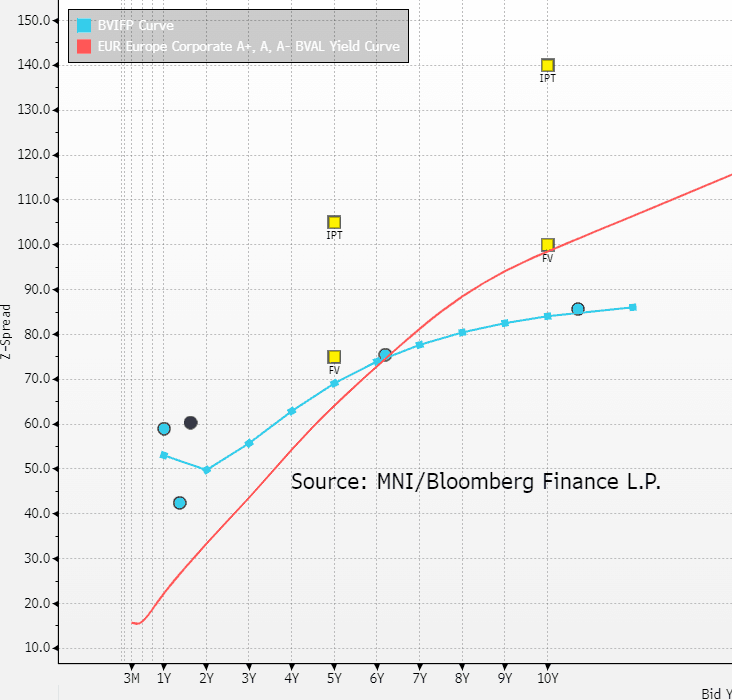

EU HEALTHCARE: SGS: Dual Tranche FV

• IPT: €500m WNG 5yr ms+105-110bps; FV ms+75

• IPT: €500m WNG 10yr ms+140-145bps; FV ms+100

• Comps: BVIFP 3.125 31 6.2yrs z+74; BVIFP 3.5 36 10.7yrs z+83 (A3 Stable)

• UOP: to pay for ATS acquisition.

• Non-Acquisition Event clause. 1st Apr 2026 test date.

Bureau Veritas is the clear comp. The two companies are very similar in terms of size and scope. BVIFP is A3 stable. SGS is A3 on Neg since March last year. The new CEO at SGS is embarking on turnaround strategy to raise margins to high teens and to grow revenues by 4-5% annually until 2027. The ATS acquisition will see Net Leverage go up by 0.2x to ~2.0x after synergies.

Dark Blue circle is the SGSNVX 27s.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Indices are pulling away from Friday's lows

- European and US Equities are pulling away from Friday's lows, the Estoxx futures plummeted 5% from just Thursday's high to Friday's low, VGU5 is now up 0.77%.

- Looking at a Micro level, the Index is close to where it was trading at pre NFP, although we noted at the time of the Employment release the surprising lack of moves in Equities versus what was witnessed in Bonds, Rates and FX.

- This was most likely because of the already big sell off seen in Equities since Thursday into Friday's Data.

- VGU5 was trading at 5234.00, which is right here, and for the US Emini, it was trading at 6320.00, but fell 3.54% from last Thursday's high at 6468.50.

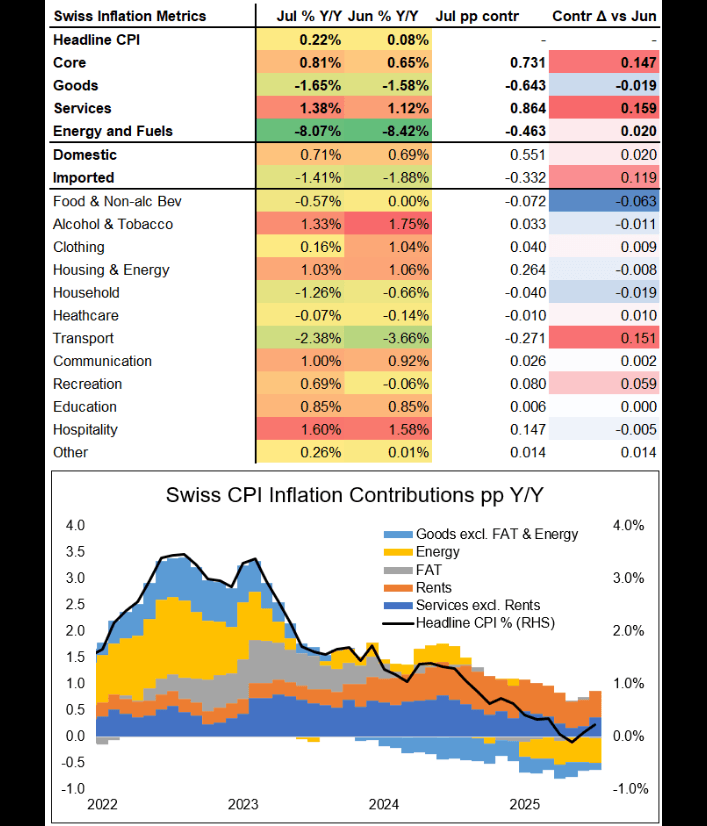

SWITZERLAND DATA: Transport Services Dragged Up July CPI Print

Looking at the details of the Swiss CPI print, upside momentum from transport and recreation categories stands out (contributing a combined 0.21pp more than in June). Overall it remains that this was the second consecutive positive print in Swiss CPI.

⦁ Transport services (airfares but also "public transport abroad" in particular) and package holidays (part of recreation category) were behind the acceleration here, having seen higher Y/Y prints this time - that might help explain parts of the unusual higher services / imported inflation combination.

⦁ Food inflation meanwhile has fallen this time, contributing 0.06pp less than in June.

⦁ Further details see table / chart below:

EGB OPTIONS: Bund Put Fly Buyer

RXU5 128.5/127.5/126.5p fly, bought for 11 in 6.5k.