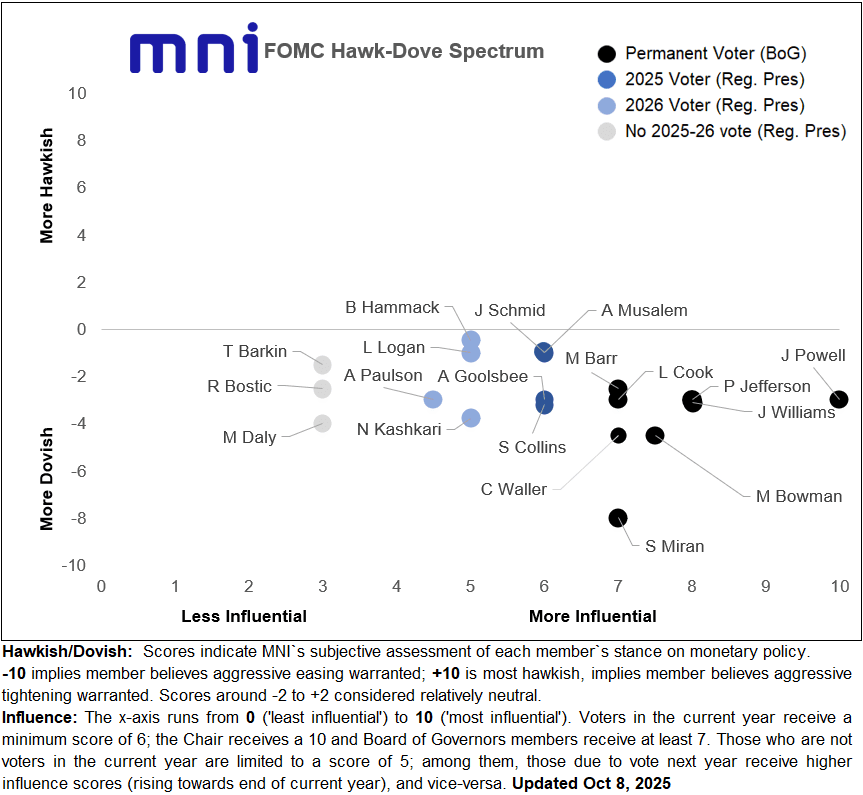

FED: September Minutes Seen Framing Lively Debate Over The Path Ahead (1/3)

Wednesday (2pm ET) sees the publication of the minutes to the September FOMC meeting. Most of the 19 members of the Committee have already spoken on their monetary policy outlook since the meeting (just four have not: Waller, Barr, Cook and Paulson, and Waller’s dovish views are well-known), so the Minutes should bring limited surprises on the rate outlook. Indeed there is a pretty good idea now of where most individual “dots” were on the September SEP. And with so little key data having been provided since the decision to reinitiate the easing cycle with a 25bp cut, there has been little more to change participants’ outlooks.

- That doesn’t mean the minutes are unimportant – indeed markets may indeed be increasingly sensitive to any signals sent in this edition, if only because of what will likely be a continuing dearth of data going into the pre-Oct 29 blackout communications period (at this point getting September Nonfarm Payrolls or CPI reports before the evening of October 17 would be a welcome surprise).

- A key question is how cautious the Minutes portray the stance on future cuts. With a split Committee evident in both the Dot Plot and Statement, as well as Chair Powell’s post-meeting commentary, we would expect some caution against signalling commitment to front-loaded cuts, and only limited discussion about outsized (ie 50bp) cuts (Powell said re this that “there wasn’t widespread support at all”). This makes for what is likely a naturally cautious tone to the Minutes. So explicit openness to those possibilities would be considered dovish, especially since there was probably a lively debate over the path forward given the meeting communications.

- Indeed, Powell’s only appearance since the meeting appeared to reiterate the press conference’s messages, in particular that there were no “risk-free” paths ahead. Recall that at the meeting (MNI review here), the statement revised the description of labor market conditions to reflect weaker conditions and mounting risks to the downside, which were of course the key factor that spurred the Fed to cut. But the projections actually showed stronger growth compared with the prior quarter’s projections, no deterioration in the labor market, and higher inflation through end-2027, with no return to target until end-2028. And the statement took the time to add language noting that inflation had moved up, which it hasn’t said for several iterations. Against this backdrop, Powell summed up the 25bp reduction as a “risk management cut”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (Z5) Bullish Structure

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-16+ @ 16:14 BST Sep 8

- SUP 1: 112-28+/112-07+ Low Sep 5 / 20-day EMA

- SUP 2: 111-24 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied sharply higher on Friday and the contract remains closer to its recent highs The move higher highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (piered), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-07+, the 20-day EMA.

FED: US TSY 13W AUCTION: NON-COMP BIDS $2.256 BLN FROM $82.000 BLN TOTAL

- US TSY 13W AUCTION: NON-COMP BIDS $2.256 BLN FROM $82.000 BLN TOTAL

FED: US TSY 26W AUCTION: NON-COMP BIDS $1.829 BLN FROM $73.000 BLN TOTAL

- US TSY 26W AUCTION: NON-COMP BIDS $1.829 BLN FROM $73.000 BLN TOTAL