EU FINANCIALS: SEB Group (SEB Aa3/A+/AA)- Q4 Results - market reaction & valuation

Following the SEB group FY 24 results this morning the equity is down, following a good run into results. This was mostly being attributed to a lower than expected dividend this quarter. Reuters reports the SEK 11.5 dividend was below an expected SEK 12.73.

Clearly management have to balance equity holder returns with bondholder expectations - which will be slightly jarred by the -1.8% fall in CET1, although this is largely frontloading of the planned - and still optional should a shock occur - share buyback. We think a combination of solid capital generation and management target of 100-300bps above the minimum threshold are both reasonable for creditors, although creditors would probably like to remain in the upper half of that range.

We think by far the most notable point in the Q4 results is the jump in Stage 3 loans - which were not touched upon much during the earnings call or questions. Management noted there were " a handful of larger exposures requiring provisioning", but believed this uncorrelated. Further commenting that broadly credit quality remains legacy risks in funding-dependent sectors like real estate and private equity remains

The bonds are arguably lagging a strong market today, most noticeable in their 2's.

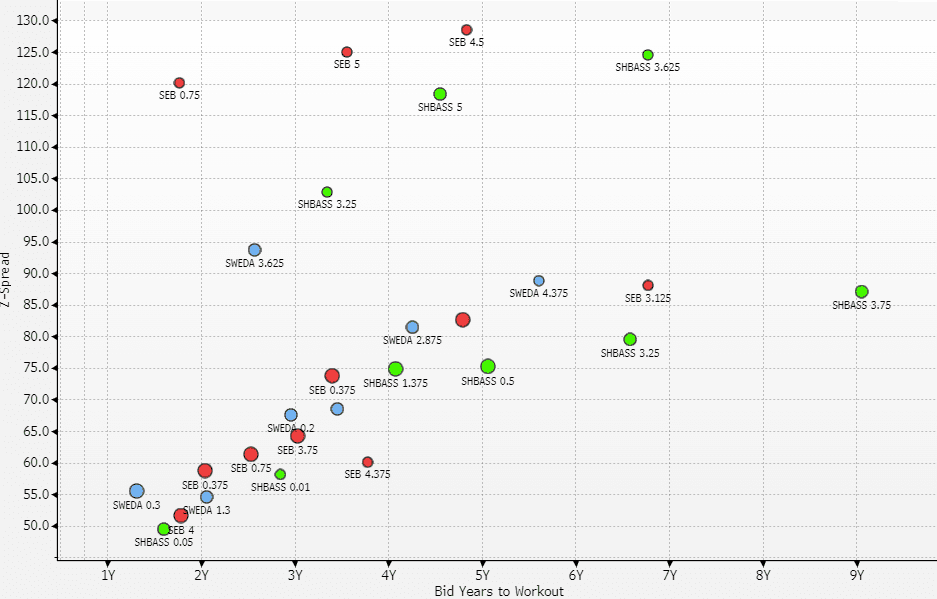

Valuation: Despite the minor concerns SEB trades close to SWEDA in Sr Non-Pref - which are lower rated but reported very decent results recently. The given how steep the SHBASS tier 2 curve is however, we wouldn’t be surprised if investors prefer the higher quality SHBASS 3.625% as the pick of the Swedish tier 2's

Link to earlier Q4 results post - https://mni.marketnews.com/412KTMd

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: No clear drivers for European FI despite higher Spain inflation

- There's no overarching driver for European fixed income this morning. The main event has been the release of Spanish inflation - which came in a couple of tenths above consensus.

- EGBs have seen curve flattening with 2-year yields marginally higher (as are Whites and some Red Euribor futures) but the bigger (yet still rather limited) moves have been further out the curve with 10-year Bunds (and other 10-year EGBs) moving off their early morning / late Friday lows.

- Gilts have in contrast seen a more parallel move in curves with yields around 1.1-1.6bp lower on the day at writing.

- The moves higher for core FI around the 10-year area come as European stock markets move off some of their early lows (although US markets, Eurostoxx and the FTSE100 are all still lower on the day).

- Gilt futures are up 0.05 today at 91.89 with 10y yields down -1.1bp at 4.620% and 2y yields down -1.6bp at 4.432%.

- Bund futures are down -0.01 today at 133.01 with 10y Bund yields down -0.9bp at 2.386% and Schatz yields up 0.3bp at 2.095%.

- BTP futures are up 0.03 today at 119.88 with 10y yields down -1.6bp at 3.525% and 2y yields up 0.3bp at 2.417%.

- OAT futures are down -0.03 today at 123.22 with 10y yields down -1.1bp at 3.199% and 2y yields up 0.1bp at 2.280%.

STIR: Large Jun'25 SOFR Midcurve Option Package

- Just over 33,000 0QM5 96.37/97.00 call spds vs. 95.37/95.62 put spds ref 96.02 - checking direction.

US TSYS: Tsys Unwinding Friday's Sale, PMI, Pending Home Sales Ahead Year End

- Treasuries are looking modestly firmer, near early early London session highs as rates recover from Friday's sell-off. The Mar'25 10Y contract trades 108-19 last (+5) vs. 108-21 high on decent volumes heading into year end: just over 175k at the moment.

- Average to small year-end duration extensions: US +0.07Y, EU: +0.04Y, UK -.02Y (Bbg)

- Tsy 10Y yield at 4.5951% (-.0303), curves mixed with 2s10s -.342 at 28.950 despite overnight Block steepener: +4,276 TUH5 at 102-22.75 vs. -2,592 TYH5 108-17.5 (0256:12ET); 5s30s +1.752 at 37.159.

- Projected rate cuts into early 2025 look steady to slightly higher vs. late Friday levels (*) as follows: Jan'25 steady at -2.8bp, Mar'25 -13.6bp (-13.3bp), May'25 -19.5bp (-18.5bp), Jun'25 -28.8bp (-26.5bp).

- Data on tap (prior, estimate): MNI Chicago PMI (40.2, 43.0) at 0945ET, followed by Pending Home Sales at 1000ET MoM (2.0%, 0.8%), YoY (6.6%, 7.9%). Dallas Fed Mfg Activity at 1030ET (-2.7, -3.0). Dearth of scheduled Fed speak until Richmond Fed's Barkin gives keynote remarks at a Maryland Bankers assn event on January 3 at 1100ET (text & Q&A).

- Treasury auctions $84B 13W, $72B 26W bills at 1130ET followed by 75B 42D CMBs at 1300ET.