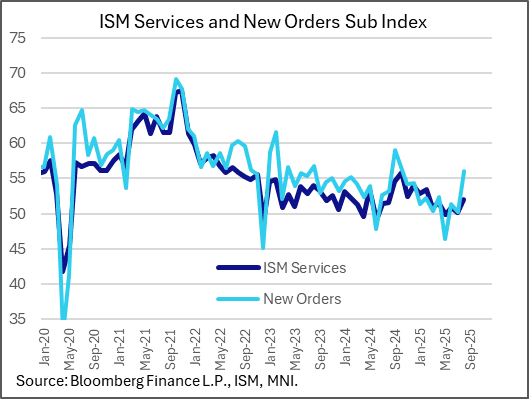

US DATA: Solid ISM Services Potentially Boosted By Tariff-Related Activity

August's ISM Services report was stronger than expected in most major categories, with the headline index rising to a 6-month high 52.0 from 50.1 prior (and vs 51.0 Bloomberg consensus). This was a solid report but there was still ample evidence of tariff-related effects on business activity: anecdotes suggested front-running may be exaggerating a sharp improvement in new orders and a rise in inventories, and while price pressures moderated slightly, they remain very elevated.

- New orders were a standout in the report at a 10-month high 56.0 (50.3 prior, 51.1 expected), despite a pullback in New Export Orders to a 5-month low 47.3 (47.9 prior). Some anecdotes suggested continued tariff front-running may have been a factor (“Getting merchandise into the U.S. ahead of effective dates of tariff increases"). Indeed, Imports rose 8.7 points to 54.6, highest since January 2024.

- One standout on the downside was that the Backlog of Orders subindex was below 50 for a 6th consecutive month, down 3.9 points at 40.4 for the lowest since May 2009 - there wasn't much explanation provided in the report but the ISM highlighted that this 16-year low was a negative factor.

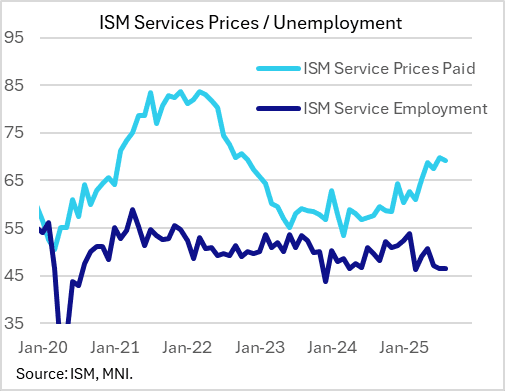

- Employment improved, but by slightly less than anticipated, to 46.5 from 46.4 (46.7 expected), and thus remaining in contractionary territory for a 3rd consecutive month and 5th month in 6. (One side note, the only "Commodity" listed as being in "short supply" in this report was "Labor — Construction").

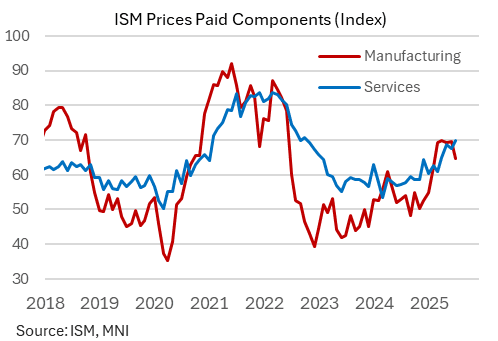

- Prices Paid fell a little more than expected from July's 33-month high 69.9, although at 69.2 remains elevated.

- Supplier Deliveries remained above 50, indicating slower supplier delivery performance, but the 0.7 point drop to 50.3 suggested that deliveries were slowing at a lesser rate. The anecdotes were of potential interest from a tariff-hit supply chain perspective albeit mixed (“It appears most manufacturers are finally back to pre-COVID-19 lead times” and “Shortage of a vendor’s inventoried goods has affected the on-time delivery of needed supplies.”)

- Additionally, Inventories rose 1.4 points to 53.2 (above 50 for 3 consecutive month), with respondents noting potential inventory build ahead of anticipated price increases (one anecdote reported “We have been making strategic buys of critical components to build a safety stock in response to extended lead times and anticipated price increases in the fourth quarter”).

- Even so, Inventory Sentiment was up 2.3 points to 55.5, indicating that firms increasingly see inventories as "too high”.

- Overall, 12 (of 16) industries reported growth in the month, one more than in July's report. The non-growth exceptions: " Accommodation & Food Services; Management of Companies & Support Services; Other Services; and Construction".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

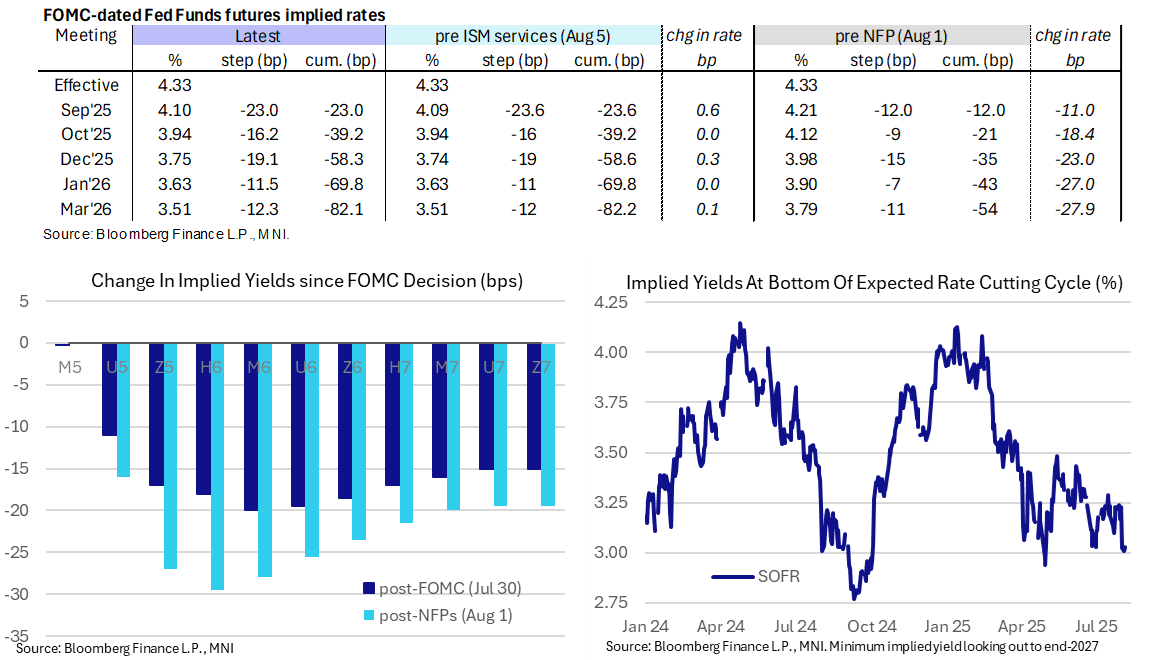

STIR: Fed Rates Look Through A Mixed ISM Services Report

- Fed Funds implied rates have seen almost no reaction to the ISM services report for July, rising at most 0.5bp for meetings out to 1Q26.

- The overall index underwhelmed in July at 50.1 (cons 51.5) after 50.8 in contrast to a strong rise in the S&P Global US services PMI, but prices paid surprisingly increased to 69.9 (cons 66.5) after 67.5 for a fresh high since late 2022.

- Cumulative cuts from 4.33% effective: 23bp Sep, 39bp Oct, 58.5bp Dec, 70bp Jan and 82bp Mar.

- Echoing the growth negative aspects of the report, the SOFR implied terminal yield of 3.03% (SFRH7) is 1bp lower post-ISM to limit the day’s increase to 2bp.

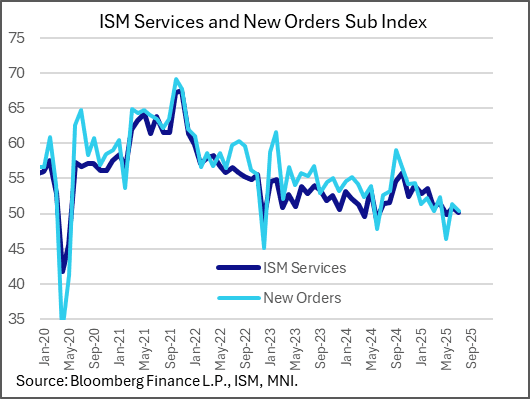

US DATA: ISM Services Points To Stagflationary Developments Amid Tariffs

July's ISM Services data were more "stagflationary" than anticipated, with a dip in activity amid a pickup in price pressures. The report overall suggests that firms' tariff-related concerns linger, with momentum failing to build on a brief improvement in June. Combined with the headline index, the subcomponents of the survey show a clear slowing in activity since late 2024.

- The headline Services PMI reading fell by 0.7 points to 50.1 (51.5 expected, 50.8 prior), merely a 2-month low but suggesting that an expected pickup in momentum and sentiment is not materializing. The ISM report writes that the index is consistent with 0.5% annualized real GDP growth. Business activity fell 1.6 points to 52.6.

- The main worrying point was new orders, which fell 1 point to 40.3 (no expectations). That was led by a 3.2 point drop in new export orders (47.9) - which apart from March 2025's tariff driven low (45.8) was the joint-weakest since March 2023. Imports fell 5.8 points from 51.7 - one firm's anecdote was “Imports have increased in price, to be less competitive than domestic vendors.”

- Employment, too, was a weak spot - down 0.8 points at 46.4, it's now declined in 2 consecutive months after a brief return above the 50.0 mark in May. It's now been below 50 in 4 of 5 months (i.e. contractionary). However, the anecdotes of the latest report make it difficult to know whether this squares with the broader "low hiring, low firing" theme in data elsewhere, with firms reporting supply-side restraints rather than weaker demand ("Comments from respondents include: “Lost a few service technicians; still difficult to recruit in this market” and “We have lost employees due to normal attrition and are having issues backfilling these positions with qualified candidates.”)

- Inventories fell by a second consecutive month, by 0.9 points to 52.7 (further evidence of pre-tariff buildup reversing; inventory sentiment pointed to inventories were "too high" at 53.2 albeit down from 57.1 prior and the lowest since Oct 2024), while supplier deliveries rose 0.7 points to 51.0 (slower supplier deliveries, which is a positive for the headline reading).

- Prices paid meanwhile ticked up 2.4 points to 69.9 (66.5 expected, 67.5 prior), a fresh 33-month high. While MNI had flagged potential upside risks to the prices reading, based on regional Fed surveys and the flash PMI report, this was even higher than we would have anticipated and defies a pullback in its manufacturing counterpart.

EUR: FX Exchange Traded Option

FX Exchange trade Option, looking for EUR upside, doesn't cover the next Sep ECB meeting (11th Sep):

- EURUSD (5th Sep) 1.1600c, bought for 0.0096 in 1.4k.