US DATA: Soft Underlying Import Dynamics Underpin Narrowing Trade Deficit

Dec-11 14:26

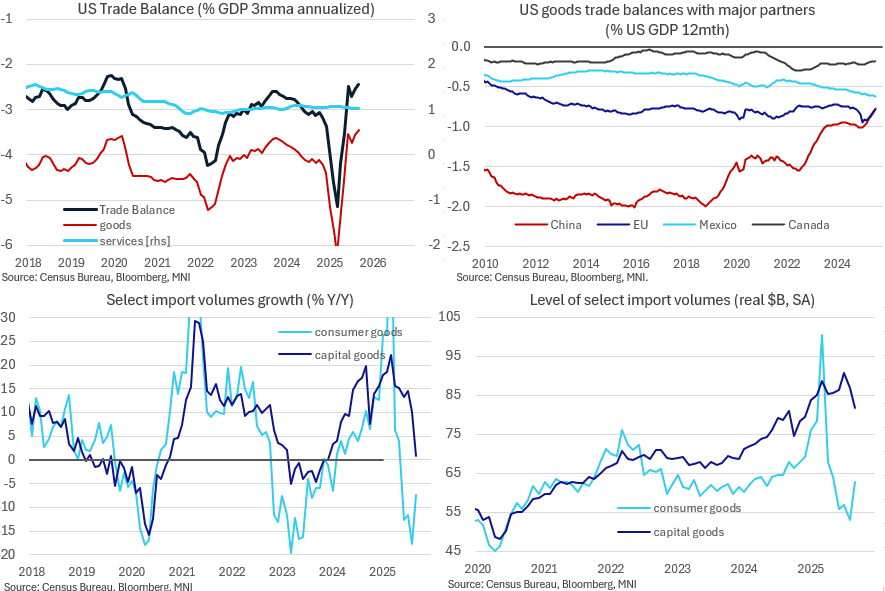

September's goods and services trade deficit came in on the smaller side of expectations, at $52.8B ($63.1B consensus) - the smallest shortfall since June 2020. It's a far cry from the $100+B deficits in the 1st quarter, and came on the back of the smallest goods deficit since September 2020 ($79.0B). This should be positive in terms of the readthrough for Q3 GDP and maintains the trend of narrowing deficits as the tariff regime settles in.

- The services surplus was steady at $26.2B, the 21st month in a row that it's printed with a 25/26/27B handle.

- As a percentage of GDP the 3-month moving average of the overall goods and services deficit has edged down to 2.4%, compared with just over 5% in Q1 for the smallest shortfall since before the Covid pandemic.

- Goods exports jumped in September in both nominal (3.0% M/M) and real (4.2%) terms, with volumes now up 3.0% Y/Y. Contrast this with imports which are down 6% Y/Y in real terms, at the same level seen at the start of 2024.

- Consumer goods imports soared 18% M/M in September in real terms - which was due entirely to pharmaceuticals, which nearly doubled M/M even as other categories fell (front-running a 100% tariff on branded pharma products starting Oct 1).

- But consumer goods imports are down 7% Y/Y and while capital goods have maintained positive growth it's tapered off substantially (0.9% Y/Y vs double digit rises for the prior 15 months). Industrial supplies import volumes dropped 11% Y/Y, the sharpest fall since early 2023 and leaving the level around the lowest of the 2000s.

- We take particular note of the drop off in capital imports, as the recent surge had coincided with strong domestic business capex.

- The pharma jump in turn was attributed to imports from Ireland, which at $19.9B in September basically meant that the US imported as much in goods from the Irish as from China ($20.1B) in September.

- While the September pharma jump is a one-off, this is part of a broader trend in which the US goods trade deficit with China has fallen to below 1% of GDP from 2% pre-pandemic, putting it on a par with the EU as a whole (0.8% of GDP).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: SFIG6 96.60/96.70/96.75/96.85 Call Condor Lifted

Nov-11 14:23

SFIG6 96.60/96.70/96.75/96.85 thin body call condor paper paid 1.5 on 9K.

GILTS: Tsy Bid Drives Fresh Demand, Resistance In Futures Remains Intact

Nov-11 14:07

Spill over from the post-ADP weekly employment data move in Tsy futures drives fresh demand for gilts in recent trade.

- Futures trade as high as 93.95, nearing resistance at 93.98.

- A break would reignite bullish momentum and switch focus to nearby round number resistance at 94.00, followed by some Fibonacci projections (94.24 & 94.60).

- Yields now ~8bp lower across the curve, with fresh session lows registered across the curve.

- Only 2s have broken below October yield lows when it comes to benchmark yields.

SONIA OPTIONS: Call Structures Bought

Nov-11 14:00

Demand for call structures in recent trade:

- SFIZ6 96.75/97.00/97.25 call fly paper paid 3.75 on 5.25K

- 0NU6 96.70/96.80 call spread and 97.10/97.20 call spread paper paid 6.25 on 7.5K