EU COMMUNICATIONS: SES: Moody’s Downgrade

(SESGFP; Ba1/NR/BBBneg)

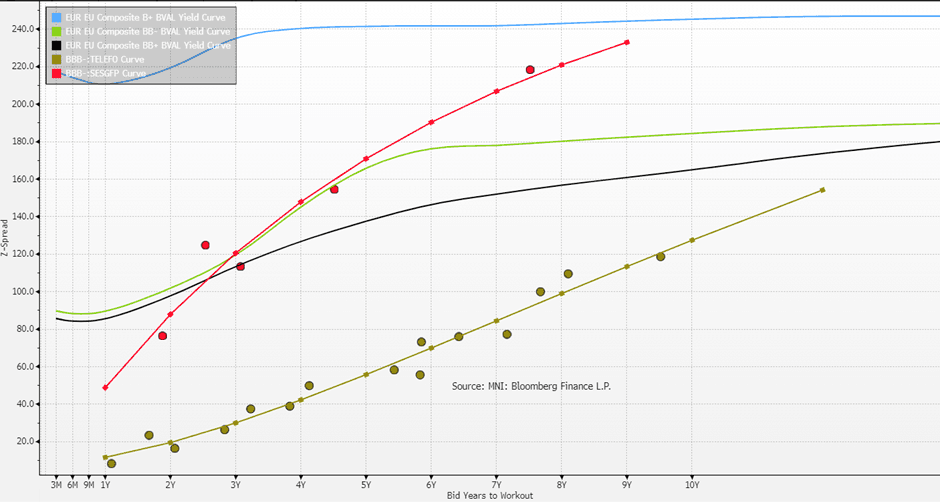

We flagged that management language on IG commitment was notably weaker in the recent post-results call. Senior curve is >20bp wider at the long-end, taking the 33s well past BB+ levels and wide of the BB- BVAL curve. Moody’s have left the name on stable outlook with deleveraging expected in 2027 albeit this will depend on proceeds from FCC C-band auctions.

- Senior notes from Baa3 to Ba1 CFR, hybrids from Ba2 to Ba3. BCA cut to ba2 from ba1.

- “"The DG reflects the material deviation in op performance relative to our previous expectations when we changed the outlook on the rating to negative back in February"

- They flag weak Media, Fixed & Maritime; mix shift to lower-margin Aviation/Gov’t.

- Rebased forecast; EBITDA seen toward €1.7bn by 2027 (vs. 9M25’s €1.2bn; -10% YoY).

- Expected WC optimisation to see Moody’s-adj FCF remain neutral to marginally positive.

- ~€1.5bn in hybrids no longer receive equity credit; ~+0.5x on Moody’s gross lev toward 4.8x.

- The ratio is seen steady in 2026 and move toward 4x in 2027 on C-band monetisation.

- One-notch uplift on Luxembourgish Government’s 20% stake remains intact.

- Downside threshold set at remaining >4x, negative FCF on a sustained basis, gov’t stake sale.

- Upside thresholds set leverage <3.5x and positive FCF.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Citi Recommend SFIH6/Z6 Flattener

Citi have recommended entering a SFIH6/Z6 flattener at -17.0bp, targeting a move to -50.0, with a stop set at 0bp.

- They view the BoE easing cycle as “likely having 3 phases. The first was the regular quarterly rhythm for the first 5 cuts. The second - which is the current - is a risk management phase of slower, irregular cuts awaiting more evidence that disinflation is on track. The third, we suspect, will be cuts to a lower terminal rate than priced, informed by lacklustre growth (impeded by a long list of small tax hikes and ongoing political/fiscal uncertainty), with mounting evidence of growing slack in the labour market, and with CPI realizing close to target later in 2026”.

- They believe that the second/current phase is “fairly priced”, and the “potential third phase that offers the best risk-reward”.

Fig. 1: SONIA Mar '26/Dec '26 Spread (SFIH6/Z6 Spread)

Source: MNI - Market News/Bloomberg Finance L.P.

SONIA OPTIONS: Call Condor

SFIZ5 96.25/96.30/96.35/96.40c condor, bought for 2.5 in 4.5k.

FRANCE: OATs Widening Alongside Peers, But Domestic Political Risks Increasing

The 10-year OAT/Bund spread is back at 75bps, 1bp wider on the day alongside EGB peers. While continued weakness in equity benchmarks looks to be the main driver of recent EGB spread widening, domestic political developments remain a risk to monitor.

- This morning, Le Parisien reported that members of the centre and right “agreed” that they would note vote in favour of the revenue section of the 2026 budget, if it were to be put to a vote in its current form. Link here

- Sources suggest this would be “due to the insincerity of some of the measures adopted”.

- However, the report does not contain information on whether ministers would abstain from a vote, or vote against the motion.

- Ultimately, it underscores the difficult balancing act PM Lecornu is facing. Amendments to the budget to date have already pushed the expected 2026 deficit towards (or above) 5%, versus a target of 4.7%.

- Meanwhile, the Senate starts reviewing the Social Security section of the budget tomorrow. Actions around the 2023 pension reform suspension are in focus.