US OUTLOOK/OPINION: Solid Core PCE Estimates With PPI Portfolio Rebound Eyed

Jul-16 11:34

- Adding a few more names to yesterday’s round up of core PCE analyst estimates ahead of today’s PPI details, the average estimate still sits at 0.31% M/M in June after 0.18% M/M in May. This lifted from closer to 0.25% prior to CPI.

- Core PCE estimates for June: JPM 0.28, TDS 0.28%, Barclays 0.29%, GS 0.29%, Citi 0.32%, UBS 0.32%, BofA 0.34%, MS 0.35% and Nomura 0.35%.

- A reminder that there are many, mostly services-related, components that feed into core PCE from PPI, with medical care, airfares and in particular portfolio management & investment advice again receiving attention this month.

- Also expect continued growing focus on the broader core PPI categories for cost pressure implications.

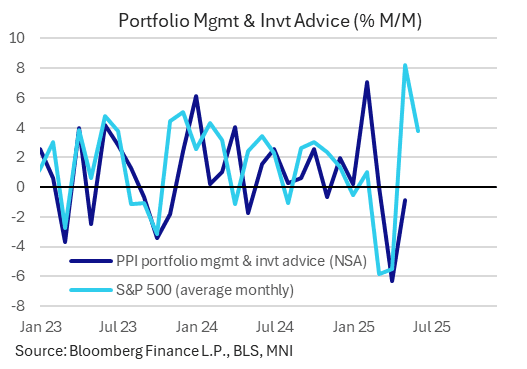

- Portfolio management & investment advice: It fell -0.8% M/M in May following swings in recent months of -6.3% in Apr, a flat Mar and +7.1% in Feb on equity market volatility.

- Lags in the series suggest that strong increases in equity markets in May and early June should feed through into this month’s June report, and continue to boost it ahead judging by equity gains since June onwards.

- Citi eye a ~2.5% rebound in portfolio management fees (but note that it “should not be concerning to Fed officials after three sub-target monthly annualized readings”) whilst Nomura look for a 4.3% M/M increase in portfolio management & investment advice.

- Jefferies, explicitly talking about portfolio management, a large subset of portfolio management & investment advice which has seen -7.1% in Apr, flat Mar and +8.1% in Feb, expect it to “contribute significantly to PPI this time around” on the resulting increase in AUM with “markets rebounding to near-record highs in June”.

- Weighing 1.7% of core PCE, it dragged -0.01pp from M/M core PCE inflation in May after a heavy -0.11pp in April. A 3% M/M increase in June, meeting somewhere between the Citi and Nomura estimates, who are both a little above the median for core PCE, would add roughly 0.05pps to core PCE.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Roundup: EIB, IBK, Hungary on TAP

Jun-16 11:28

- Date $MM Issuer (Priced *, Launch #)

- 06/16 $Benchmark EIB 7Y SOFR+53a

- 06/16 $Benchmark IBK 3Y SOFR+58a, 5Y +45a

- 06/16 $Benchmark Hungary +5Y, +10Y, +30Y

- 06/13 No new issuance Friday, $22.8B total on week

OUTLOOK: Price Signal Summary - Bund Support Remains Intact

Jun-16 11:14

- In the FI space, Bund futures have traded lower today, extending the reversal from Friday’s session high. For now, the move down is considered corrective and key short-term support to watch lies at 130.12, the Jun 5 low. A break of this level would highlight a stronger reversal and undermine the bullish theme. Key short-term resistance and the bull trigger, has been defined at 131.95, the Jun 13 high.

- A bullish condition in Gilt futures remains intact and Friday’s steep sell-off from the session high is for now, considered corrective. The move higher last week marks an extension of the recent breach of resistance at 91.87, the May 20 high. This signals scope for a test of 93.73, a 1.764 projection of the May 22 - 27 - 29 price swing. Note the uptrend is in overbought territory, a deeper pullback would unwind this position. First firm support lies at 92.04, the 20-day EMA.

STIR FUTURES: UPDATE on Large Dec'25 & Mar'26 SOFR Volume

Jun-16 11:10

- Reportedly over 72,500 SFRH6/SFRM6 spds sold at -0.195 - hitting the bid, remains well offered.