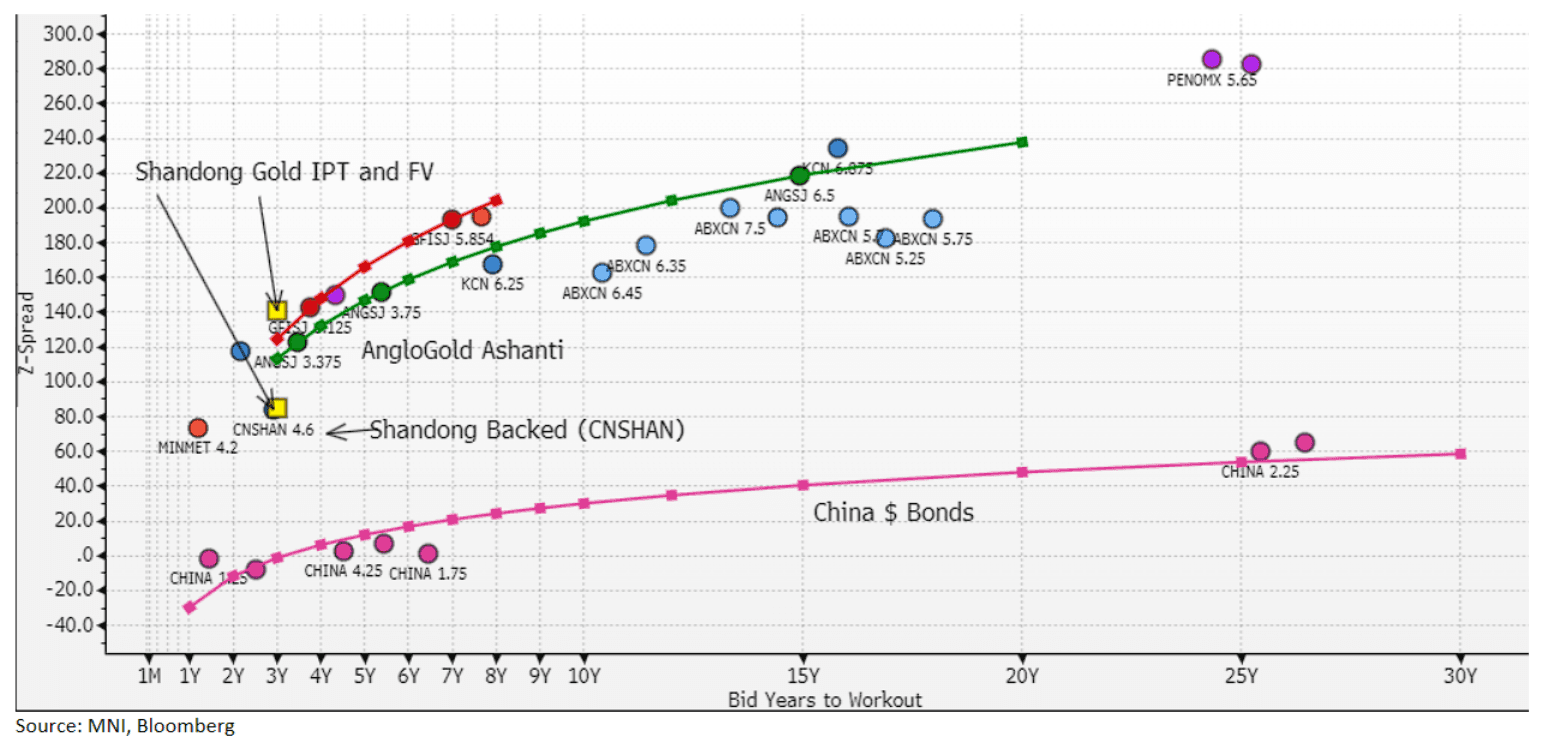

EM CREDIT SUPPLY: Shandong Gold (SDGOLD, NR/BBB-/NR) - FV Estimate

"IPT: Shandong Gold Group $Bmark 3Y Green Reg S 5.2% Area" - BBG

New Issue: $benchmark 3y

IPT: 5.2% area (z+141bp)

FV estimate: 4.65% (z+85bp)

• Shandong Gold Group's (BBB-) wholly owned subsidiary, SDG Finance Ltd (SDGOLD), is coming to the market with a $benchmark 3y green deal for financing, refinancing of green projects. The bonds will be guaranteed by Shandong Gold Group and will also be rated BBB- with S&P.

• Shandong Gold is a state backed (Shandong Province) gold producer, one of the largest in China (Top 2, 17% of China production) and globally (#12) having produced 52 tons in 2024. In all, gold resources are estimated at 2,940 tons, around 56 years of production based on 2024 actual.

• In terms of estimating a fair value, in the chart below we include various emerging market gold producers and the recent $ 3y deal from Shandong Hi-Speed Group (CNSHAN, A3), the most reasonable comparable given the issuer is also backed by Shandong Province.

• We also include China $ bonds for a guide on the curve, Shandong Province hasn’t any USD outstanding.

• On the high end of the pricing range, if we focus on ratings and compare Shandong Gold to South African, AngloGold Ashanti (Baa3/BB+/BBB-), we would get to a z-spread of around 113bp at the 3y point (c. 4.9%). That said, Shandong Gold, like its core product, is a rare issuer and I would expect there to be strong demand and that pricing will be driven the ultimate backing from Shandong Province.

• The recent Shandong Province backed CNSHAN 3y deal would indicate a fair value around z+85bp (4.65%). We see fair value at similar levels for the new deal, and estimate the 3y at Z+85 (4.65%), though mindful it could trade tighter based on rarity.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBA Dated OIS Pricing Softer Ahead Of RBA Minutes (April)

RBA-dated OIS pricing is flat to 4bps softer across meetings today.

- A 50bp rate cut in May is given a 39% probability, with a cumulative 121bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Today Vs. Yesterday

Source: MNI – Market News / Bloomberg

MNI: CHINA PBOC CONDUCTS CNY164.5 BLN VIA 7-DAY REVERSE REPO TUES

- CHINA PBOC CONDUCTS CNY164.5 BLN VIA 7-DAY REVERSE REPO TUES

CNH: USD/CNY Fixing Edges Down

The USD/CNY fix printed at 7.2096, versus a BBG market consensus of 7.3075.

- The fixing is down from yesterday's 7.2110 outcome, and is also in line with a lower market estimate today compared to yesterday. The fixing error didn't change much, coming in at -979pips.

- A higher fix today compared to yesterday's level (despite further USD weakness) would have likely driven a fresh move higher in USD/CNH.

- This scenario has been avoided and USD/CNH is down modestly, back under 7.3100. Earlier highs in the pair were at 7.3189.