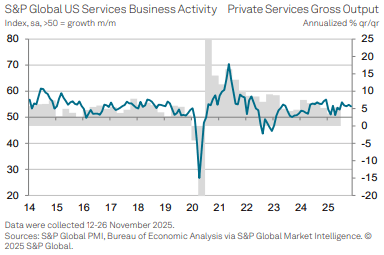

US DATA: Services PMI Revised Lower But Still Solid In Final November Release

[A correction to the original 0956ET bullet, which incorrectly referenced the chart on input cost inflation from the flash November release rather than today's final report. The former clearly showed a still large uptick in the input cost component].

The S&P Global US services PMI was revised lower in the final November release, dipping to its lowest since June rather than confirming what had been its highest since July. Along with this downward revision, input cost inflation was also trimmed somewhat from the highest since Jan 2023 in the flash to today's six-month high.

- US Services PMI: 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct

- US Composite PMI: 54.2 (flash 54.8) in Nov final after 54.6 in Oct

S&P Global US PMI press release opening highlights (release in full, here):

- "The US private sector services economy continued to expand at a solid pace in November, despite growth softening to a five-month low, according to the latest PMI survey data from S&P Global."

- "Activity was supported by the firmest rise in new work of 2025 so far, whilst confidence in the outlook strengthened following the end of the government shutdown and expectations of improved economic growth in the year ahead."

- "Firms also took on additional staff to a stronger degree amid some evidence of capacity pressures, but with reports of higher labor costs and tariffs continuing to push up prices in general, input cost inflation accelerated to a six-month high."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: August Highs Cap DXY Topside for Now, CHF & CAD Weakest in G10

- Despite the greenback making initial further progress on Monday, the USD index rally has stalled just ahead of the psychological 100 mark, and the August highs at 100.25. Additionally, weaker-than-expected ISM manufacturing and prices paid data have provided a moderate dollar headwind, especially against a backdrop of relatively few US data releases in recent weeks.

- Softer-than-expected CPI data in Switzerland this morning has resulted in the Swiss Franc being the weakest currency across the G10 today. EURCHF (+0.28%) held a significant medium-term support last week, and spot is now operating roughly 100 pips above the key 0.9206 level. A break back above 50-day EMA resistance at 0.9308 would be a bullish development, likely allowing the cross to re-establish the 0.93-0.94 range that was broadly in place between May/September.

- USDCAD's +0.30% Monday rally puts the pair on course for a third consecutive higher daily close but, more importantly, the pair is on course to test and break 1.4080 resistance to clear to the best levels since mid-April's Liberation Day. Tomorrow's Federal Budget in Canada remains a key risk with some analysts touting risks of a "significantly more expansionary than previous" annual budget. The next topside level would be 1.4111, the Apr 10 high.

- There was a slight divergence between the antipodeans to start the week, with AUDNZD trading to a fresh cycle high of 1.1461. Solid demand was found beneath 1.13 and the latest strength further narrows the gap towards the 2022 highs at 1.1491. A break of this level would place the cross at its highest point since 2013. The RBA decision highlights the APAC calendar on Tuesday, and NZ employment data is scheduled Wednesday.

- Other central bank decisions due later in the week include the Riksbank, Norges Bank and the Bank of England.

EURUSD TECHS: Bear Leg Extends

- RES 4: 1.1779 High Oct 1

- RES 3: 1.1728 High Oct 17

- RES 2: 1.1669 High Oct 28 and key resistance

- RES 1: 1.1577 Low Oct 22

- PRICE: 1.1530 @ 16:24 GMT Nov 3

- SUP 1: 1.1505 Low Nov 3

- SUP 2: 1.1460 1.382 proj of the Oct 17 - 22 - 28 price swing

- SUP 3: 1.1392 Low Aug 1 and bear trigger

- SUP 4: 1.1313 Low May 30

EURUSD traded lower Monday, as the current bear leg extends. The pair last Friday breached an important support at 1.1542, the Oct 9 low. This confirms a resumption of the current downtrend. Note that 1.1516, the 76.4% retracement of the Aug 1 - Sep 17 bull leg, has been pierced. A clear break of this level would expose key support at 1.1392, the Aug 1 low. Resistance to watch is 1.1669, the Oct 17 high.

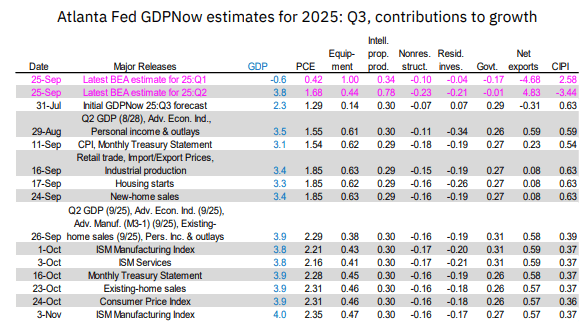

US OUTLOOK/OPINION: GDPNow Firms Further To 4.0% For Q3

- It has less to go on under the government shutdown but the Atlanta Fed’s GDPNow estimate has been revised up marginally to 3.99% annualized for Q3 real GDP growth, a fresh high, after 3.93% on Oct 24.

- Whilst it isn’t a material departure from the 3.8-3.9% updates seen through October, it’s still solid considering today’s ISM manufacturing report surprised to the downside.

- The small upward revision from Oct 24 is led by an additional 0.04pps coming from personal consumption. Equipment investment tracking was also revised up from 8.7% to 9.0% but that’s only worth an extra 0.01pp to GDP.

- It points to robust GDP growth after the 3.8% in Q2 and -0.6% in Q1, or an average of 1.6% through 1H25 when trying to control for tariff front-running, after the 2.4% through 2024.

- Alternatively, private domestic final purchases (PDFP – a favorite of Fed Chair Powell) is seen on track for a strong ~3.2% in Q3. That would be a further recovery from the 2.4% averaged in 1H25 after the 2.9% through 2024.