AUSSIE BONDS: Slightly Richer, RBA Bullock: Cautious, NVDA Beats, Q4 Capex Due

ACGBs (YM +1.5 & XM +1.0) are stronger after a modest cheapening by US tsys overnight. * KC Fed Sch...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.710 @ 15:51 GMT Jan 23

- SUP 1: 95.655 - Low Jan 23

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices fell sharply on the stronger-than-expected jobs print last week, pressuring prices again to recent lows. This adds to pricing for additional RBA tightening this year - which should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

AUSSIE BONDS: Futures Up But Near Recent Lows, NAB Survey Today, Q4 CPI Tomorrow

Australian markets have returned from yesterday's break, with bond futures edging a little higher in the first part of trade. This follows a mostly positive lead from offshore markets on Monday, with both US Tsy and JGB futures biased higher. For 3yr futures (YM) we were last 95.695, +1.5bps. This still leaves us within striking distance of recent lows, while 10yr futures (XM) were at 95.14, +1bps. With 95.275 cleared for the 10yr, prices are pushing to new contract lows, opening vol-band support through 95.113 and into 94.269. Any recoveries need to break back above 95.900 to signal near-term bullish traction. In the cash ACGB space, yields are higher led by the front end.

- The 3yr bond yield was last near 4.27%, just short of recent highs. Focus will be on upside momentum towards the 4.45/50% region, levels last seen in 2023. Moves under 4.10% should draw support.

- The key near term focus point will be tomorrow's CPI print for Q4 (and the monthly Dec outcome). Market pricing has close to a 60% chance of a Feb hike.

- The AU-US 10yr spread is back above +60bps, with tighter spreads likely to draw interest for re-widening plays as risks around the RBA-Fed outlook diverge in the near term.

- The 3/10s curve is maintaining a flattening bias, last +55bps.

- The local data calendar has a Dec NAB business survey and conditions today. Also we have a 2031 debt sale.

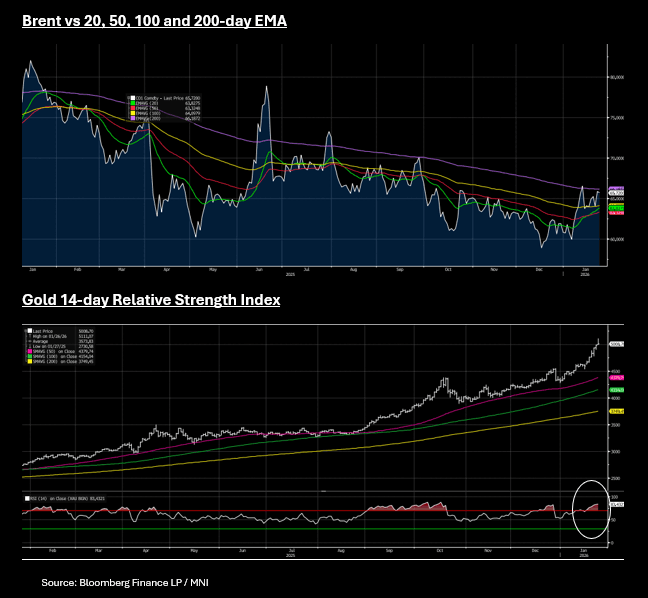

COMMODITIES: Supply Concerns Pressure Oil as Gold Closes Above $5,000

- Oil's price action overnight put the winter disruption to one side and seemed to focus on the various supply led stories.

- A severe winter storm in the US disrupted significant crude and natural gas production over the weekend, with estimates of up to 2 million barrels per day lost, with full restoration expected by January 30.

- Kazakhstan's largest oil producers is readying the huge Tengiz oil field to resume output following disruptions caused by fire the impact of which reduced the country's overall oil output by approximately 40% over the last month. This comes as the Kazakh Black Sea port damaged by drone attack is back and operational following repairs, having been operating at a reduced capacity since mid-November.

- Chevron has sent 15 ships to Venezuela to expedite the export of crude from the country as the US's grip over the country's oil sector tightens.

- WTI finished in the US down -0.72% at US$60.63 bbl near to downside resistance via the 100-day EMA of $60.19

- Brent finished down -0.36% at US$65.64 bbl near to the topside resistance via the 200-day EMA at US$66.18.

- Gold closed above $5,000 for the first time at US$5,008.72 and ahead of many investor's year end forecast. Gold finished the US trading day up +.043% Monday to cap its sixth straight day of gains, moving the precious metal further into overbought on the 14-day relative strength index.

- Gold's rise continued even as equities are normalizing following the geopolitical tensions over Greenland