USD: Should The USD Have Performed Better ?

The BBDXY range overnight was 118843 - 1195.52, Asia is currently trading around 1190. The BBDXY initially gapped higher around 0.5% but again failed miserably to hold onto these gains and was very quickly sold back down. The price action is particularly poor given the surge in US yields and a market that is supposedly extremely short. The USD has opened slightly lower in the Asian session, -0.10%. The larger picture remains one of USD weakness and in the current environment rallies should continue to be met with supply, first resistance is back towards the 1205/1215 area.

- Robin Brooks on X: “Dollar weakness so far this year is based on markets forecasting recession. But the US economy continues to surprise positively, including with today's payrolls. That means cyclical weakness in the Dollar is very vulnerable to a reversal, especially if US inflation picks up...”

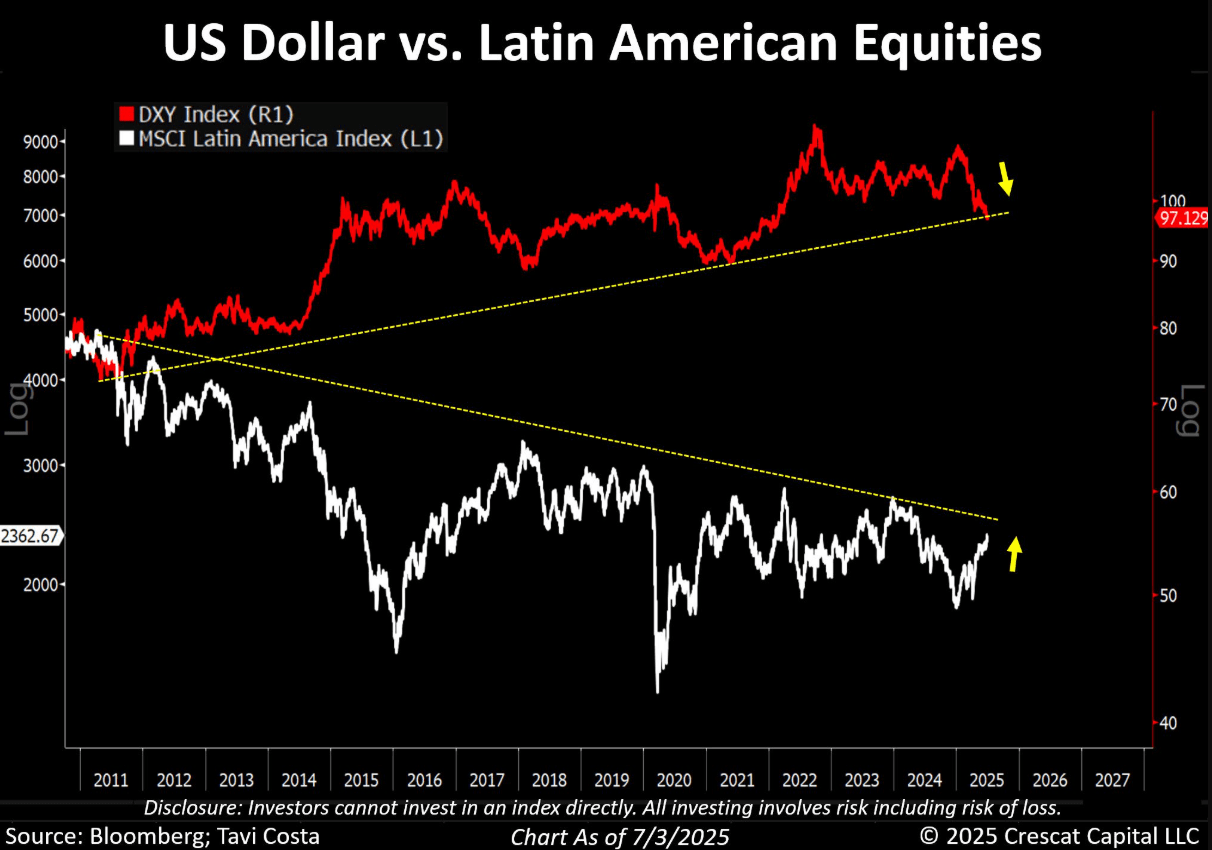

- Otavio Costa on X: “US Dollar vs. Latin American Equities: A classic macro alligator mouth that, in my view, is likely to close as global investors begin rotating out of US dollar-based assets. Emerging market equities remain one of the most fundamentally undervalued areas of the market and have historically benefited significantly from prolonged declines in the dollar, in my view. I believe that shift is beginning to unfold now.” See Graph below.

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. This consensus will also result in some decent short squeezes as a lot of the market is positioned the same way.

- Data/Events : NFP, S&P Global Services PMI, ISM Services Index, Factory Orders, Durable Good Orders

Fig 1: US Dollar vs. Latin American Equities

Source: MNI/@TaviCosta/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

THAILAND: Thailand Manufacturing Outperformed In May

Thailand was the only country in Asia to show an increase in manufacturing activity and positive growth in the sector in May. The S&P Global manufacturing PMI rose to 51.2 from 49.5, highest since December, driven by output growing at its fastest in nine months. It signals an improvement in manufacturing growth. Unlike the rest of ASEAN, export orders were higher. The outlook is also positive.

- Business confidence eased but remained well above the historical average despite heightened global trade and economic uncertainty as producers hope that marketing will improve interest.

- The increase in domestic and export orders encouraged hiring and inventory building in May but purchasing eased. Total orders grew for the first time since December with exports positive for the first time in over 18 months which may be due to increased marketing and new product efforts.

- Inflation remained contained with costs low helped by suppliers’ discounting, according to S&P Global, but these were still passed onto customers but selling price inflation remained marginal.

Thailand manufacturing

AUSTRALIA DATA: A$ Dip Post GDP Miss Short Lived, RBA July Easing Odds Firm

AUD/USD dipped modestly post the GDP miss (Q1 growth at 0.2%q/q versus 0.4% forecast). We got to lows of 0.6454, but quickly rebounded. We were last back in the 0.6470/75 region, slightly up on NY close levels from Tuesday. Broader USD sentiment is softer, the BBDXY down close to 0.20% at this stage. The AUD was lagging this weakness, but has caught up now. the AUD/NZD cross is at 1.0760/65, (post data lows were at 1.0752), which keeps us within recent ranges.

- In the bond space, YM spiked higher but quickly reversed. OIS is a few bps softer (more details to follow). There is a 87% chance of July cut up from 79% pre-data.

AUSTRALIA DATA: Soft Q1 Growth Impacted By Weather Events

GDP grew 0.2% q/q & 1.5% y/y in Australia in Q1 as extreme weather events in the quarter impacted domestic demand and exports. This is lower than Bloomberg consensus but in line with revisions by the big 4 local banks following Tuesday’s net exports, government and inventory data. See ABS press release here. More details to follow.