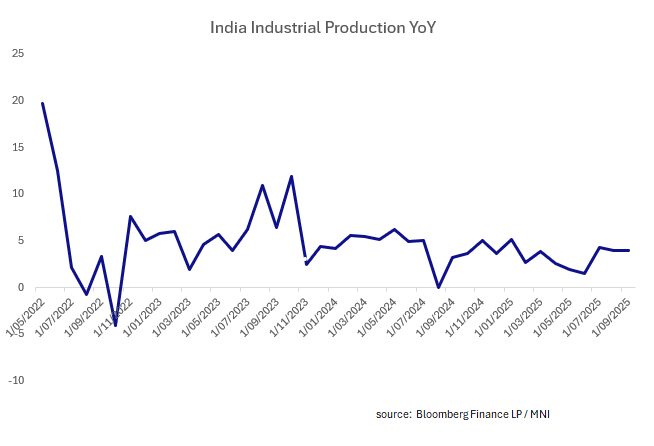

INDIA: SEPT Industrial Production Strong, Challenges Rate Cuts Priced In

- September Industrial Production topped expectations overnight, again showing the resilience in the Indian economy and how it appears impervious to tariff threats.

- Forecasts had anticipated that September could be the month where the impact from tariffs could start to show, with consensus forecast for a decline to +2.9%.

- The September result of +4.0% not only beat forecasts, but August's numbers were revised up to +4.1%

- Mining production fell 0.4% YoY versus revised +6.6% in August, whilst Electricity production rose 3.1% YoY versus +4.1% in August

- Manufacturing production rose 4.8% YoY versus +3.8% in August and Capital goods production rose 4.7% YoY versus revised +4.5% in August

- Infrastructure goods rose 10.5% YoY versus revised +10.4% in August and Consumer durables rose 10.2% YoY versus +3.5% in August.

- The resilience of the Indian economy continues to show. With just over a month to go before the next RBI meeting, swaps and bond signals are still suggesting that the last meeting for the year will see a cut. The swaps market has 25bps of cuts over the next month and 29bps over the next two, whilst the MIPR function on Bloomberg has 29 cuts priced in over the next month. The risk to markets is now no cut, which could see yields spike and the 10-Yr back above 6.60%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

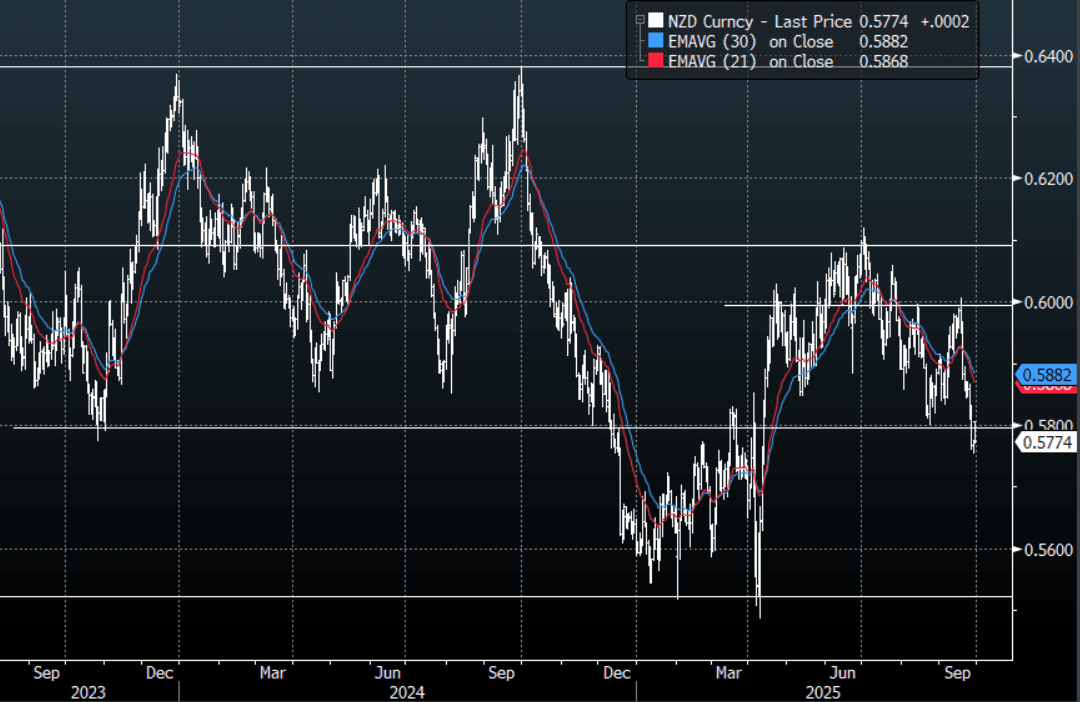

NZD: NZD/USD - Closes The Week Below 0.5800

The NZD/USD had a range overnight of 0.5754 - 0.5776, Asia is trading around 0.5775. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The NZD broke through its pivotal 0.5800 support last week which should keep the pair under pressure heading into payrolls. The first sell zone would be between the 0.5850/0.5900 area. US Futures have opened slightly higher this morning, E-minis +0.10%, NQU5 +0.10%.

- Bloomberg - “New Zealand Dollar Worst Performing G10 Currency This Year. The New Zealand dollar has become the worst performing G10 currency in the year to date. It is up 3.18% against the U.S. dollar, trading at 0.58 to the U.S. currency.”

- MNI AU - Monthly Data May Shape OCR Expectations. This week will provide more information on how NZ’s recovery tracked in Q3. The higher frequency data have been the focus of the RBNZ for over a year and so should help shape expectations for the 8 October RBNZ decision where some are forecasting a 50bp rate cut following the very weak Q2 GDP print.

- "NZ AUG. FILLED JOBS RISE 0.2% M/M, NZ AUG. FILLED JOBS 2.346M" - BBG

- MNI AU - Labour Market Weak But Turning. August filled jobs rose 0.2% m/m after a downwardly revised flat July. This is the first increase in hiring since January and while the labour market appears to have stabilised conditions remain weak with filled jobs down 0.7% y/y. On a positive note, the August increase was across sectors with the good-producing industries the strongest.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5785(NZD904m Sept 30), 0.5875(NZD372m Sept 30) - BBG

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

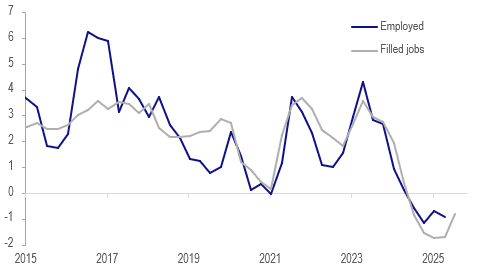

NEW ZEALAND: Labour Market Weak But Turning

August filled jobs rose 0.2% m/m after a downwardly revised flat July. This is the first increase in hiring since January and while the labour market appears to have stabilised conditions remain weak with filled jobs down 0.7% y/y. On a positive note, the August increase was across sectors with the good-producing industries the strongest. The next RBNZ decision is on October 8 and it is expected to ease again but it remains uncertain if it will be by 25bp or 50bp.

- The Q3 average to date filled jobs are up 0.1% q/q, which if sustained would be the first positive after 5 quarterly contractions. September filled jobs are published on 28 October and Q3 labour data on 5 November.

NZ filled jobs vs employment y/y%

Source: MNI - Market News/LSEG/Statistics NZ

- Good-producing industries increased filled jobs by 0.6% m/m in August with the primary sector up 0.2% and services +0.1%. Over the last year construction has been the weakest down 5.1% y/y followed by professional, scientific and technical services -2.7% y/y, while healthcare and education were both up 1.7% y/y.

- The weakness in the jobs market has been concentrated in the under 35s with 15-19 years -8.2% y/y, 20-24 years -3% y/y and 25-29 years -3.5%. Due to this many people have stayed in education.

- Another tentative sign of a stabilisation in the jobs market is the SEEK new job ads index which was up 4.4% y/y in August after contracting since November 2022. The index is at its highest since May 2024.

AUD: AUD/USD - Finds Buyers Towards 0.6500 As The USD Move Stalls

The AUD/USD had a range overnight of 0.6521-0.6552, Asia is trading around 0.6550. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The AUD found some demand back towards the 0.6500 area and is trying to bounce. Price is back in the range and the market will be turning its attention towards Fridays Payroll number if it is released. The AUD outperformance continues to be better expressed in the crosses for the time being.

- MNI RBA WATCH: On Hold, Eyeing Further Labour, CPI Data. The Reserve Bank of Australia board is likely to hold the cash rate at 3.6% tomorrow as it considers the floor of its easing cycle and awaits clearer signals on inflation and labour market tightness, making a November cut a possibility. Former RBA officials argue that a tight labour market, weak productivity, and strong wage growth could limit the Bank to just one or two more cuts, with the risk tilted toward one. They agree labour market performance will be central to the Bank’s next steps.

- Bloomberg - “Trump will meet the top four congressional leaders at the White House Monday as an Oct. 1 shutdown looms. The US will still continue to collect tariff revenue and pursue its immigration crackdown if the government closes.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD405m), 0.6625(AUD1.29b), 0.6725(AUD1.19b). Upcoming Close Strikes : 0.6600(AUD943m Oct 1), 0.6600(AUD1.57b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

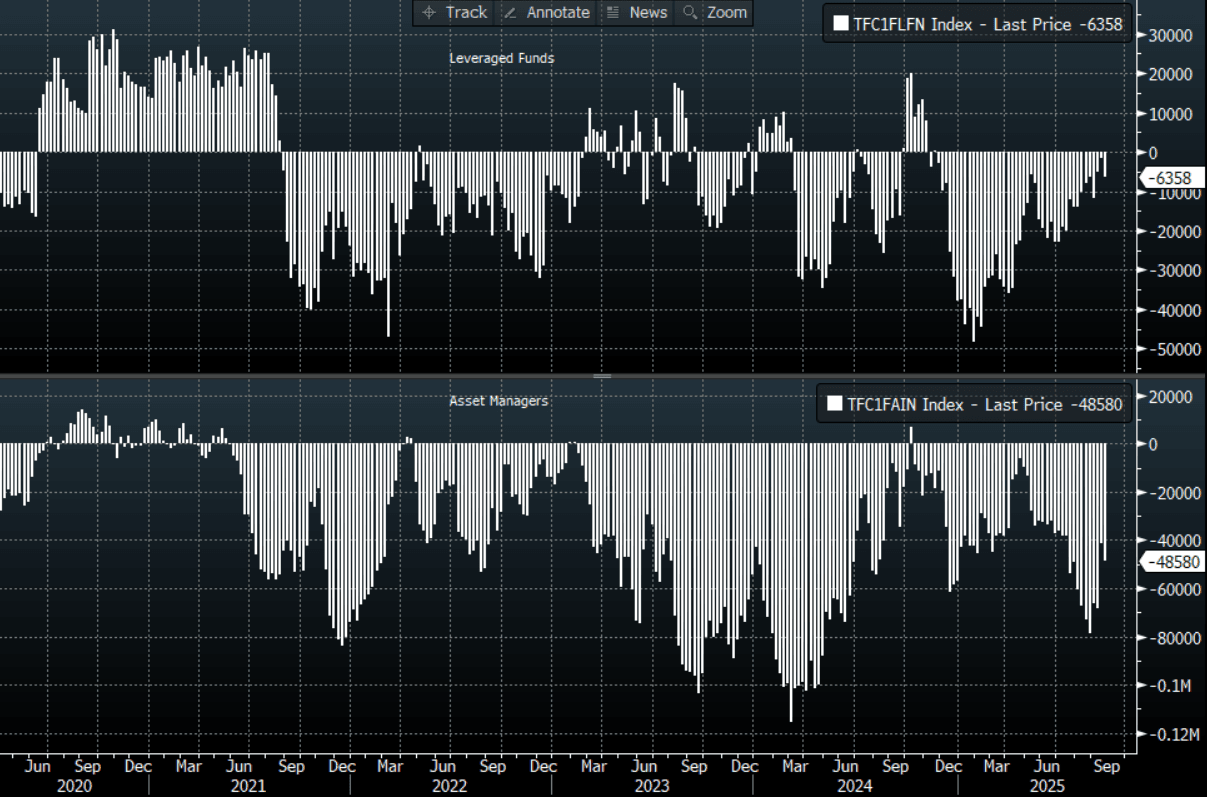

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P