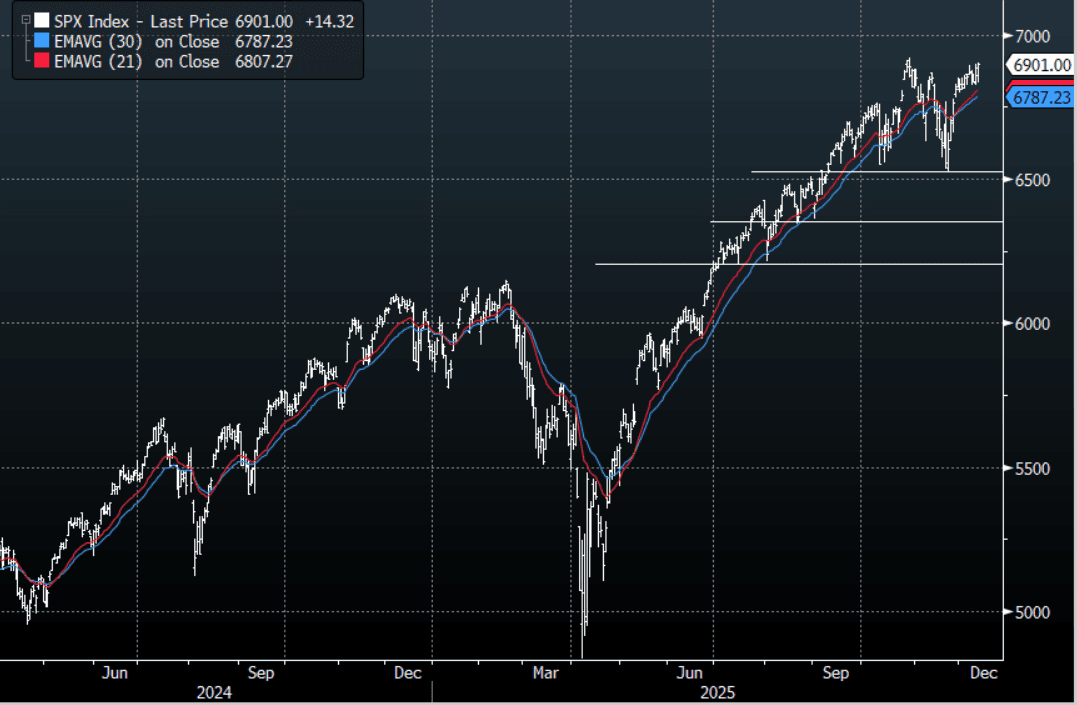

US STOCKS: S&P(ESZ5) - Looking To Challenge Highs en Route To 7000

The S&P(ESZ5) overnight range was 6828.50 - 6928.75, SPX closed +0.21%, Asia is currently trading around 6905. Risk has regained its momentum higher on the surprisingly dovish FOMC. This morning futures have opened a little lower, E-minis(S&P) -0.02%, NQZ5 -0.10%. The S&P is again challenging all-time highs but it's the broader market that is playing catch up as rotation again picks up, Russell Index +1.21%, Dow Transports + 0.64%. On the day, dips back toward 6800-6830 should now be supported as the market tries to find the momentum to make new all-time highs and challenge the 7000 area.

- James Lavish on X: “It was only a matter of time. With the government running multi-trillion dollar deficits, once the Reverse Repo Facility slush fund is drained, the ability for the Fed to reduce its balance sheet is nullified, and the Treasury's need for additional liquidity must come from somewhere. And that 'where' is, in fact, the Fed again. As predictable as a tide that goes out and comes back in, the Fed must print again.”

- Zerohedge on X: "What Bessent/Trump want is cheap funding – flood the short end and starve the long end of issuance. Today, the Fed announced it will be there to buy the short end. - TS Lombard”

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 60 Points

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Cold Winter Outlook Drives US Gas Up, Milder Europe Keeps It In Range

US gas continued to rise strongly driven by wintery weather across the east and forecasts for a cold season. Prices are now almost 10% higher this month and 21% since 17 October but is now flashing overbought. Production remains ample though to provide for increased heating consumption and robust demand for LNG exports. European prices continue to trade in a narrow range waiting for direction.

- Henry Hub rose 4.3% to $4.525 after reaching $4.581 off a low of $4.276. Not only has a cold snap hit the eastern US this week, but long-term forecasts for November to March have shifted cooler, according to Bloomberg. Temperatures for mid- and into the second half of the month have also been revised lower for the north and central US (Vaisala). Thus heating demand over winter is looking solid. BNEF data showed demand on Tuesday was up 20.1% y/y.

- European gas was little changed trading between EUR 30.83 and 31.180. The lack of direction is reflected by flat prices in November. The market is waiting for information on the outlook for winter and is stable while LNG imports remain strong but remains vulnerable to any supply disruptions.

- Storage in Europe is slightly lower at 82.4% having reached 83% last week. Near-term the weather shouldn’t cause a drawdown with temperatures above average over the second half of November, according to Bloomberg.

JGB TECHS: (Z5) Fades Toward Support

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 135.90 @ 16:17 GMT Nov 11

- SUP 1: 135.58 - Low Nov 10

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

Prices started last week well, growing the gap with next support into the 135.61 Oct 08 low. Despite this stability, prices remain inside the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. Further weakness would open 135.39 next, a Fibonacci projection.

AUSSIE BONDS: Dec-35 Supply Faces Higher Yield But Flatter Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 17 September 2025 for A$1200mn. The line was opened via syndication on 24 July 2024 for A$11.5bn. Bidding is likely to be shaped by several key factors:

- The current outright yield is around 10bps higher than at the previous auction and approximately 40bps lower than the peak in late 2024.

- The 3/10 yield curve is around 10bps flatter than the previous auction level and sits around 50bps below its recent high.

- On the positive side, the auction comes amid stronger sentiment toward longer-dated global bonds.

- Moreover, the line is included in the XM basket.