FED: SF's Daly: Likely Further Cuts Will Be Needed To Support Labor Market

Sep-24 20:19

SF Fed President Daly (non 2025/2026 FOMC voter said in a speech Wednesday that she "fully supported" the Fed's 25bp September cut, and suggested "Moving forward, it is likely that further policy adjustments will be needed as we work to restore price stability while providing needed support to the labor market."

- She notes that the latest Fed Dot Plot showed that further cuts were expected, "but these are projections, not promises, and making good decisions will require us to anchor on our objectives, assess the tradeoffs, and decide, again and again."

- She said re September's cut that "The risks to the economy had shifted, and it was time to act. Growth, consumer spending, and the labor market had slowed, and inflation had risen less than expected, remaining largely confined to sectors directly affected by tariffs."

- Recall Daly has long had a base case of 2 cuts by year-end but said that 3 could be appropriate, noting going into the September meeting that "It will soon be time to recalibrate policy to better match our economy", calling every meeting "live". As such even before this speech, we had expected her to have been one of the 9 participants on the median expecting a rate of 3.6% at end-2025.

- There will me a moderated Q&A after the prepared remarks, livestreamed here.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

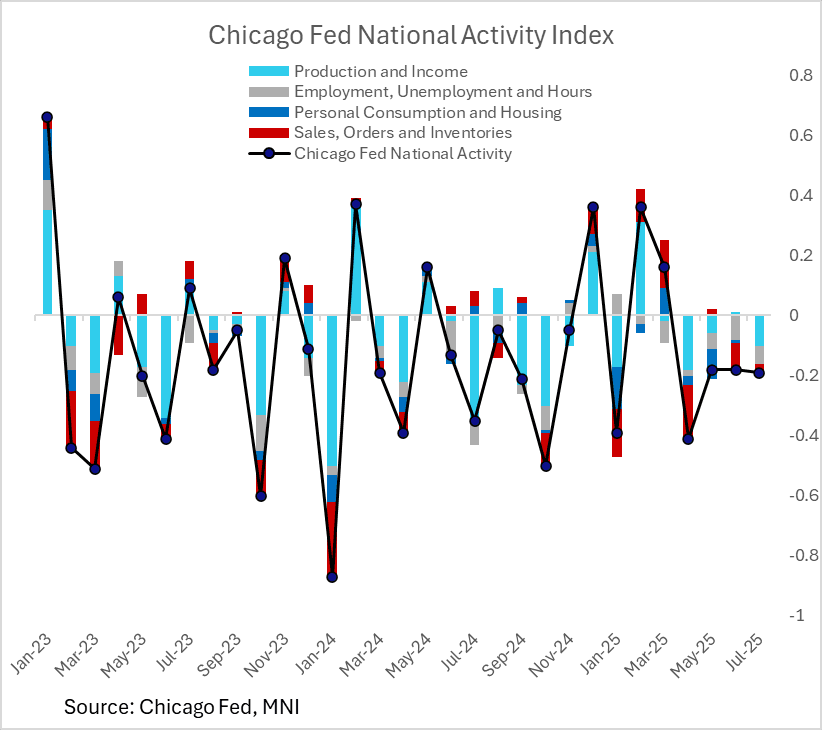

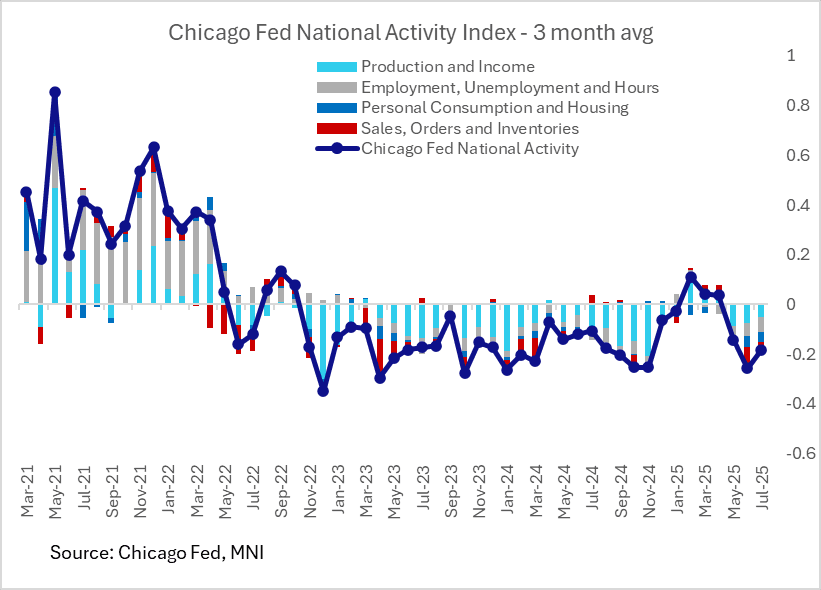

US DATA: Chicago Fed National Activity Index Implies Reversion To Sub-Par Growth

Aug-25 20:14

The Chicago Fed National Activity Index (CFNAI) edged lower to -0.19 in July from -0.18 in June, marking the 4th consecutive decrease in the index suggesting weakening activity.

- After spending 3 months in positive territory from Feb-Apr, the 3-month moving average has reverted to its usual negative territory over the last 3 months. Prior to this brief positive period, the 3-month average hadn't been above zero since late 2022.

- Changes in this index haven't been particularly well correlated with month-to-month or even quarter-to-quarter GDP growth per se (growth has been positive in almost all of the 3-month periods that the CFNAI has averaged negative).

- That said, the index and GDP growth look fairly similar over multi-quarter horizons, and a negative reading doesn't imply contraction, but rather below-average growth.

- In this regard it suggests that a spike in domestic demand/activity in H1 amid tariff front-loading has run its course with the economy starting to slow in H2.

FED: Dallas's Logan: More Room To Go On Reducing Reserves

Aug-25 19:22

Two takeaways from Dallas Fed President Logan's speech on central bank balance sheet policy Monday (which didn't include anything on current monetary policy):

- First, the ex-SOMA manager sees "more room to reduce reserves". While acknowledging what was already in the July FOMC meeting minutes about seeing "some temporary pressure around the tax date and quarter-end in September", Logan says she anticipates market participants will use the standing repo facility if necessary in September. "That will allow us to continue gradually bringing reserves to a more efficient level with market rates close to, but perhaps slightly below, interest on reserves on average over time." This sounds like she is not concerned with the ongoing reduction of reserves warranting a shift in Fed policy in the coming months.

- On this front, she again advocates for further development of so-called "ceiling" tools: "while we have made strides in enhancing the effectiveness of the discount window and Standing Repo Facility, it would be worthwhile to consider further steps, such as increasing or removing limits on the SRF’s size or centrally clearing those transactions."

- Second, she suggests that the Fed could shift to overweighting Treasury bills in its portfolio, over time: "it makes sense for the FOMC to hold primarily Treasuries in the long run, as we’ve repeatedly said we intend to do" and suggests that the Fed could in the long run "make its asset purchases proportional to Treasury issuance. In the medium term, overweighting Treasury bills in our purchases could more expeditiously move our current mix of holdings closer to matching the market."

- However, "the FOMC has made no decisions on the long-run composition of its Treasury holdings, and I look forward to continuing to discuss this topic with my colleagues" - as such this doesn't appear to be an imminent prospect.

- This adds another key update to current FOMC views on balance sheet composition. In June Gov Waller (a possible next Fed chair) concluded in a lengthy speech on the topic: "Though the FOMC has not finalized its desired efficient and effective size and composition of the balance sheet, it seems apparent that today's portfolio should be adjusted. And there are obvious steps to take. We are reducing the size of the balance sheet slowly and need to consider shifting it toward more bills."

US TSYS: Tsys Retreat, Greenback Bounce, Both Unwind Half Fri's Post Powell Move

Aug-25 19:10

- Relatively quiet start to the week with London out for annual bank holiday. Treasuries opened weaker - scaling back a fair portion of Friday's post-Chair Powell speech in Jackson Hole that left the door open to a possible rate cut at the next FOMC annc on September 17.

- NEC director Kevin Hassett (potential Fed Chair candidate) tells CNBC that Chair Powell's Jackson Hole speech showed a Fed that is "late" to cut but that Powell's presentation was "sound" and "data driven".

- Treasury futures maintained losses after higher than expected new home sales - but climbed back to mildly weaker levels on the open. After the bell, Se'25 10Y contract trades -6.5 at 111-30 vs. 111-27.5 low. Support around the 50-day EMA, at 111-13. A clear break of this average would expose support at 110-23+, the Aug 1 low.

- The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k).

- July's building permits were revised up in the final reading to 1,362k (annualized, seasonally-adjusted), vs 1,354k in the initial estimate. That got the data a little closer to the 1,386k consensus estimate going into the initial reading last week, though either way it is a pullback from 1,393k in June (a 2.2% fall vs the 2.8% initially recorded).

- US$ continued to climb in late trade, recovering appr half of Friday's decline. Today's move said to be EUR related after the French confidence vote call earlier. The Bbg $ index: BBDXY +5.94 at 1207.43 vs. 1201.02 low.