EU TECHNOLOGY: SAP: Q3 Results

(SAPGR; A1/A+/NR)

In line set of results with the usual strong growth and expanding margins which both agencies are looking for to upgrade. The 31s already sit tight of the AA ex. Utils/Fins index.

- Q3 Revs: €9.1bn (+7% YoY, in line). YTD: €27.1bn (+9% YoY).

- Q3 Org Rev Growth: 11.0% YoY (+1pp vs. Q324, 0.2pp miss).

- Q3 Op Profit: €2.6bn (+14% YoY, 1% beat). YTD: €7.6bn (+33% YoY).

- Q3 FCF: €1.3bn (+5% YoY, 49% beat). YTD: €7.2bn (+40% YoY).

- Net cash position €2.5bn vs. €2.3bn at Q2 and €2.9bn at Q324.

- FY cloud revs at low end of range but op profit at upper end. FCF tweaked higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UN: Trump Calls For Immediate Hostage Release & NATO Stop Russia O&G Purchases

In his address to the United Nations, US President Donald Trump lambasts the organisation for "not being there for us" during peace negotiations. Says that the UN "has tremendous potential" but is "not coming close to living up" to this. Trump claims that the UN offers only "Empty words, and empty words don’t solve war."

- Says we "have to get a Gaza ceasefire", but that "Hamas rejects reasonable peace offers." Says recognition of a Palestinian state "would be too great for Hamas". Trump: "Those who want peace should be united behind one message: release the hostages". Trump: "We have to stop the Gaza war immediately".

- On Ukraine, Trump says the war in Ukraine "is not making Russia look good, it's making them look bad". Trump: "The question now is how many more lives are lost on both sides." Criticises Chinese and Indian purchases of Russian O&G, but also NATO countries. Trump: "They're funding a war against themselves...Europe has to step it up...They have to immediately cease energy purchases from Russia".

- Trump says that he is set to talk to European leaders later today to press the issue. Hungarian Peter Szijjarto said on 22 Sep that stopping Russian purchases was a 'nice idea', but "We can’t ensure the safe supply [of energy products] for our country without Russian oil or gas sources,"

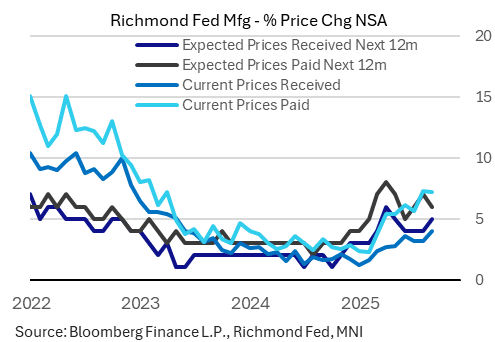

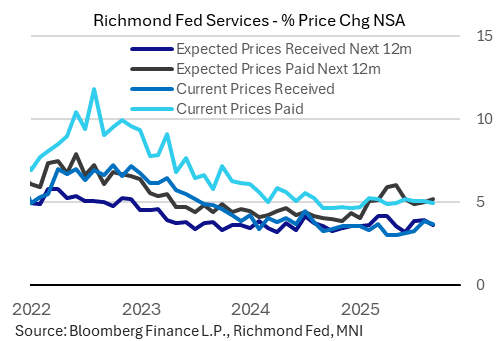

US DATA: Richmond Fed: Price Developments Mixed In September (2/2)

The Richmond Fed surveys' inflation subcomponents were somewhat mixed in September, with continued pressures more apparent for manufacturers than for services firms. Note that the Richmond Fed reports its price indices differently from the other regional banks, expressing them in percentage changes over the last / next 12 months.

- Manufacturing prices remained stubbornly high: current prices paid stayed at 7.2% for a second consecutive month (August's was a 27-month high), with prices received picking up sharply to 4.0% - the latter marking a 27-month high (and a potential sign that manufacturers are passing through tariff costs).

- Expected prices paid dipped to 6.0% however from 7.0%, with received up to 5.0% after four months at 4.0%.

- Services price inflation was better-behaved. Current paid dipped to 5.0% from 5.1%, marking a 4-month low, with prices received at a 2-month low 3.7% after August's 3.9% was the highest in over a year.

- Expected prices paid ticked up to 5.2% from 5.0%, though expected received fell to 3.6% from 4.0% for a 3-month low.

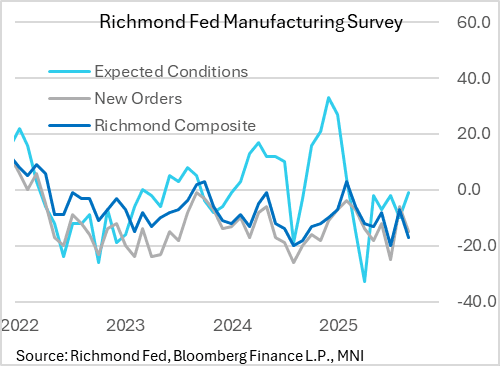

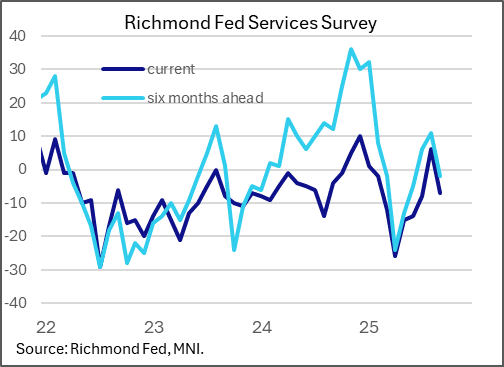

US DATA: Richmond Fed: Pickup In Activity Fails To Persist In September (1/2)

The Richmond Fed's Fifth District surveys of regional manufacturing and services firms for September showed that a nascent pickup in activity in August may have been an outlier. The headline aggregate indices as well as key sub-components weakened, though were roughly in line with averages seen over the last year.

- The manufacturing survey showed a sharp retrenchment to -17 in September from -7 prior, for the 2nd weakest headline figure since September 2024 and a full reversion of the surprise improvement in August. This was far worse than the expected improvement to -5 (Bloomberg consensus).

- The internals of the report were weak: all three of the composite sub-indices pulled back, including shipments (−20 from −5), new orders (−15 from −6), and employment (−15 from −11). In a rare bright spot, expectations improved to -1 from -10.

- The Services business activity index reverted to -7 in September after an improvement to 6 in August. Similarly the 6-month outlook fell to a 3-month low -2 from 11 prior.

- As with manufacturing, current measures were weak (revenues down to 1 from 4, demand down to 3 from 13), though employment remained steady.