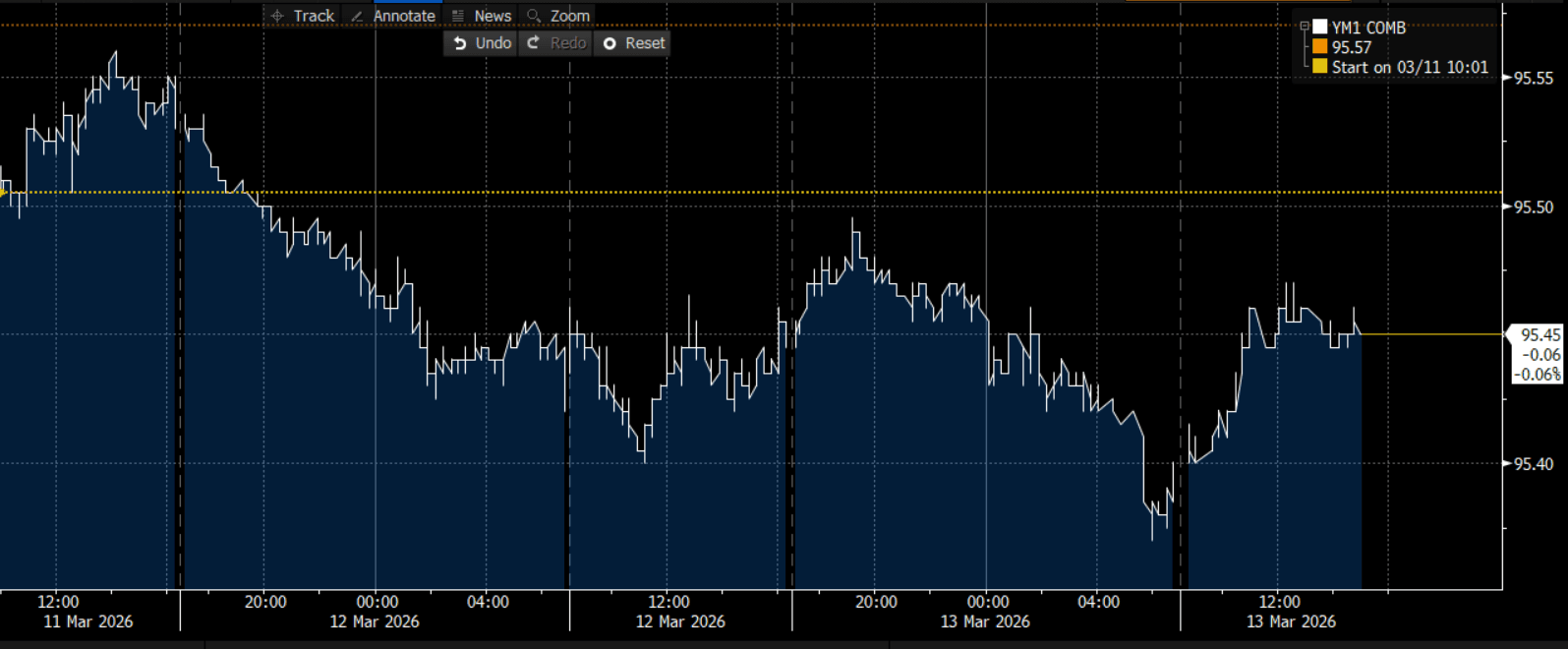

AUSSIE BONDS: Slightly Stronger As Early Losses Reversed

ACGBs (YM flat & XM +2.5) are slightly stronger, reversing early weakness driven by overnight losses for US tsys.

- (Bloomberg) “Goldman Sachs says the conflict in the Middle East could send the oil price as high as $US150 a barrel amid growing fears that a crucial channel will remain closed for months. The Wall Street investment bank expects oil to peak at around $US150 a barrel should the Strait of Hormuz remain closed for the next two months.”

- Cash US tsys are flat to 1bp richer, with a steepening bias.

- Cash ACGBs are flat to 2bps richer after being 3-5bps cheaper early. The AU-US 10-year yield differential is at +68bps after +71bps early.

- The bills strip is flat to -2 across contracts.

- The local calendar will be empty until next Tuesday's RBA meeting.

- Going into next week's policy decision, RBA-dated OIS pricing implies a 72% probability of a 25bp hike, up from 35% at last Friday's close.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising to 165% by June and 277% by December 2026.

- Next week, the AOFM plans to sell $1000mn of the 4.25% 21 March 2036 bond on Wednesday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

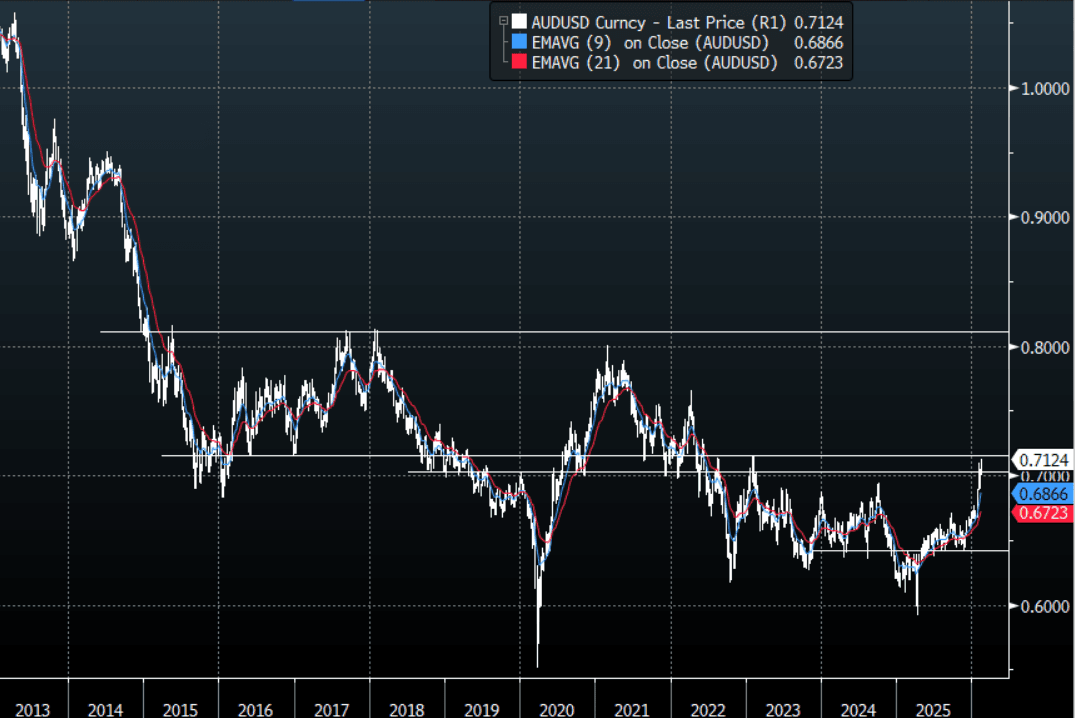

AUD: AUD/USD-Extends Above 0.7100 As Hauser Says: "Will Do What's Necessary"

The AUD/USD has had a range today of 0.7067 - 0.7128 in the Asia- Pac session, it is currently trading around 0.7125. The AUD took another leg up across the board as the market reacted to Hauser saying they “will do what's necessary to return inflation to target”. The USD is again back under pressure and the move lower in yields overnight is just adding to its headwinds, the AUD remains a favourite vehicle to express a long against it. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7040–0.7070 area, and then the 0.6950 area. The bulls will be looking for dips to remain supported in order to break above the pivotal 0.7100-0.7200 area. A sustained break above here targets 0.7600-0.7800 first and then 0.8000-0.8200.

- "HAUSER: WILL DO WHAT'S NECESSARY TO RETURN INFLATION TO TARGET" - BBG

- MNI BRIEF: Stronger Demand Drove Hike - RBA's Hauser. The RBA’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply. The reason policy turned around in February is because the facts changed,” he said, referring to last week’s decision.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7010(AUD560m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6850(AUD933m Feb 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 80 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

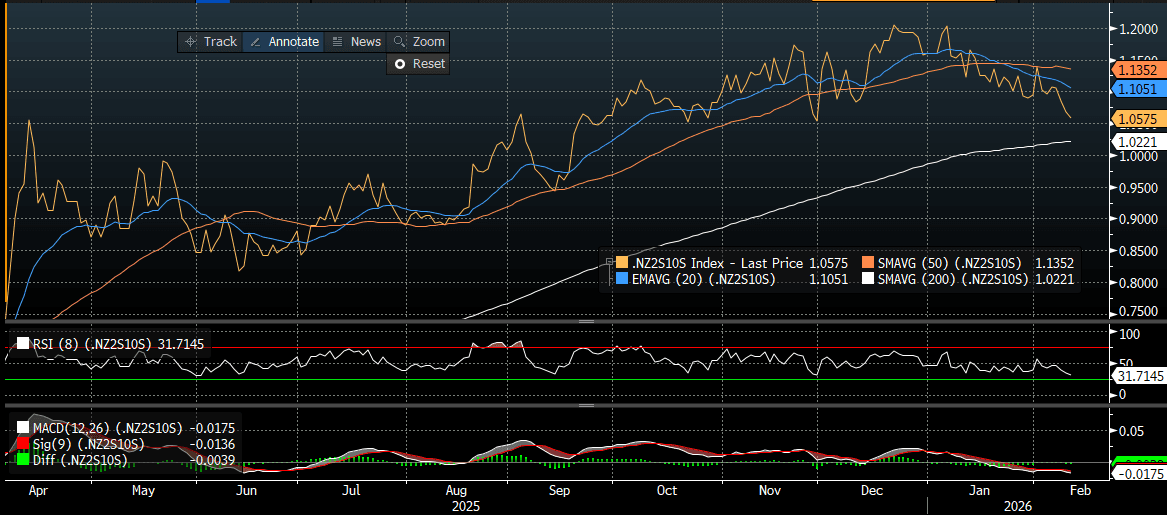

BONDS: NZGBS: Bull-Flattener Leaves Curve At Its Flattest Since Nov

NZGBs closed showing a bull-flattener, with benchmark yields 2-4bps lower.

- Nevertheless, NZGBs underperformed ACGBs with the NZ-AU 10-year yield differential 2bp wider on the day.

- There has no cash US tsys dealings in today’s Asia-Pac session, with Japan out on holiday.

- (Bloomberg) “New Zealand’s government has started an independent review of New Zealand’s monetary policy response to the Covid-19 pandemic. Purpose of the review is to identify lessons New Zealand could learn to improve the monetary policy response to future major events.”

- Swap rates closed 2-5bps lower, with the 2s10s curve flatter. At 1.06, the curve is at its flattest since late November (see chart).

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 43bps.

- The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

OPTIONS: +$3bn In USD/JPY Options So Far Today, O/N Vol Elevated Ahead Of NFP

In the FX option space, JPY volumes have dominated so far in Wednesday trade, with around $3.1bn in total volumes so far. This is 46.6% of total volumes, per DTCC via BBG and comes despite onshore markets in Japan being out today. Next on the volumes list is USD/TWD with 10.8% of total volumes. AUD/USD, which has broken above 0.7100 for the first time since 2023 just under $600mn in FX options volumes so far today (around 9.5% of total).

- For USD/JPY, the larger volume transactions ($100mn or more), are mostly for puts, with a variety of strike levels. A 143 strike, expiry end April this year was executed for +200mn per DTCC. This comes as USD/JPY continues to unwinds its pre-election bounce, amid signs that government wants to earn the markets trust around fiscal policy etc. Softer US yields are also weighing on USD/JPY.

- USD/JPY risk reversals are rolling back over, but are above late Jan lows. The 1 month is around -1.64.

- In the vol space, overnight vol is elevated near 16.45%, which reflects the upcoming US payrolls print later. Other implied vol measures are sub 10%.