25bp cut next week.

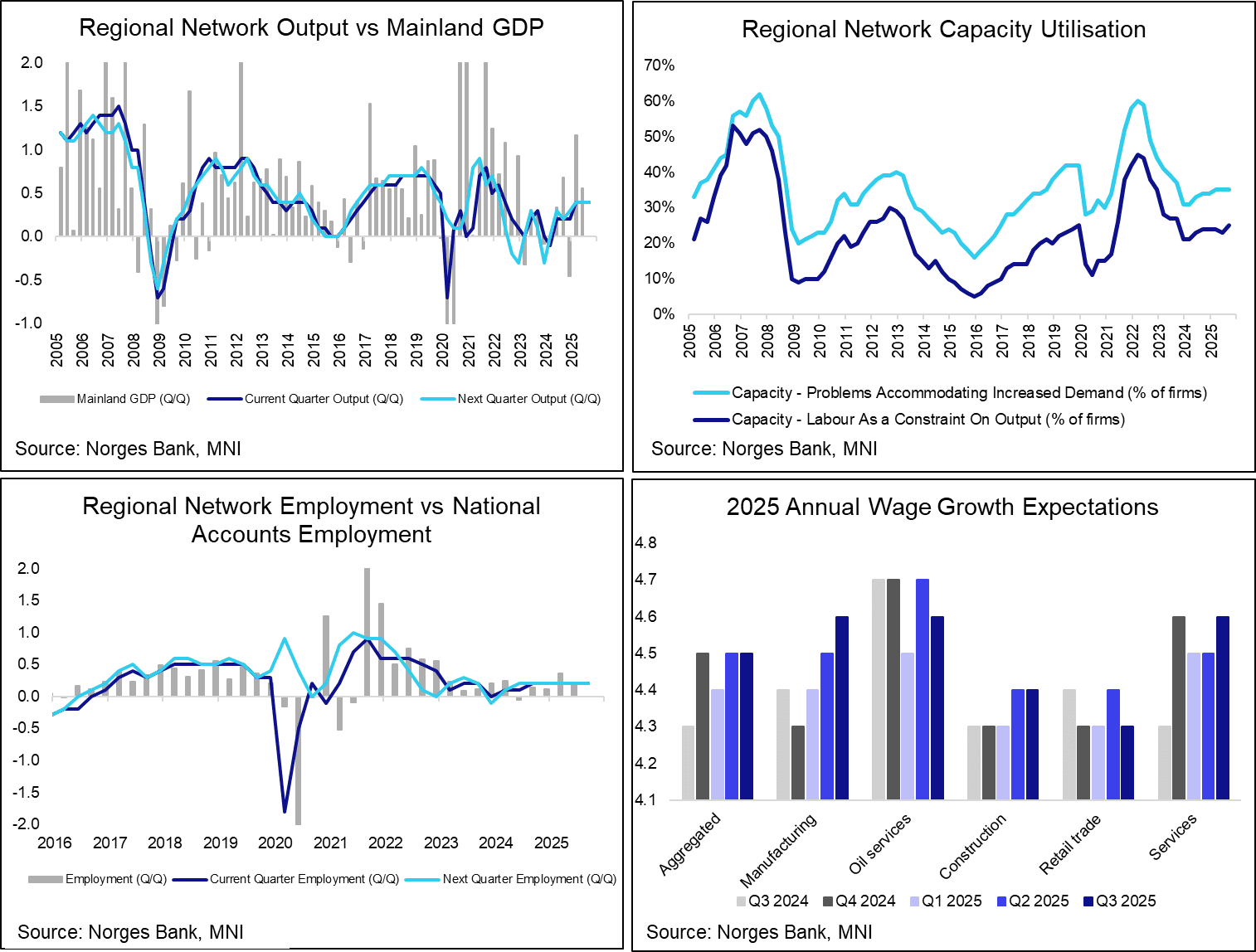

Inflation/slack: Overall, fairly steady developments relative to Q2.

- Wage growth expectations were steady at 4.5% Y/Y in 2025 and 4.0% in 2026. Broadly in line with Norges Bank June MPR (4.5% in 2025 and 4.1% in 2026).

- Capacity Utilisation: The share of contacts that will have problems accommodating a rise in demand was steady at 35%. However, the share of those citing shortage of labour as a constraint on output ticked up to 25% (vs 23% in Q2). The latter is somewhat surprising given the sharp rise in (caveated) LFS implied participation rates and fall in vacancy rates in recent months.

Output/Activity: Steady, positive signals. We don’t think the rise in investment intentions should be considered too hawkish, as these estimates can be volatile.

- Q3 and Q4 output seen at 0.4% Q/Q. Norges Bank projected Q3 mainland GDP at 0.4% Q/Q in the June MPR, but may revise up its outlook in the September MPR following solid outturns in Q1 and Q2.

- Largest increases in expectations relative to the prior survey came from construction and oil services. In the latter category, better expectations amongst domestic oil services firms were offset a little by worse expectations amongst export-oriented firms.

- Q3 and Q4 employment seen at 0.2% Q/Q, little changed from the previous survey.

- Q3 investment expectations seen at 1.1% Y/Y in 2025 and 0.1% in 2026, solid upward revisions relative to the June survey. This year’s rise was driven by manufacturing (5.0% vs 0.5% prior) and oil services (0.5% vs -5.0% prior), while 2026 was driven by oil services (0.0% vs -1.5% prior) and other services (2.5% vs 0.5% prior)

- Profitability expectations were revised up to 5.9% Y/Y (vs 4.2% prior)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Call Spread vs Put Spread

SFIM6 96.90/97.10cs vs 96.00/95.85ps, bought the cs for 1.25 in 5k.

FRANCE DATA: BdF Expects Q2 GDP To Be Confirmed At 0.3%

Banque d France's expects Q2 GDP growth to be confirmed at 0.3% Q/Q following the releaase of the August monhtly business survey. Based on a survey of 8,500 businesses between July 22 - August 5, the survey notes that:

- "Activity continued to grow significantly in July in industry and construction, and more moderately in market services. In August, according to business expectations (which should be interpreted with greater caution this month due to the holidays), activity would remain on the rise in industry and construction and would change little in services. Order books are considered slightly less empty in industry excluding aeronautics, as well as in construction, while remaining relatively low".

- "Our monthly uncertainty indicator, constructed from a textual analysis of comments from the companies surveyed, continues to decline in all three sectors, and more significantly in construction. It remains significantly higher in industry compared to services and construction, which reflects the greater exposure of this sector to international trade, particularly to the United States' tariff policy".

- "Based on information from the Banque de France's monthly business survey, supplemented by other available data (industrial production indices, INSEE surveys, and high-frequency data), we estimate that GDP will grow in the third quarter at a pace close to that observed in the previous quarter. Activity will be driven by the dynamism of value added in the manufacturing industry, as suggested by the monthly business survey. Value added will also increase in market and non-market services, but will decline in construction and energy".

EQUITIES: Estoxx Put Spread

SX5E (19th Sep) 4900/4550ps, bought for 11 in 7.5k.