PRECIOUS METALS: Silver Continues Outperformance Following Fed Decision

Gold continued to underperform silver after the Fed eased policy as expected but maintained its one rate cut for 25bp suggesting the bar has been lifted for further easing given rates are now in its “neutral” range. “Additional adjustments” will be data and outlook dependent. The Fed is even more uncertain for 2026 than usual as Chair Powell’s replacement is likely to be more dovish, supportive of precious metals, but inflation continues to print above target.

- The Fed outlook remains cautious with the market pricing in only a 20% chance of a 28 January cut but 140% of a June one. The OIS market and therefore gold will remain very sensitive to data releases, especially the labour market.

- Silver and gold were supported by the fall in the US dollar (BBDXY -0.4%) and US yields. Silver jumped another 1.9% to $61.811/oz, reaching a new record high of $61.951, and up 6% this week. In comparison, gold rose 0.5% to $4228.84/oz but is only 0.7% higher this week and has been in a fairly narrow range.

- Silver broke above two resistance levels opening $62.937 reinforcing the bullish trend. The metal is currently around $61.91 after rising to $61.976, another record.

- Gold prices reached a high of $4228.84 following the Fed after falling to $4182.14, holding above the 20-day EMA at $4155.2. Gold has not been able to break above initial resistance at $4264.7, a retracement level, and is currently around $4232.5. Technicals remain bullish.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

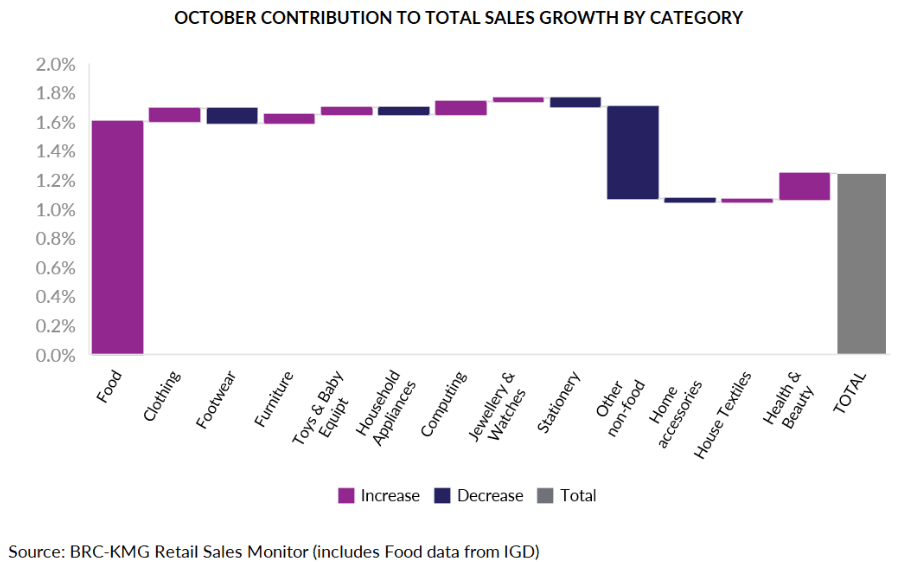

MNI: UK BRC OCT BY VALUE SHOP SALES LFL +1.5% Y/Y, TOTAL +1.6% Y/Y

- MNI: UK BRC OCT BY VALUE SHOP SALES LFL +1.5% Y/Y, TOTAL +1.6% Y/Y

UK DATA: BRC Retail Sales Values Only Increase Y/Y Due to Food Inflation

BRC Retail Sales slowed again in October, posting a 1.6% Y/Y increase in value terms (vs 2.3% September). The year-on-year growth in the value of retail sales was the weakest since May and was almost entirely driven by food sales, which in turn were almost entirely driven by food price inflation.

- Food sales rose at a slower pace than September, rising 3.5% Y/Y (vs 4.3%). Again, the press release noted that the positive figure "was mostly driven by higher prices rather than higher volumes". The year-on-year rate is now at its lowest since May, but we note that the BRC shop price index and official ONS data both show a slowdown in food price inflation recently, so its hard to know how whether there is much of a slowdown here in volume terms.

- Non-food almost flatlined at 0.1% Y/Y (vs 0.7% Sep), mostly driven by a notable downward contribution from the "Other non-food" subcategory. Note that when taking into account inflation, non-food sales volumes were probably overall lower than a year ago.

- The press release highlighted that October saw a slowdown in the sale of many household goods, after sustained strength "linked to the lagged benefit from the house buying surge seen before Stamp Duty changes in Spring". Upcoming releases should show whether this is a result of a moderation in the housing market or more cautious consumers.

- Consumers awaiting Black Friday deals, as well as continued Budget-driven caution and subdued consumer confidence were also highlighted as downward drivers by the BRC.

- The ONS's retail sales volume index will see October data released on 21 November, following four consecutive M/M increases including a 0.5% M/M rise in September. Today's BRC release covers the same 4 weeks as the ONS report (from 5 October - 1 November 2025).

CNH: USD/CNH Risks Still Appeared Skewed Lower, Nov/Dec Seasonals May Help

Spot USD/CNH risks still appear skewed lower, although we couldn't sustain sub 7.1200 intra-session lows on Monday. We track just above this level in early Tuesday dealings. The broader backdrop hasn't changed with moves back into the 7.1300/1.1400 area likely to draw selling interest, while a break above 7.1500 (with the 100-day EMA near 7.1510), is likely needed to shift mindsets around fading upticks in the pair. Downside focus is likely to rest around the 7.1000 area (which remains the consensus estimate for year end USD/CNY levels). Note that CNH seasonality is positive into year end. CNH has risen in each Nov and Dec since 2017, except for 2024.

- Spot USD/CNY ended Monday at 7.1186, while the CNY CFETS basket tracker edged down a little further to 97.93, still close to recent multi month highs.

- USD/CNH implied vols have ticked up slightly, but at 2.25% for the 1 month remain very close to recent cycle lows. The 1 month risk reversal is range bound but at -0.39 still favours puts over calls.

- Cross asset trends were mixed with not a lot of change in US-CH yield differentials. The 2yr spread is around +214bps, with recent lows sub +200bps coinciding with USD/CNH testing under 7.1000.

- Late yesterday BBG noted declining car sales in China for Oct ("Retail sales of passenger vehicles fell 0.8% in October from a year earlier, according to data from China’s Passenger Car Association.", which is still likely to keep the focus on further policy support, although the inflation bounce in Oct may delay the timing.

- The local data calendar is empty, with Oct new loans/aggregate financing data due between now and this Saturday.