AUSSIE BONDS: Slightly Mixed Ahead Of Monday's ANZAC Day Holiday

ACGBs (YM -2.0 & XM +0.5) are slightly mixed after a data light session ahead of Monday's ANZAC Day ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Twist-Flattener As Geopol Optimism Strengthens

At the Tokyo lunch break, JGB futures are stronger, +10 compared to settlement levels.

- The market has been buoyed by optimism around Washington's diplomatic push to resolve the Middle East conflict. Cash US tsys are 2-4bps richer in today's Asia-Pac session.

- The US has drafted a 15-point plan intended to help bring the war with Iran to a close, according to people familiar with the matter. – BBG

- However, The Spectator Index on X: "Iran has demanded closure of US bases in the Gulf, end of all sanctions, end of Israeli campaign against Hezbollah and a framework that would allow it to collect fees from ships transiting through the Strait of Hormuz, as part of a response to Trump proposal, according to Wall Street Journal report."

- MNI: BOJ Minutes: Neutral Rate Difficult To Assess. Most Bank of Japan board members agreed the neutral rate remains difficult to identify in advance, underscoring the need to gauge it gradually by assessing the impact of each rate hike on economic activity and prices, minutes of the Jan 22-23 meeting showed Wednesday.

- Cash JGBs have twist-flattened across benchmarks, with yields 1bp higher to 4.5bps lower.

- Tomorrow, the local calendar will see PPI Services and Investments Flow data alongside Enhanced-Liquidity Auction 1-5 YR.

Source: Bloomberg Finance LP

AUSSIE BONDS: Strong Rally On US's Push To End Middle East Conflict

ACGBs (YM +11.5 & XM +9.5) are sharply stronger but a tad off session bests.

- Inflation pressures appear to have stabilised before fuel prices jumped in response to supply fears following the closure of the Strait of Hormuz. February CPI inflation was slightly lower than expected with headline at 3.7% y/y after 3.8% and trimmed mean 3.3% y/y following a downwardly revised 3.3%, and around the rate seen since October.

- We won't get a feel for any second-round effects from higher fuel prices until March CPI (29 April) at the earliest, but the March PMI showed increased cost pressures being partially passed on.

- Cash US tsys are 2-3bps richer in today’s Asia-Pac session following Washington's diplomatic push to resolve the Middle East conflict.

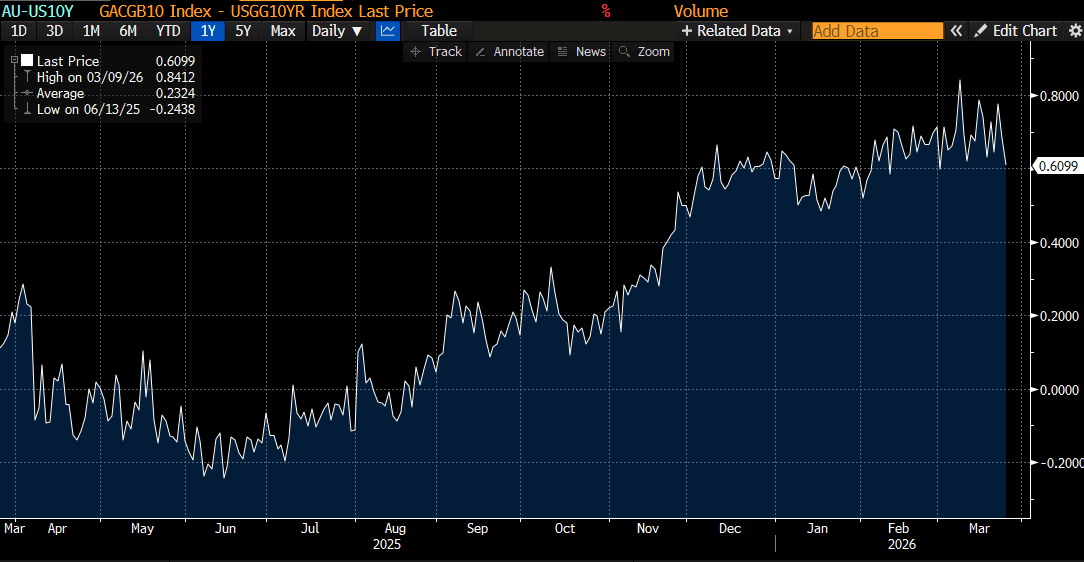

- Cash ACGBs are 9-12bps richer with the AU-US 10-year yield differential at +61bps, the lowest since early March.

- The bills strip has bull-flattened, with pricing +9 to +16 across contracts.

- RBA-dated OIS pricing is softer today but continues to show tightening across all meetings, with the probability of a 25bp hike rising from 59% for May to 148% by August and 223% by December 2026.

- Tomorrow, the local calendar will see a speech from RBA Kent at the KangaNews Debt Capital Market Summit.

Bloomberg Finance LP

ASIA STOCKS: Solid Gains, But Uncertainty On Iran Conflict Outlook Remains

Asian bourses are mostly up firmly for Wednesday trade. Sentiment was aided late in US trade on Tuesday, as headlines crossed around the US reportedly proposing a one-month ceasefire in terms of the Iran conflict, as well as sending Iran a 15 point plan to end the conflict. Still, the WSJ has reported on Iranian demands, which includes the closure of US bases in the Gulf. Via the WSJ: "A U.S. official called the demands ridiculous and unrealistic." This has taken some of the shine off the risk rebound, although US equity futures remain comfortably in the green at this stage. Eminis were last up +0.75%. Oil prices are still down comfortably for the session, but up from session lows (Brent last near $99.35/bbl)

- In regional Asia Pac markets, we have seen tech related plays outperform. Japan's Topix and NKY 225 are both up over 2%. The BOJ Mins, as usual displayed a wide variety of viewpoints, while noting it was difficult to determine where the neutral rate was. However, the majority of members noted it was desirable to make policy decisions at each meeting without committing to a specific pace, while carefully assessing economic activity, prices and financial conditions.

- The Kospi is up 1.95%, while Taiwan's Taiex is up around 2.9%. Earlier trends showed offshore investors buying local stocks, but this afternoon has seen this flick back to net selling, which has been the predominant theme since the start of the Iran conflict.

- China and Hong Kong markets are firmer, but lag the gains seen elsewhere in North East Asia.

- The ASX 200 has climbed 1.8%, with earlier data showing a slightly weaker than expected Feb inflation print, but this pre-dates the Iran conflict impact.

- Indonesian markets have also returned from the break for the past week, opening up firmer with gains currently around 1%. We are coming from depressed levels though, with lows pre the holiday period under 7000 (the JCI was above 9000 in Jan).

- Other SEA markets are mostly up between 1-2%.