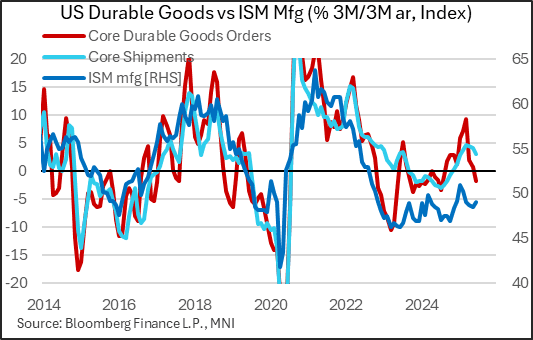

US DATA: Slowing Momentum In Core Durables Orders Points To Softer Investment

June's advance durable goods report showed renewed weakness in core orders to end Q2, a potential sign of softer business investment and manufacturing in the months ahead.

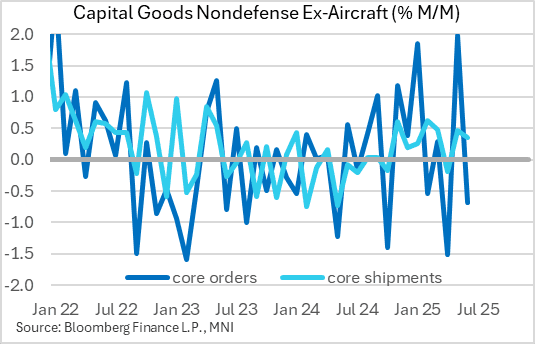

- Once again, the headline durable goods orders reading showed extreme volatility, falling 9.3% M/M after rising 16.5% in May (upwardly revised by 0.1pp), due to nondefense aircraft orders contracting by 52% after a 232% rise.

- While that beat consensus (expected -10.7%), the report overall was weak due to core orders (nondefense ex-aircraft) unexpectedly contracting: -0.7% M/M (0.1% consensus, albeit the contraction came from a higher base as May orders growth was revised up 0.3pp to 2.0%).

- Core orders have been stop-start, alternating between expansion and contraction in each of the last 5 months. Momentum has clearly been waning overall, with the 3M/3M annual rate now down to -1.7% (0.7% prior), the weakest since July 2024 and well down from what is now clearly a tariff front-running boosted 9.2% high in March (which was the strongest momentum in 35 months).

- Prior orders mean core shipments continue to pick up, growing 0.4% M/M in June after 0.5% in May, though momentum overall is beginning to roll over (see chart).

- On a Y/Y NSA basis, things look healthier, with core orders up by a 31-month high 5.0%, but we take more signal from the pullback in sequential momentum.

- Category-by-category dynamics were mixed. There were notable M/M contractions in computers/related products and communications equipment, with capital goods ex-aircraft declining for the 2nd month in 3. On the other hand, machinery orders rose by a healthy 0.4% for a 2nd consecutive month, with orders of electrical equipment/appliances, and primary and fabricated metals products, continuing to rise.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Aggressive sellers in Treasuries

- Some aggressive sellers in Treasuries, nothing too big, but through intraday lows.

- While the 30yr futures have been leading lower, the 10ytr part of the curve is catching and EGBs are weighing on US Treasuries.

- That latest leg higher in Yield, helps the USDJPY towards the 146.00 figure, and seeing broader highs for the Dollar here.

RIKSBANK: Breman: Market Participants Don't Trust CBs Enough

An interesting quote from Breman at the BOE conference: "My experience, and this is not in the speech, it is that the general public, regular households, especially when times are uncertain, they want clarity on what's going to happen to mortgage rates, etc, and they almost have too much of trust in the central bank; market participants, not quite as much."

RIKSBANK: Breman Praises Riksbank Transparency; Advocates CB Scenario Use

There doesn't seem to be much market moving in Riksbank First Deputy Governor Breman's speech, but it's an interesting assessment of the Riksbank's transparent communication processes.

- Re-iterating that the rate path is a forecast not a promise: "It is therefore crucial that it is made clear that the policy rate path is indeed a forecast − and that the transparency applies to the forecast, not the policy going forward. The latter is simply very difficult to be transparent about far in advance. The fact that the interest rate forecast is a “forecast and not a promise” has been something of a mantra in the Riksbank’s communication over the years. "

- "As the economy is constantly hit by various shocks, the policy rate path that is expected to produce this inflation trend will need to be changed more or less constantly. The fact that interest rate forecasts are not seldom wrong is therefore “a feature, not a bug”.

- "My assessment is that it will become increasingly common for scenarios to play a role in monetary policy communication. This is, of course, particularly true if the global macroeconomic environment continues to be characterised by large and frequent shocks. Scenarios become a natural way for the central bank to analyse and communicate different risks. And, as is the case with most other communication tools, the more central banks use them, the more economic agents will become accustomed to and familiar with alternative scenario"

- "I can only account for the Riksbank’s experiences during the almost eighteen years that we have included names in the minutes. In my view, this has increased the transparency of the judgements made by different members of the Executive Board on different issues, and this in turn has made it easier for households, firms and market participants to understand both the policies we are pursuing and how they might change"